Crypto exchange Bybit will enforce mandatory KYC to access all of its products and services.

This is no less than a Cultural conflict, as Crypto has always rejected the notion of proving one’s identity.

Crypto, perhaps rebranded as the more respectable-sounding web3, steers ever closer toward mainstream integration. Is it a given that certain tenets that have always been central to the crypto space may start to be edged out as they are incompatible with traditional and legally compliant operating methods?

Regarding financial operations and anti-money laundering requirements, know-your-customer (KYC) protocols are a regulatory expectation. Yet, up to now, crypto has operated in a gray area, or at least an inconsistent one, with different platforms and services employing systems that are not always aligned.

However, the direction of movement, particularly for centralized exchanges, appears only to be in one direction, towards a greater emphasis on unavoidable KYC procedures for customers, as evidenced recently by changes taking place at the trading exchange, Bybit.

What's Happening at Bybit?

A recent announcement from the major crypto exchange detailed its plans to enforce mandatory KYC on all users to access its products and services. This new arrangement will start today and affect both new and existing customers.

Notably, the first two reasons given by Bybit for enforcing this change are "security and compliance" and "prevent illegal activities". In addition, there are reasons given that relate to improving the user experience, including "enhanced services", "exclusive offers", and "convenience and security".

Notably, Bybit is taking an overall approach in which KYC must use any aspect of its platform, which is not the case with all of its competitors.

Trading without KYC

After Bybit has changed its approach, there will still be some well-known platforms that allow some of their trading services to be accessed without KYC completion, including OKX and KuCoin, both of which allow non-KYC cryptocurrency withdrawals.

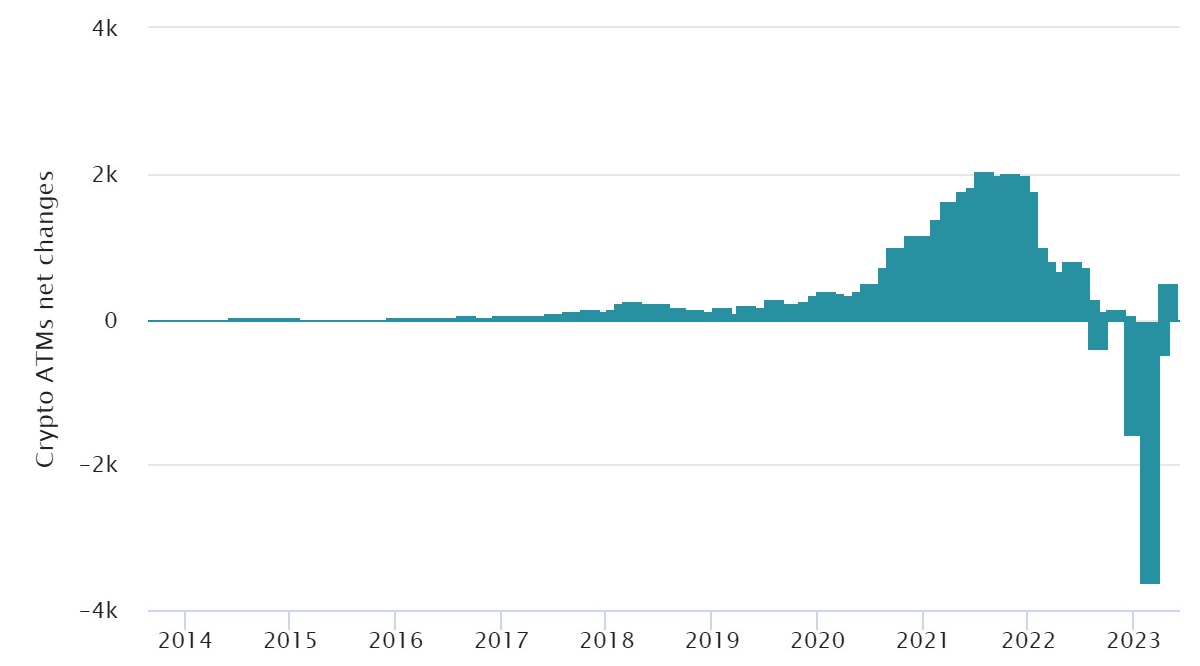

Crypto ATMs and peer-to-peer trades are also still options. However, ATM installation has stalled. Earlier this year, the longstanding platform LocalBitcoins, which acted as a means for buyers and sellers to find one another, closed down due to a lack of market demand for its services after more than ten years in operation. This closure, which is coming at the same time as the EU's MiCA, arguably marks the end of a crypto era as the entire ecosystem shifts in from the fringes.

Chart from Coin ATM Radar

That said, decentralized exchanges such as Uniswap and Sushi remain faithful to the spirit of the tech, requiring neither permission nor verification and no trusted third parties to use their protocols. However, what can't be done on these platforms is cashing out to fiat, and it's at this contact point with traditional finance that most users find themselves subject to orthodox formalities.

Uniswap and Sushi are integrated with fiat on-ramps to allow crypto purchases (through MoonPay and Transak, respectively); these integrated providers enforce their own KYC processes.

Mastercard and Web3 Verification

One giant of traditional finance executing a web3 strategy is Mastercard, and, just as it is occurring at crypto-native exchanges, it's also emphasizing user verification.

Mastercard has demonstrated its interest in crypto and web3 through its Mastercard Artist Accelerator, which uses NFTs on Polygon to connect musical talent with the digital economy, and through a partnership with web3 payment protocol Immersive.

Accordingly, Mastercard has created a standards and infrastructure package called Mastercard Crypto Credential, which aims to facilitate user verification across blockchain networks. The idea is that this system allows varying regulatory standards to be met, errors reduced, and consumer experiences improved.

These developments are being worked on in collaboration with blockchain organizations, including The Solana Foundation, Polygon Labs, Aptos Labs, and several crypto wallet providers.

Mastercard's announcement talks about "instilling trust in the blockchain ecosystem", but this brings to mind a possible contrast with a founding ideal in crypto of a trustless system, meaning one in which it's not necessary to trust anyone, neither counterparty nor third party since the blockchain network itself enables hard-coded mechanisms for verification instead.

A Clash of Cultures?

Perhaps it's inevitable that as traditional finance and cryptocurrencies shift into a closer shared orbit, clashes in culture, and methods of operation, will become apparent. Crypto has always, at its core, rejected the notion of proving one's identity, and safeguarding the freedom to transact without permission has been a key driver in its development.

When it comes to decentralized exchanges, these ideals are built in, and in the case of peer-to-peer transactions, no third parties or permissioned rails are required.

However, trade-offs are taking place at centralized exchanges and when interacting with non-crypto consumer environments to comply with financial norms and operate above-board platforms. If these adaptations bring in new users and greater adoption, there will, perhaps, be few complaints.

However, there is the potential that once a new user is acquainted with crypto, they may find themselves wandering from centralized entities to decentralized protocols and, in the process, picking up on those founding elements, decentralization, and trustless systems, that crypto was always intended to enable.

Crypto, perhaps rebranded as the more respectable-sounding web3, steers ever closer toward mainstream integration. Is it a given that certain tenets that have always been central to the crypto space may start to be edged out as they are incompatible with traditional and legally compliant operating methods?

Regarding financial operations and anti-money laundering requirements, know-your-customer (KYC) protocols are a regulatory expectation. Yet, up to now, crypto has operated in a gray area, or at least an inconsistent one, with different platforms and services employing systems that are not always aligned.

However, the direction of movement, particularly for centralized exchanges, appears only to be in one direction, towards a greater emphasis on unavoidable KYC procedures for customers, as evidenced recently by changes taking place at the trading exchange, Bybit.

What's Happening at Bybit?

A recent announcement from the major crypto exchange detailed its plans to enforce mandatory KYC on all users to access its products and services. This new arrangement will start today and affect both new and existing customers.

Notably, the first two reasons given by Bybit for enforcing this change are "security and compliance" and "prevent illegal activities". In addition, there are reasons given that relate to improving the user experience, including "enhanced services", "exclusive offers", and "convenience and security".

Notably, Bybit is taking an overall approach in which KYC must use any aspect of its platform, which is not the case with all of its competitors.

Trading without KYC

After Bybit has changed its approach, there will still be some well-known platforms that allow some of their trading services to be accessed without KYC completion, including OKX and KuCoin, both of which allow non-KYC cryptocurrency withdrawals.

Crypto ATMs and peer-to-peer trades are also still options. However, ATM installation has stalled. Earlier this year, the longstanding platform LocalBitcoins, which acted as a means for buyers and sellers to find one another, closed down due to a lack of market demand for its services after more than ten years in operation. This closure, which is coming at the same time as the EU's MiCA, arguably marks the end of a crypto era as the entire ecosystem shifts in from the fringes.

Chart from Coin ATM Radar

That said, decentralized exchanges such as Uniswap and Sushi remain faithful to the spirit of the tech, requiring neither permission nor verification and no trusted third parties to use their protocols. However, what can't be done on these platforms is cashing out to fiat, and it's at this contact point with traditional finance that most users find themselves subject to orthodox formalities.

Uniswap and Sushi are integrated with fiat on-ramps to allow crypto purchases (through MoonPay and Transak, respectively); these integrated providers enforce their own KYC processes.

Mastercard and Web3 Verification

One giant of traditional finance executing a web3 strategy is Mastercard, and, just as it is occurring at crypto-native exchanges, it's also emphasizing user verification.

Mastercard has demonstrated its interest in crypto and web3 through its Mastercard Artist Accelerator, which uses NFTs on Polygon to connect musical talent with the digital economy, and through a partnership with web3 payment protocol Immersive.

Accordingly, Mastercard has created a standards and infrastructure package called Mastercard Crypto Credential, which aims to facilitate user verification across blockchain networks. The idea is that this system allows varying regulatory standards to be met, errors reduced, and consumer experiences improved.

These developments are being worked on in collaboration with blockchain organizations, including The Solana Foundation, Polygon Labs, Aptos Labs, and several crypto wallet providers.

Mastercard's announcement talks about "instilling trust in the blockchain ecosystem", but this brings to mind a possible contrast with a founding ideal in crypto of a trustless system, meaning one in which it's not necessary to trust anyone, neither counterparty nor third party since the blockchain network itself enables hard-coded mechanisms for verification instead.

A Clash of Cultures?

Perhaps it's inevitable that as traditional finance and cryptocurrencies shift into a closer shared orbit, clashes in culture, and methods of operation, will become apparent. Crypto has always, at its core, rejected the notion of proving one's identity, and safeguarding the freedom to transact without permission has been a key driver in its development.

When it comes to decentralized exchanges, these ideals are built in, and in the case of peer-to-peer transactions, no third parties or permissioned rails are required.

However, trade-offs are taking place at centralized exchanges and when interacting with non-crypto consumer environments to comply with financial norms and operate above-board platforms. If these adaptations bring in new users and greater adoption, there will, perhaps, be few complaints.

However, there is the potential that once a new user is acquainted with crypto, they may find themselves wandering from centralized entities to decentralized protocols and, in the process, picking up on those founding elements, decentralization, and trustless systems, that crypto was always intended to enable.

Sam White is a writer and journalist from the UK who covers cryptocurrencies and web3, with a particular interest in NFTs and the crossover between art and finance. His work, on a wide variety of topics, has appeared on platforms including The Spectator, Vice and Hacker Noon.

Deutsche Börse’s 360T Plugs Bitpanda Into FX Network to Channel Institutions Into Crypto

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights