Shares of Bitcoin Investment Trust (OTCMKTS:GBTC) spent a good part of today trading below their fair value, an odd phenomenon for a security that investors have traditionally paid a premium for.

Units of the fund, when originally launched, represented one tenth of a bitcoin (accounting for the annual management fee of 2%, units now represent 0.09604763 BTC). The shares became the first publicly traded investment vehicle in bitcoin, gaining approval in March and debuting for trade in early May on the US OTC Markets.

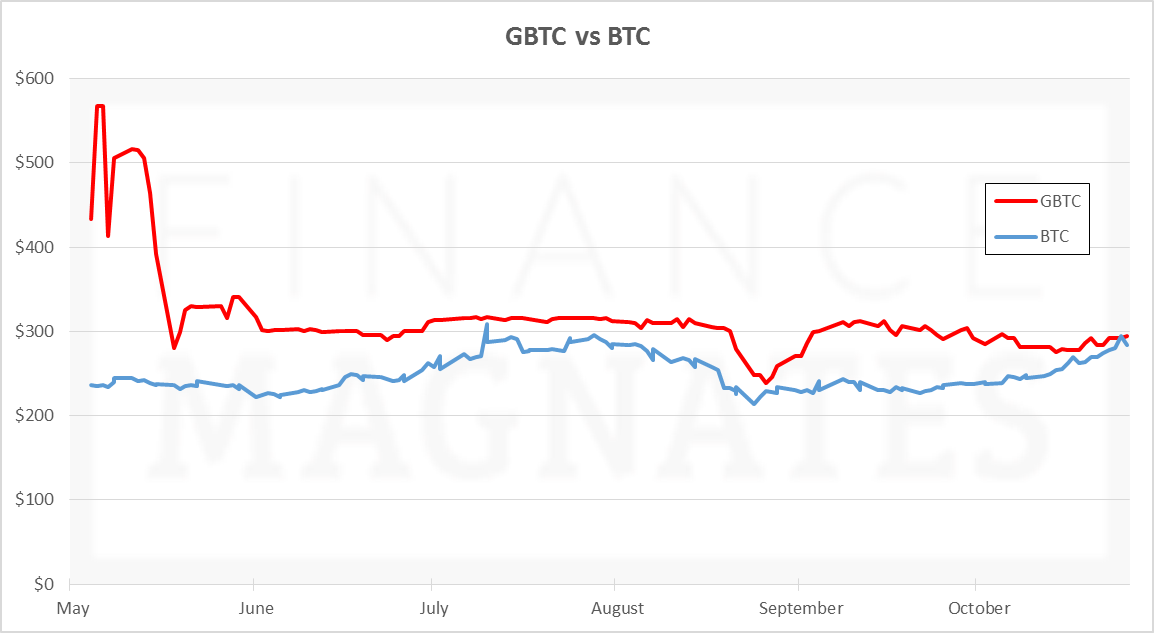

When GBTC first debuted for trade, investors were paying premiums of over 100% of bitcoin's value to get their hands on the coveted shares. After the first three weeks, the typical premium settled to between 10% and 25%. The assumption was that investors were willing to pay more to have some secure and regulated bitcoin exposure, and that they were enamored by the first such instrument of its kind.

Despite a monster weekend for bitcoin (BTC/USD) trading, during which bitcoin shot as high as $296 and came into Monday morning hovering near $285, shares of GBTC continued unchanged at $28.00 (representing a premium of only 1.9% to bitcoin's value) for nearly two hours after trading commenced this morning. After briefly jumping to $28.95, they fell as low as $26.68, which translates into a 2.5% discount relative to bitcoin's value.

The shares spent most of the afternoon at $27.25 or $27.35 (discounts of 0.4% and 0.8%, respectively). They jumped to $28.32 as trading closed, bringing them back to a premium of 3.8%.

The shares thus spent nearly half the day trading below the value of their underlying bitcoin, and most of the other half at historically low premium levels.

Today was the first example of such behavior in the shares' brief public history, and continues a trend of GBTC's shrinking edge over its underlying asset. Instances such as this past weekend, where GBTC's last closing price was 1.2% less than bitcoin, as well as that of July 12, when bitcoin soared on Grexit fears, are not counted since GBTC is not traded on weekends.

When we last examined the disappearing premium, we focused on the dissipation of the initial hype and the emergence of other regulated avenues for gaining bitcoin exposure, which lessen GBTC's appeal.

Worth Investing?

What has also become apparent is the limited supply of shares for secondary trading. While this can, and has, contributed to a shortage in supply and upward pressure on the traded price, it may also be contributing to outsized swings in the other direction.

Investors who have snapped up the shares for the long haul have no intention of selling any time soon, possibly even in Arbitrage situations. The bid/ask price spread has occasionally grown to $1.00, or 4%, as observed by the lengthy stretches of dormancy followed by swings of such magnitude. The lack of sellers may have also motivated buyers to head for the exits, knocking off top bids from the order book and leading to seemingly irrational trades.

It is worth noting, however, that today's volume of 12,736 shares was the highest since mid-July, and roughly 6x the 30-day average.

Also worth considering is how much investors are willing to pay for a security that automatically loses 2% of its bitcoin-based value per annum due to management fees. The fund is passively managed. The main value-add is the security of the bitcoins, which are stored by Xapo and are insured for certain types of loss. Over the long term, bitcoin will have to produce sufficient returns to justify the fees. After ten years, only 81.7% of the original bitcoin investment remains.

It is therefore understandable if investors begin attributing discounted value to the shares, especially if cheaper regulated alternatives exist.

A large investor in GBTC shares, who spoke to Finance Magnates on condition of anonymity, expressed concern over how the shares will track their underlying bitcoin in the long-term. His bitcoin holdings have been profitable, but his GBTC positions have now underperformed. Ultimately, however, he believes that the discounted valuations present a good buying opportunity.

Correction: An earlier version of this article stated that each share of GBTC represents one tenth of a bitcoin. In fact, the value was originally 0.1 BTC, but accounting for the 2% management fee, has been decreasing periodically and is currently 0.09604763 BTC. The figures in the article have been recalculated accordingly.

The ~0.8% reduction in GBTC value between May and October that is attributable to the 2% fee is still grossly insufficient to account for the total reduction in GBTC’s relative value, as observed in the charts. The article’s claims of historically low/negative premium levels on October 26 are therefore maintained.