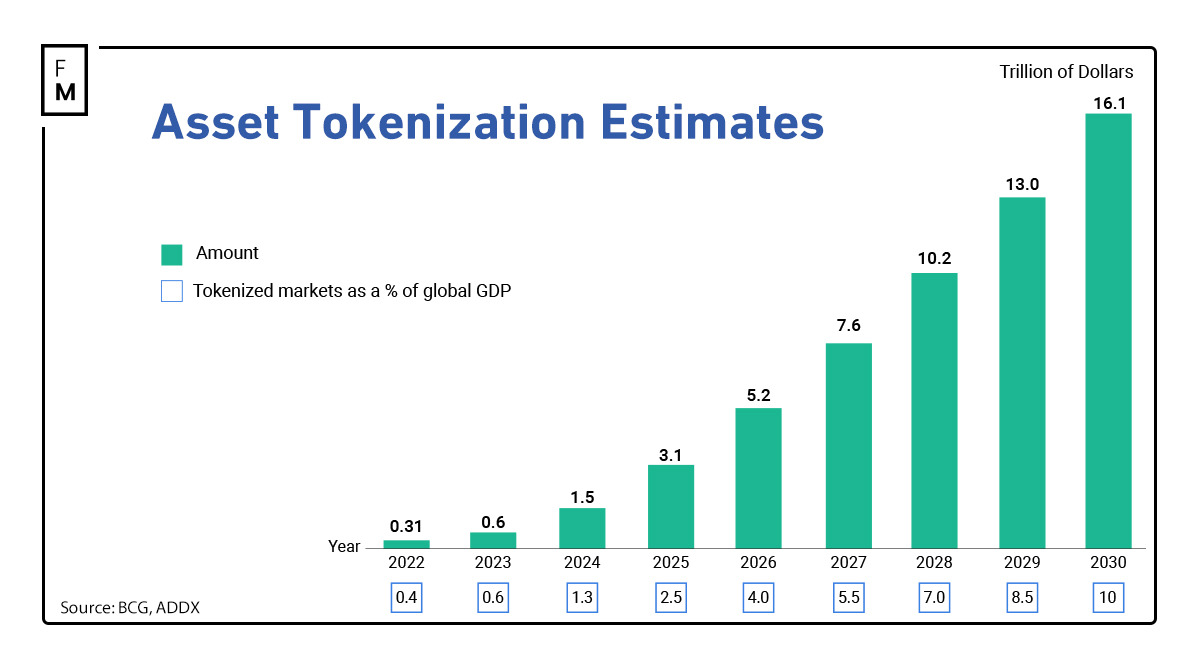

On the surface, institutional adoption of digital assets is thriving. The fact that multiple major firms like HSBC and BlackRock are beginning to offer tokenized products is a testament. One recent projection even suggested that by 2030 the tokenized asset market could go as high as $16.1 trillion.

Institutional participation has long been viewed as a necessary step for a larger mainstream adoption of digital assets, so the market is excited to welcome these new products. While this all sounds overwhelmingly positive, there is unfortunately still a significant hurdle that will need to be addressed before we see any broader acceptance and usage of digital assets: siloed liquidity.

The Walls Holding Back Adoption

Now, there are many different blockchain networks that, in most cases, don’t easily share resources. This ranges across public networks, private networks and sidechains, all of which struggle to move assets between them.

For example, JP Morgan has their own private blockchain, named Onyx. While JP Morgan is a massive, global firm and can certainly offer its customers services on this chain, it is still effectively walled off from larger public networks like Ethereum, as well as other institutional ones.

Compare this situation to the adoption of the internet around thirty years ago. It didn’t really take off until we had one “World Wide Web” that allowed access to all services via a single portal with no need to understand internet protocols. The whole of Web3 needs to work in just the same way to become functional for business.

Challenges and Considerations in Web3 Asset Transfers

In an attempt to address such issues, firms like Deutsche Bank have begun experimenting with ways to connect different institutional networks, and they are doing so via the creation of “bridges.”

Bridges aren’t entirely new to Web3, and they act as third parties that can transfer assets between different networks. However, there are some catches. Generally, bridging is a relatively expensive process to perform, usually incurring fees on both chains.

Furthermore, bridges are controlled by centralized operators, making these single points of failure among the most attack-prone elements of the modern Web3 landscape. While we have yet to see what Deutsche Bank will ultimately create, bridging is not usually a solution that financial institutions, or retail users for that matter, will find attractive. Fortunately, bridging isn’t the only option that is available.

A Universal Solution

Instead of a series of siloes, what is needed is a universal, interoperable layer that can connect liquidity across all of these networks, all without bridges that demand multiple hops and the related fees. Fortunately, this technology now exists, decades earlier than anyone thought possible.

Zero knowledge (ZK) technology allows for near-instant, cross-network transfers that are completely secure and cost almost nothing in transaction fees. This is possible because these protocols are able to generate a cryptographic “proof” that can confirm the veracity of any data, while never needing to reveal what that data is.

ZK proofs can allow for moving assets securely across networks without the need for any overly complex third-party protocols. The cryptography that powers these proofs means that instead of “bridging” assets, a single proof can be sent that ineffably confirms the veracity of any given transaction, all while using only a fraction of network resources.

Implementing a ZK powered interoperability layer will be the “aggregated” approach, and will be key to creating a Web3 space that feels like one single chain. Just like how the modern internet feels like a single service, all of the myriad of protocols and providers in the background simply merge into one experience for the end user.

This is what will bring a new wave of institutions and their products into this revolution by bringing down the barriers that are currently holding back broader institutional adoption.

By making the network that a given asset is built upon trivial, all liquidity would become unlocked across the entire Web3 ecosystem. This would be a much more attractive situation for institutions to launch new products into, and it would also draw in additional retail interest, further expanding the entire market. Web3 could finally realize the vision of an equitable, digital future, by being able to provide real financial tools that have no barriers or obstacles.