Revolut has up to 12 months to exit the ‘mobilisation’ stage.

The fintech will continue to offer services as a payment institution while it is in the ‘mobilisation’ stage.

Revolut's plans for a Western Europe HQ show the company banking on the EU.

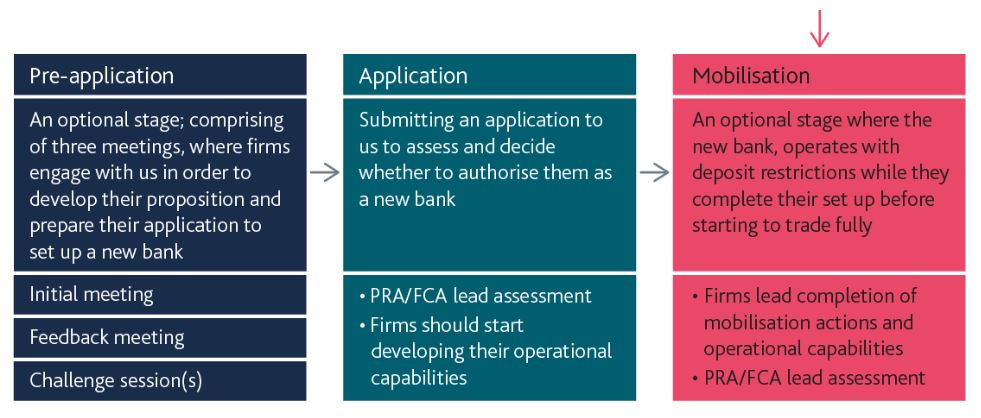

Revolut, the largest fintech by valuation, has received a banking licence in its home country, the United Kingdom. However, the licence is currently in the ‘mobilisation’ stage, also referred to as ‘Authorisation with Restrictions’.

The London-headquartered fintech pointed out that many new banks, including challenger banks like Monzo, Starling, Atom Bank, Zopa Bank, GB Bank, and Kroo, have gone through a similar ‘mobilisation’ stage.

An ‘Optional’ Route

According to the Bank of England’s ‘new bank authorisation process’ guide, the “mobilisation route is optional.”

“Mobilisation should not be seen as the stage to commence a firm’s bank-building strategies, processes, and systems, but rather a route which allows new banks extra time to finalise and deliver the development of their banks, i.e., IT infrastructure, governance, and risk management frameworks, with the benefit of being authorised,” the guide explained.

“As mobilisation is intended to complete the build-out of the bank, we do not expect firms to make material changes to their strategy or individuals during mobilisation.”

Stages of the authorisation process (mobilisation); Source: Bank of England

When in the mobilisation state, one of the major restrictions on the banking licence recipient is the £50,000 annual deposit limit by customers. Revolut will circumvent these restrictions by continuing to offer services to UK residents under the existing e-money institution licence authorised by the Financial Conduct Authority.

A 12-Month Deadline

The Bank of England, in its guide, further highlighted that the mobilisation stage must be ended within 12 months. Further, the PRA and FCA set a list of mobilisation conditions for new banking licence holders entering mobilisation state for this exit from the stage.

“A Variation of Permission application for banks to exit mobilisation shall be required to be made at least three months prior to the expiration of the 12-month mobilisation period to allow sufficient time for the regulatory assessment,” the guide added.

During the mobilisation period, the new banking licence holders also attempted to secure further investments. Although Revolut did not publicise any fundraising plans, it is considering a secondary share sale round for its employee shareholders, aiming at a valuation of $45 billion. The fintech’s CEO, Nik Storonsky, will also reportedly offload a significant chunk of his stake in the company.

New Products Are Coming for Revolut Customers

The UK is the largest market for Revolut, with 9 million customers compared to the global 45 million customers. It has been operating as a payment institution in the UK since its establishment in 2015. However, it operates as a bank with a licence from Lithuania in the European Union. It also obtained a banking license in Mexico earlier this year.

As a bank in the UK, Revolut can now offer lending products, which it could not as a payment institution. Further, when Revolut starts operating as a bank in the UK, each customer’s deposits will be protected up to £85,000 under the Financial Services Compensation Scheme (FSCS).

Meanwhile, Revolut has been focused on expanding services outside the UK as well. Recently, it partnered with CMC Markets to offer contracts for differences (CFDs) products to its customers. However, it has terminated services under the “Lite” brand in many emerging markets.

Revolut, the largest fintech by valuation, has received a banking licence in its home country, the United Kingdom. However, the licence is currently in the ‘mobilisation’ stage, also referred to as ‘Authorisation with Restrictions’.

The London-headquartered fintech pointed out that many new banks, including challenger banks like Monzo, Starling, Atom Bank, Zopa Bank, GB Bank, and Kroo, have gone through a similar ‘mobilisation’ stage.

An ‘Optional’ Route

According to the Bank of England’s ‘new bank authorisation process’ guide, the “mobilisation route is optional.”

“Mobilisation should not be seen as the stage to commence a firm’s bank-building strategies, processes, and systems, but rather a route which allows new banks extra time to finalise and deliver the development of their banks, i.e., IT infrastructure, governance, and risk management frameworks, with the benefit of being authorised,” the guide explained.

“As mobilisation is intended to complete the build-out of the bank, we do not expect firms to make material changes to their strategy or individuals during mobilisation.”

Stages of the authorisation process (mobilisation); Source: Bank of England

When in the mobilisation state, one of the major restrictions on the banking licence recipient is the £50,000 annual deposit limit by customers. Revolut will circumvent these restrictions by continuing to offer services to UK residents under the existing e-money institution licence authorised by the Financial Conduct Authority.

A 12-Month Deadline

The Bank of England, in its guide, further highlighted that the mobilisation stage must be ended within 12 months. Further, the PRA and FCA set a list of mobilisation conditions for new banking licence holders entering mobilisation state for this exit from the stage.

“A Variation of Permission application for banks to exit mobilisation shall be required to be made at least three months prior to the expiration of the 12-month mobilisation period to allow sufficient time for the regulatory assessment,” the guide added.

During the mobilisation period, the new banking licence holders also attempted to secure further investments. Although Revolut did not publicise any fundraising plans, it is considering a secondary share sale round for its employee shareholders, aiming at a valuation of $45 billion. The fintech’s CEO, Nik Storonsky, will also reportedly offload a significant chunk of his stake in the company.

New Products Are Coming for Revolut Customers

The UK is the largest market for Revolut, with 9 million customers compared to the global 45 million customers. It has been operating as a payment institution in the UK since its establishment in 2015. However, it operates as a bank with a licence from Lithuania in the European Union. It also obtained a banking license in Mexico earlier this year.

As a bank in the UK, Revolut can now offer lending products, which it could not as a payment institution. Further, when Revolut starts operating as a bank in the UK, each customer’s deposits will be protected up to £85,000 under the Financial Services Compensation Scheme (FSCS).

Meanwhile, Revolut has been focused on expanding services outside the UK as well. Recently, it partnered with CMC Markets to offer contracts for differences (CFDs) products to its customers. However, it has terminated services under the “Lite” brand in many emerging markets.

Arnab is an electronics engineer-turned-financial editor. He entered the industry covering the cryptocurrency market for Finance Magnates and later expanded his reach to forex as well. He is passionate about the changing regulatory landscape on financial markets and keenly follows the disruptions in the industry with new-age technologies.

eToro Launches Long-Term Thematic Portfolio Using Amundi ETFs for Retail Investors

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights