Investment crowdfunding can be a highly effective method of sourcing seed money to launch a start-up.

FM

This article was written by Adinah Brown from Leverate.

A darling of 21st century financial trends, most of us have heard of crowdfunding, where projects and charities get funded by lots of people who think that an idea has great potential. However, what fewer people know about is investment crowdfunding, where a company sources funds by getting a large pool of backers to invest relatively small amounts of money into a shared project, company or business venture.

For an entrepreneur, investment crowdfunding can be a highly effective method of sourcing seed money to launch a start-up or project, particularly when more traditional means of raising funds, such bank loans and venture capital, are not available, too restrictive or too costly.

From the perspective of investors, it enables them to access potentially high returns from an investment, but without the enormous capital that is otherwise required.

This structure of investment crowdfunding has entailed that investment opportunities that were previously only available to the super wealthy, are now available to the masses. This democratizing of finance means that many individual investments require an initial outlay of anywhere between $100 to $50,000, which is a far cry from the millions of dollars that is necessary in a traditional investment structure.

In this article we list the most common forms of investment crowdfunding that have taken root and look set to rise.

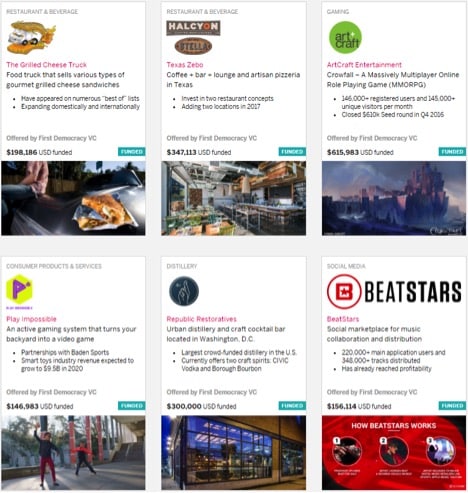

Crowd Equity

Equity crowdfunding provides an investor with a stake in a company that they have decided to financial support. Often the companies are innovative start-ups with fresh ideas that they are looking to get off the ground.

This crowdfunding option gives you ownership of a portion of the company and in terms of risk, you go along for the ride, whether that be skyrocketing success or a plummeting failure.

To help mitigate the risk of crowd equity there are a few things to be aware of:

Is the platform investor-led or entrepreneur-led? In entrepreneur led platforms, it’s the people seeking funding that set the investment terms, including the share price and the amount of equity that is to be sold off. In investor led platforms, a lead investor will negotiate the terms contributing to better terms for all other subsequent investors.

Does it have pre-emption rights? To protect your purchase from being diluted out, shares need to be sold with pre-emption rights so that their value does not decrease from subsequent funding rounds. Remember the movie ‘The Social Network’ where Facebook diluted the shareholding of Eduardo Saverin, one of its early founders, from 30% to just 0.5%? Yeah, you don’t want that to happen to you.

Crowd equity can start for as little as $10 for a very early stage start-up, however for more established companies, shares are sold for a few thousand dollars. Depending on the structure, the start-up may choose to set the minimum amount that they are willing to accept.

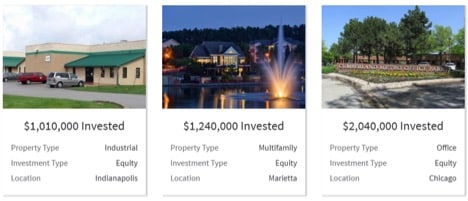

Crowd Real Estate

Moving in to the crowdfunding neighborhood is real estate. In 2016 crowd real estate funding grew beyond $3.5 billion, and by 2025 it is anticipated to be valued at more than $300 billion, as online real estate firms are expected to maximize on this development.

The beneficiaries of this innovative model are both sellers and buyers. For sellers, crowd real estate dramatically reduces the cost of selling a property whilst casting a much wider net of potential buyers. For buyers, crowd real estate provides investment opportunities that were previously only available to those with mega funds.

With a number of different platforms available online, individual investors choose a property from amongst a variety of different projects listed on a website, some of which may ask for as little as $5,000 and then go up to a maximum of $100,000.

Depending on the platform, there is usually management on the ground that organizers all the conveyancing, legal fees and any upgrades or renovations that are needed. Investors are provided with data to help inform their decision, such as the estimated return on investment, the investment duration and sometimes the details of other parties also involved in the investment. As soon as the investment is secured, the investor can start accruing interest.

The industry offers no shortage of variety, and investors are able to choose between single family homes, a building of condominiums and even multi-purpose manufacturing warehouses.

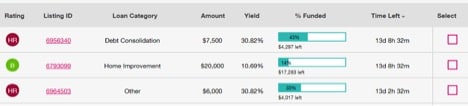

With all that said, the investor still carries the risk and needs to be aware at the outset, of the extent of risk being taken on. This means being aware of the interest rate, the length of the loan, the credit rating of the borrowing company and the nature of the company.

For their loan, investors tend to receive an interest rate that is higher than other debt instruments to counter the credit risk associated with the borrower. Also, to help mitigate risk, investors can spread their capital incrementally over multiple loans from different companies.

The range of crowd bonds has become quite extensive and varied, with bonds issued by care homes, solar farms, hydroelectric power station and pubs. The returns of the bonds are usually at a fixed rate of anywhere between 4 to 7 per cent and at a range of maturities, from 5 to 19 years.

This article was written by Adinah Brown from Leverate.

A darling of 21st century financial trends, most of us have heard of crowdfunding, where projects and charities get funded by lots of people who think that an idea has great potential. However, what fewer people know about is investment crowdfunding, where a company sources funds by getting a large pool of backers to invest relatively small amounts of money into a shared project, company or business venture.

For an entrepreneur, investment crowdfunding can be a highly effective method of sourcing seed money to launch a start-up or project, particularly when more traditional means of raising funds, such bank loans and venture capital, are not available, too restrictive or too costly.

From the perspective of investors, it enables them to access potentially high returns from an investment, but without the enormous capital that is otherwise required.

This structure of investment crowdfunding has entailed that investment opportunities that were previously only available to the super wealthy, are now available to the masses. This democratizing of finance means that many individual investments require an initial outlay of anywhere between $100 to $50,000, which is a far cry from the millions of dollars that is necessary in a traditional investment structure.

In this article we list the most common forms of investment crowdfunding that have taken root and look set to rise.

Crowd Equity

Equity crowdfunding provides an investor with a stake in a company that they have decided to financial support. Often the companies are innovative start-ups with fresh ideas that they are looking to get off the ground.

This crowdfunding option gives you ownership of a portion of the company and in terms of risk, you go along for the ride, whether that be skyrocketing success or a plummeting failure.

To help mitigate the risk of crowd equity there are a few things to be aware of:

Is the platform investor-led or entrepreneur-led? In entrepreneur led platforms, it’s the people seeking funding that set the investment terms, including the share price and the amount of equity that is to be sold off. In investor led platforms, a lead investor will negotiate the terms contributing to better terms for all other subsequent investors.

Does it have pre-emption rights? To protect your purchase from being diluted out, shares need to be sold with pre-emption rights so that their value does not decrease from subsequent funding rounds. Remember the movie ‘The Social Network’ where Facebook diluted the shareholding of Eduardo Saverin, one of its early founders, from 30% to just 0.5%? Yeah, you don’t want that to happen to you.

Crowd equity can start for as little as $10 for a very early stage start-up, however for more established companies, shares are sold for a few thousand dollars. Depending on the structure, the start-up may choose to set the minimum amount that they are willing to accept.

Crowd Real Estate

Moving in to the crowdfunding neighborhood is real estate. In 2016 crowd real estate funding grew beyond $3.5 billion, and by 2025 it is anticipated to be valued at more than $300 billion, as online real estate firms are expected to maximize on this development.

The beneficiaries of this innovative model are both sellers and buyers. For sellers, crowd real estate dramatically reduces the cost of selling a property whilst casting a much wider net of potential buyers. For buyers, crowd real estate provides investment opportunities that were previously only available to those with mega funds.

With a number of different platforms available online, individual investors choose a property from amongst a variety of different projects listed on a website, some of which may ask for as little as $5,000 and then go up to a maximum of $100,000.

Depending on the platform, there is usually management on the ground that organizers all the conveyancing, legal fees and any upgrades or renovations that are needed. Investors are provided with data to help inform their decision, such as the estimated return on investment, the investment duration and sometimes the details of other parties also involved in the investment. As soon as the investment is secured, the investor can start accruing interest.

The industry offers no shortage of variety, and investors are able to choose between single family homes, a building of condominiums and even multi-purpose manufacturing warehouses.

With all that said, the investor still carries the risk and needs to be aware at the outset, of the extent of risk being taken on. This means being aware of the interest rate, the length of the loan, the credit rating of the borrowing company and the nature of the company.

For their loan, investors tend to receive an interest rate that is higher than other debt instruments to counter the credit risk associated with the borrower. Also, to help mitigate risk, investors can spread their capital incrementally over multiple loans from different companies.

The range of crowd bonds has become quite extensive and varied, with bonds issued by care homes, solar farms, hydroelectric power station and pubs. The returns of the bonds are usually at a fixed rate of anywhere between 4 to 7 per cent and at a range of maturities, from 5 to 19 years.

Technology Providers Bring Event-Based Trading to Brokers

Featured Videos

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights