After months of bullish gains, crypto markets could be geared for a cooldown.

FM

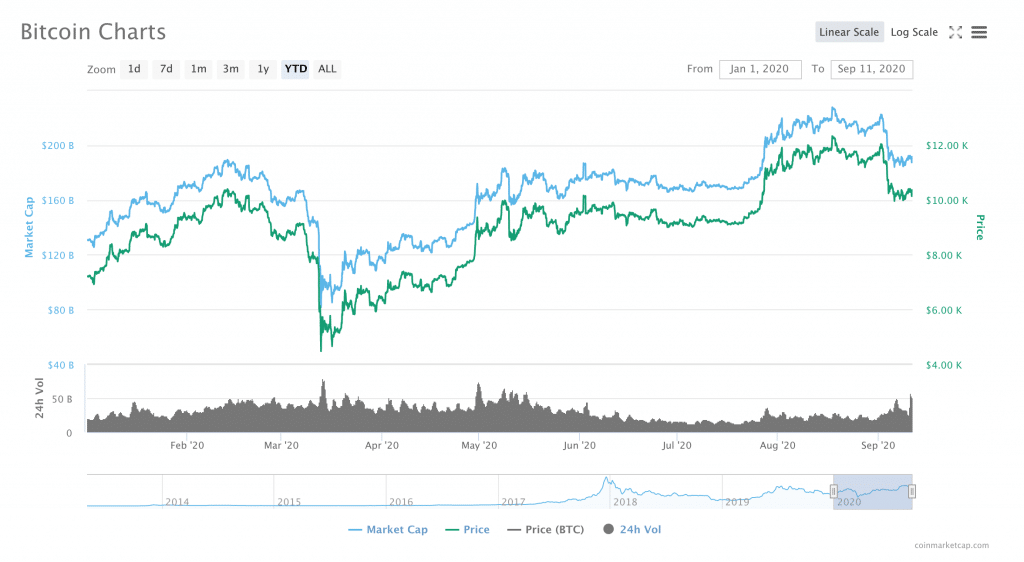

This week tested Bitcoin’s mettle over the $10,000 level. After dipping from around $11,200 to roughly $10,250 from Thursday, September 3rd, to Friday, September 4th, Bitcoin has not shown any signs of rising back over the $11,000.

In fact, Bitcoin even dipped below the $10,000 mark on several occasions this week, reaching back into price territory that has not been seen since late July.

Bitcoin’s movement down over the past several weeks seems to have vastly changed the narrative about where Bitcoin is headed next. Throughout much of August, Bitcoin’s reaches over $12k seemed to inspired analysts to think big: Bitcoin was headed toward $20,000, no, make that $50,000.

Now, the narrative around Bitcoin seems to have returned to whether Bitcoin can hold past the $10,000 mark.

However, the fall back towards $10,000 may not be entirely unwelcome. CoinTelegraph reported that “over the medium to long term, traders expect Bitcoin to recover and perceive the ongoing consolidation phase as a healthy pullback.”

In other words, this latest pullback could be the latest purge of speculative overbuying from the price of BTC. After all, the hold above $11k that took place throughout much of August may have brought buyers into the market who were exclusively interested in short-term gains.

Bitcoin Teeters on the Edge of $10k

On the other hand, the CME gap that was formed around the $9,700 mark last week still remains a threat. A ‘CME gap’ refers to a phenomenon in which Bitcoin markets make a sharp, sudden move outside of regular trading hours for CME’s Bitcoin futures markets, which results in a literal ‘gap’ in Bitcoin price charts.

Often when this happens, the Bitcoin price will eventually fall back to the level where the gap was originally formed. This retrace in the price of Bitcoin 'fills' the gap. Therefore, because the gap is around the $9700 zone, some analysts believe that Bitcoin is headed at least that low before any meaningful, long-term gains will be possible.

Although, there are some analysts who believe that Bitcoin is such a hot commodity that the gap may remain 'empty'.

Woo also added that “if so it'll be the first CME gap on daily candles that remains unfilled,” a point that was contested by several other Twitter users.

I'd say there's a fair chance this CME gap may not get filled, so far it's been front run for liquidity. Every dip snapped up.

Woo also tweeted a chart that indeed showed, when Bitcoin was headed for $9,700 earlier this week, buyers jumped on the BTC dip before it got too low.

BTC Bears May Be in the Majority

Still, while BTC may not be at a real risk of falling below $9700, some analysts do find the fact that Bitcoin seems unable to recapture the $10,500 resistance level concerning.

Indeed, while BTC bulls may be buying up Bitcoin when it begins to approach $9,700, Bitcoin bears seem to be consistently selling around $10,500. The fact that Bitcoin has been unable to surpass this level suggests that BTC bears may be in the majority this time around.

Still, while BTC has waffled between $9,800 and $10,500 for the past week, traders still seem to be uncertain where Bitcoin is headed next.

However, by Thursday, the picture looked quite different: around noon CET, data from Messari showed that 32 the 37 tokens were back in the green, including the tokens that had lost out worse, earlier in the week.

However today, DeFi markets are a mixed bag: over two-thirds of the DeFi assets tracked by Messari were back in the red.

The assets that were in the green showed relatively modest gains; Yearn.Finance led the pack with 24-hour increase of 13.76 percent, while Mainframe, Loopring and Gnosis followed closely behind with gains over 10 percentage points. 0x, Airswap, Synthetix, Terra, Cream, Blockmason, Kava, and Wrapped Nexus mutual were all in the green for less than 10 percentage points.

After Months of Red-Hot Gains, DeFi Tokens Seem to Be Cooling Down

While these kinds of gains may be significant in traditional markets, and even for other kinds of crypto assets, the DeFi space has been so hot for the last several months that any upward movement below 20 percent almost seems paltry.

Indeed, a number of DeFi assets have consistently made headlines throughout the course of the year for their eye-popping growth. For example, Finance Magnatesreported in August that the price of Band Protocol tokens had increased 6000 percent, and that Chainlink tokens had increased more than 659 percent since January 1st.

However, like Bitcoin, August seemed to be a bit of a high point for DeFi tokens, and while the DeFi space may be geared for gain in the long term, the DeFi space could be staring at a serious market correction, right in the face.

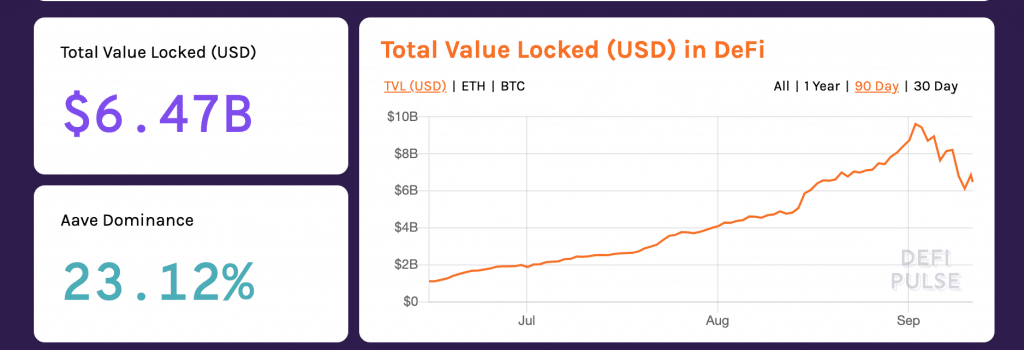

In fact, the correction already seems to have begun: earlier this week, crypto Twitter commentator @cryptounfolded pointed out that in addition to token prices, the total amount of value 'locked' in DeFi protocols had also taken a hit.

Indeed, on September 2nd, the total value locked peaked at over $9.5 billion before crashing to as low as $7.56 billion on Sunday, September 6th. At press time, the total value locked had fallen even further, sitting at $6.47 billion.

Ethereum Congestion May Be Contributing to DeFi Downfall

What is driving the prices down? In addition to the pressure to sell that may be rippling out from Bitcoin markets, DeFi may also be feeling the aftereffects of several recent incidents that took place over the course of the last 2 weeks.

In particular, assets that have ties to the Ethereum ecosystem may have been affected by a massive increase in transaction fees and decreases in transaction speeds during the first few days of this month.

Indeed, according to on-chain analytics firm, Glassnode, miners on the network earned over $500,000 in just 1 hour on September 1st. Around the same time, Ethereum network users reported transactions taking much longer than usual to complete.

The more traffic there is on the network, the more congested it becomes; as it becomes more congested, fees go up, and transaction times slow down. In the long term, this means that DeFi developers may be seeking alternatives to Ethereum.

SushiSwap Snafu, EMD Exit Scam May Be Contributing to DeFi Cooldown

Beyond Ethereum, the DeFi space was also marked by the SushiSwap saga that took place over last weekend, a series of events that had large swathes of the community accusing a popular new protocol of being an exit scam.

The trouble began on Saturday, when the pseudonymous founder of SushiSwap, known only as ‘Chef Nomi’, suddenly made the decision to sell all of his SUSHI tokens, which totaled roughly $13 million.

The move caused the token price to suddenly take a significant dive: after peaking at $11.27 on Tuesday, September 1st, SUSHI prices dropped to as low as $1.21 on Saturday. This led the crypto community to initially decry the project as an exit scam. Though, control of the protocol was eventually handed over to members of the DeFi community.

In addition to the SushiSwap incident, a liquidity mining DeFi project on the EOS network known as Emerald Mine (EMD) was accused of an exit scam.

While incidents of fraud have been relatively few and far between in the DeFi space, compared to the ICO space in late 2017, both incidents have been the subject of much controversy.

However, Corey Caplan, partner of the DeFi Money Market Foundation, pointed out to Finance Magnates that, though much less frequent, incidents of fraud in the DeFi space could be having a large impact.

“In any nascent sphere, a single entity’s failure or success can have an outsized effect on the entire space,” he said. “This is what happened with the SushiSwap snafu, but I don’t believe this incident should be viewed as an encapsulation of the entire DeFi ecosystem.”

This week tested Bitcoin’s mettle over the $10,000 level. After dipping from around $11,200 to roughly $10,250 from Thursday, September 3rd, to Friday, September 4th, Bitcoin has not shown any signs of rising back over the $11,000.

In fact, Bitcoin even dipped below the $10,000 mark on several occasions this week, reaching back into price territory that has not been seen since late July.

Bitcoin’s movement down over the past several weeks seems to have vastly changed the narrative about where Bitcoin is headed next. Throughout much of August, Bitcoin’s reaches over $12k seemed to inspired analysts to think big: Bitcoin was headed toward $20,000, no, make that $50,000.

Now, the narrative around Bitcoin seems to have returned to whether Bitcoin can hold past the $10,000 mark.

However, the fall back towards $10,000 may not be entirely unwelcome. CoinTelegraph reported that “over the medium to long term, traders expect Bitcoin to recover and perceive the ongoing consolidation phase as a healthy pullback.”

In other words, this latest pullback could be the latest purge of speculative overbuying from the price of BTC. After all, the hold above $11k that took place throughout much of August may have brought buyers into the market who were exclusively interested in short-term gains.

Bitcoin Teeters on the Edge of $10k

On the other hand, the CME gap that was formed around the $9,700 mark last week still remains a threat. A ‘CME gap’ refers to a phenomenon in which Bitcoin markets make a sharp, sudden move outside of regular trading hours for CME’s Bitcoin futures markets, which results in a literal ‘gap’ in Bitcoin price charts.

Often when this happens, the Bitcoin price will eventually fall back to the level where the gap was originally formed. This retrace in the price of Bitcoin 'fills' the gap. Therefore, because the gap is around the $9700 zone, some analysts believe that Bitcoin is headed at least that low before any meaningful, long-term gains will be possible.

Although, there are some analysts who believe that Bitcoin is such a hot commodity that the gap may remain 'empty'.

Woo also added that “if so it'll be the first CME gap on daily candles that remains unfilled,” a point that was contested by several other Twitter users.

I'd say there's a fair chance this CME gap may not get filled, so far it's been front run for liquidity. Every dip snapped up.

Woo also tweeted a chart that indeed showed, when Bitcoin was headed for $9,700 earlier this week, buyers jumped on the BTC dip before it got too low.

BTC Bears May Be in the Majority

Still, while BTC may not be at a real risk of falling below $9700, some analysts do find the fact that Bitcoin seems unable to recapture the $10,500 resistance level concerning.

Indeed, while BTC bulls may be buying up Bitcoin when it begins to approach $9,700, Bitcoin bears seem to be consistently selling around $10,500. The fact that Bitcoin has been unable to surpass this level suggests that BTC bears may be in the majority this time around.

Still, while BTC has waffled between $9,800 and $10,500 for the past week, traders still seem to be uncertain where Bitcoin is headed next.

However, by Thursday, the picture looked quite different: around noon CET, data from Messari showed that 32 the 37 tokens were back in the green, including the tokens that had lost out worse, earlier in the week.

However today, DeFi markets are a mixed bag: over two-thirds of the DeFi assets tracked by Messari were back in the red.

The assets that were in the green showed relatively modest gains; Yearn.Finance led the pack with 24-hour increase of 13.76 percent, while Mainframe, Loopring and Gnosis followed closely behind with gains over 10 percentage points. 0x, Airswap, Synthetix, Terra, Cream, Blockmason, Kava, and Wrapped Nexus mutual were all in the green for less than 10 percentage points.

After Months of Red-Hot Gains, DeFi Tokens Seem to Be Cooling Down

While these kinds of gains may be significant in traditional markets, and even for other kinds of crypto assets, the DeFi space has been so hot for the last several months that any upward movement below 20 percent almost seems paltry.

Indeed, a number of DeFi assets have consistently made headlines throughout the course of the year for their eye-popping growth. For example, Finance Magnatesreported in August that the price of Band Protocol tokens had increased 6000 percent, and that Chainlink tokens had increased more than 659 percent since January 1st.

However, like Bitcoin, August seemed to be a bit of a high point for DeFi tokens, and while the DeFi space may be geared for gain in the long term, the DeFi space could be staring at a serious market correction, right in the face.

In fact, the correction already seems to have begun: earlier this week, crypto Twitter commentator @cryptounfolded pointed out that in addition to token prices, the total amount of value 'locked' in DeFi protocols had also taken a hit.

Indeed, on September 2nd, the total value locked peaked at over $9.5 billion before crashing to as low as $7.56 billion on Sunday, September 6th. At press time, the total value locked had fallen even further, sitting at $6.47 billion.

Ethereum Congestion May Be Contributing to DeFi Downfall

What is driving the prices down? In addition to the pressure to sell that may be rippling out from Bitcoin markets, DeFi may also be feeling the aftereffects of several recent incidents that took place over the course of the last 2 weeks.

In particular, assets that have ties to the Ethereum ecosystem may have been affected by a massive increase in transaction fees and decreases in transaction speeds during the first few days of this month.

Indeed, according to on-chain analytics firm, Glassnode, miners on the network earned over $500,000 in just 1 hour on September 1st. Around the same time, Ethereum network users reported transactions taking much longer than usual to complete.

The more traffic there is on the network, the more congested it becomes; as it becomes more congested, fees go up, and transaction times slow down. In the long term, this means that DeFi developers may be seeking alternatives to Ethereum.

SushiSwap Snafu, EMD Exit Scam May Be Contributing to DeFi Cooldown

Beyond Ethereum, the DeFi space was also marked by the SushiSwap saga that took place over last weekend, a series of events that had large swathes of the community accusing a popular new protocol of being an exit scam.

The trouble began on Saturday, when the pseudonymous founder of SushiSwap, known only as ‘Chef Nomi’, suddenly made the decision to sell all of his SUSHI tokens, which totaled roughly $13 million.

The move caused the token price to suddenly take a significant dive: after peaking at $11.27 on Tuesday, September 1st, SUSHI prices dropped to as low as $1.21 on Saturday. This led the crypto community to initially decry the project as an exit scam. Though, control of the protocol was eventually handed over to members of the DeFi community.

In addition to the SushiSwap incident, a liquidity mining DeFi project on the EOS network known as Emerald Mine (EMD) was accused of an exit scam.

While incidents of fraud have been relatively few and far between in the DeFi space, compared to the ICO space in late 2017, both incidents have been the subject of much controversy.

However, Corey Caplan, partner of the DeFi Money Market Foundation, pointed out to Finance Magnates that, though much less frequent, incidents of fraud in the DeFi space could be having a large impact.

“In any nascent sphere, a single entity’s failure or success can have an outsized effect on the entire space,” he said. “This is what happened with the SushiSwap snafu, but I don’t believe this incident should be viewed as an encapsulation of the entire DeFi ecosystem.”

Rachel is a self-taught crypto geek and a passionate writer. She believes in the power that the written word has to educate, connect and empower individuals to make positive and powerful financial choices. She is the Podcast Host and a Cryptocurrency Editor at Finance Magnates.

Deutsche Börse’s 360T Plugs Bitpanda Into FX Network to Channel Institutions Into Crypto

Featured Videos

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights