This article was written by Sonny Singh, CCO of Bitpay.

Sonny Singh

The recent high profile fundings of Robinhood and Stripe have led many to believe it’s very easy for companies to raise venture capital. Unfortunately, this does not always seem to be the case, especially for Fintech companies.

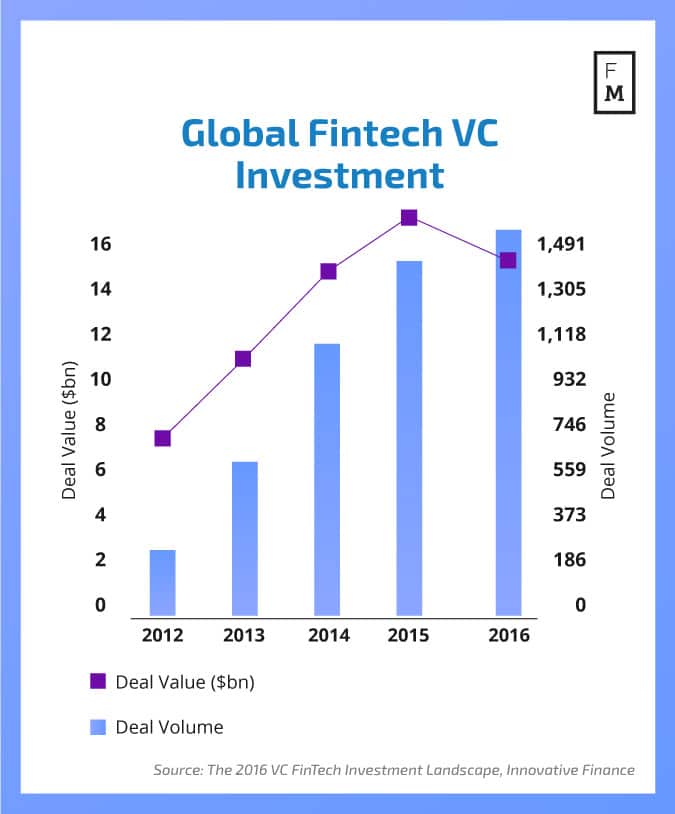

In 2016, the total number of funded deals dropped to 1,436 from its previous-year high of 1,617. According to CB Insights, seed investments made up 29 percent of the deals in 2016—down from 35 percent the year before —while Series D investments rose to 7 percent.

Over the last year, I’ve met with several fintech founders who attested to the trouble they’ve been having trying to raise a seed round. I started to see many common trends and problems the founders were encountering.

1. First Time Founders

Most founders I met with were first time founders from large financial institutions that have limited experience in technology, venture capital, or even the Silicon Valley ecosystem. This type of founder was new to the concept of raising venture capital. They want to set up meetings with the large traditional Silicon Valley VCs and assume it would be easy to get funding with just a powerpoint presentation. They are surprised to learn that VCs invest in about 1-2% of the companies they meet with.

I need to explain that normally the first money in a seed round comes from friends and family, and former employers or advisors. I also encourage them to look at joining fintech incubators like 500 Startups, Wells Fargo, Plug and Play, and Yodlee, as these incubators provide great training for first time founders.

2. Not a Billion-Dollar Idea

Most founders I meet with admit that their company does not have the market opportunity to become a $1 billion company. Their companies are solving specific point solutions in industries like remittance, payment fraud, or gift cards. They are excited and believe the company could grow very quickly to a $100 or $200 million valuation, and could be cash-flow positive. However, they are surprised and disappointed to learn that VCs look to invest in companies that have the potential for a $1 billion exit.

I tell them that most businesses do not need venture capital funding: a $200 million company is an amazing accomplishment, and they should continue down that path regardless of getting venture capital. Getting customer traction should be the top priority.

3. Most VCs Lack Fintech Expertise

Most traditional venture firms do not have employees with fintech operating experience, and the corporate venture arms like Citi Ventures and AMEX Ventures prefer to invest in later stage companies. This makes it very challenging for founders trying to pitch their ideas when the VCs have limited knowledge in their space. Also, the VCs don’t understand all the regulations around international banking laws, PCI Compliance , AML/KYC, money transmitter licenses, etc.

4. Regulations and Compliance

While the VC might not understand all the regulations and compliance issues, the founder does—and unfortunately still underestimates how much time and cost is required for compliance. At the large banks where these founders once worked, compliance is an issue, but they have large teams dedicated to it. Compliance quickly becomes the top priority for startups, and it will require the most headcount and legal expenses. If you’re handling credit card data, then you need to be PCI compliant; if you’re sending money, you need to get money transmitter licenses (MTLs) for each state. In real estate, lenders need to get licensed by state—which is why most of the real estate startups, like Lending Home, SoFI, or Poynt, are not yet licensed to operate throughout all 50 states.

5. Slow Sales Cycle

A lot of times the founder will show potential investors a large pipeline of partnerships they expect to close with large banks. Unfortunately, the founder underestimates the time it takes to close these deals which slows down the fund raising process. As a result, the investors keep waiting while the founder starts to burn cash trying to close the big deal.

Summary

Fortunately, all is not lost for fintech founders. They just need to do some homework on their business model and decide if and when they should raise venture capital. There are many successful companies that have sold for hundreds of millions of dollars without ever having raised venture capital. My advice is to build up a good network of advisors, raise a friends-and-family round, and start gaining customer traction as soon as possible.