FCA wants to see more competition in the open banking services industry.

Seven million Britons currently use the UK’s open banking products.

Bloomberg

The Joint

Regulatory Oversight Committee (JROC), which is co-led by the Financial Conduct

Authority (FCA) and the Payment Systems Regulator (PSR), has released its

proposed guidelines for the upcoming stage of open banking in the United

Kingdom.

Currently,

the open banking services and products have reached more than 7 million

consumers in the UK. The Committee wants this number to increase, promoting

open banking to consumers and using fintech companies' apps in the coming years.

JROC Unveils Two-Year Open

Banking Development Plan

JROC was

established with the cooperation of the FCA and the PSR in March 2022, and its

main purpose is to oversee planning and preparation for the creation of a

future open banking entity and the transition to the future framework.

The term 'open

banking' pertains to the utilization of banking data from clients at

established financial institutions by third-party companies to provide

customized services like lending and payments. This industry has contributed to

the transformation of the UK's fintech sector into the third largest in the

world.

More than a

year after its establishment, JROC has published recommendations presenting the

next phase of open banking development in the islands. Among the recommended

steps were proposals to develop a scalable, secure and economically sustainable

system.

To do that,

JROC has laid out a roadmap of priorities for the next two years in the UK's

open banking sector. The roadmap is focused on five key themes: leveling up

availability and performance, mitigating the risks of financial crime, ensuring

effective consumer protection, improving information flows to third-party

providers (TPPs) and end users, and promoting additional services. As part of

the roadmap, the JROC plans to pilot non-sweeping variable recurring payments

(VRP) to explore new payment models. The recommendations are aimed at creating

a more secure and inclusive open banking ecosystem in the UK.

"Open

banking can be a UK success story and we want to help it grow and develop

sustainably. Today's report sets out a roadmap and the framework for delivering

the next phase of open banking," the Co-Chairs of the Committee, PSR's

Managing Director, Chris Hemsley, and the FCA's Executive Director of Consumers and

Competition, Sheldon Mills, said in the statement.

"Only

through effective collaboration can we deliver on our ambition and develop open

banking in a way that promotes continued innovation and competition, for the

benefit of consumers, businesses, and the wider economy," the statement

added.

The JROC

has outlined its vision for the future of open banking and identified the

necessary steps required in its design. This includes a transition from the

current Open Banking Implementation Entity (OBIE) to the new entity that will

build on the substantial progress achieved so far.

"Britain

leads the pack in open banking, with 7 million users, but we can't sit back and

put our feet up," Andrew Griffith, the City Minister, said. "Today's plan

will deliver a new generation of products and services, making banking more

accessible and convenient for millions of people."

The JROC

will collaborate with industry stakeholders and oversee progress towards the

five key themes and the design of the future entity. They will provide a

progress report in Q4 2023 and a detailed plan for the transition from OBIE to

the future entity. The roadmap's full timetable is outlined

in the publication.

What Is the Future of Open

Banking?

After

Brexit, the UK is eager to advance open banking to draw in more fintech

companies, especially since the European Union is preparing to launch its own

comprehensive open banking scheme. While regulators have praised the successful

implementation of open banking technology in the UK fintech industry, industry

leaders cautioned against becoming too complacent.

According

to Chris Hayward, the Policy Chief at the City of London Corporation, which manages

London's financial district, the UK's fintech industry ranks third worldwide,

with a total investment of $12.5 billion in 2022, following the United States

and China.

Fintechs

and challenger banks are

projected to grow in the coming years. According to Business Insider

Intelligence, digital banks will have over 75 million subscribers in the United

States alone by 2023. This indicates a 25% growth over the current user base.

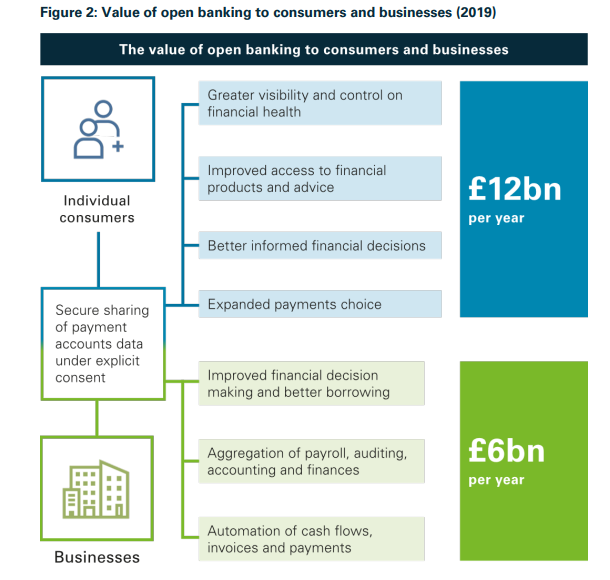

Value of open banking to consumers and businesses (2019). Source: Gov.uk

API

integration is a significant focus in the industry, involving linking

various software systems via APIs. APIs enable secure and efficient sharing of

data between software systems. Within banking, API integration facilitates the

exchange of consumer data among different financial institutions and enables

the creation of innovative new services.

The Global

Opportunity Analysis and Industry Forecast report states that the size of the

global online banking market was worth $11.43 billion in 2019 and is

expected to grow to $31.81 billion by 2027.

FCA Wants Greater Investor

Protection

In the

meantime, the FCA has released its business plan for 2023-2024, outlining its

roadmap for the next 12 months in accordance with the three-year development

strategy introduced a year ago. Its primary objective is to enhance overall

investor protection.

Meanwhile,

the UK is taking steps to prepare for cryptocurrency regulation by launching a

public consultation to create a draft law on regulating digital assets.

To further

bolster the safety of retail traders, the UK financial market supervisor has

appointed joint Executive Directors of Enforcement and Market Oversight, Steve

Smart and Therese Chambers, following Mark Steward's retirement in October last

year.

Additionally,

the FCA and the Advertising Standards Authority (ASA) have collaborated on a

campaign to educate financial influencers and prevent the promotion of illegal

'get rich quick' schemes. The agencies have partnered with prominent social

media influencer Sharon Gaffka.

Furthermore, the FCA is actively expanding its regulatory efforts, as evidenced by its rejection

of 8,582 financial promotions in 2022, seeking their amendment or removal by

authorized firms, which is an increase of 1,400% from the 573 financial promotions it

rejected in 2021.

The Joint

Regulatory Oversight Committee (JROC), which is co-led by the Financial Conduct

Authority (FCA) and the Payment Systems Regulator (PSR), has released its

proposed guidelines for the upcoming stage of open banking in the United

Kingdom.

Currently,

the open banking services and products have reached more than 7 million

consumers in the UK. The Committee wants this number to increase, promoting

open banking to consumers and using fintech companies' apps in the coming years.

JROC Unveils Two-Year Open

Banking Development Plan

JROC was

established with the cooperation of the FCA and the PSR in March 2022, and its

main purpose is to oversee planning and preparation for the creation of a

future open banking entity and the transition to the future framework.

The term 'open

banking' pertains to the utilization of banking data from clients at

established financial institutions by third-party companies to provide

customized services like lending and payments. This industry has contributed to

the transformation of the UK's fintech sector into the third largest in the

world.

More than a

year after its establishment, JROC has published recommendations presenting the

next phase of open banking development in the islands. Among the recommended

steps were proposals to develop a scalable, secure and economically sustainable

system.

To do that,

JROC has laid out a roadmap of priorities for the next two years in the UK's

open banking sector. The roadmap is focused on five key themes: leveling up

availability and performance, mitigating the risks of financial crime, ensuring

effective consumer protection, improving information flows to third-party

providers (TPPs) and end users, and promoting additional services. As part of

the roadmap, the JROC plans to pilot non-sweeping variable recurring payments

(VRP) to explore new payment models. The recommendations are aimed at creating

a more secure and inclusive open banking ecosystem in the UK.

"Open

banking can be a UK success story and we want to help it grow and develop

sustainably. Today's report sets out a roadmap and the framework for delivering

the next phase of open banking," the Co-Chairs of the Committee, PSR's

Managing Director, Chris Hemsley, and the FCA's Executive Director of Consumers and

Competition, Sheldon Mills, said in the statement.

"Only

through effective collaboration can we deliver on our ambition and develop open

banking in a way that promotes continued innovation and competition, for the

benefit of consumers, businesses, and the wider economy," the statement

added.

The JROC

has outlined its vision for the future of open banking and identified the

necessary steps required in its design. This includes a transition from the

current Open Banking Implementation Entity (OBIE) to the new entity that will

build on the substantial progress achieved so far.

"Britain

leads the pack in open banking, with 7 million users, but we can't sit back and

put our feet up," Andrew Griffith, the City Minister, said. "Today's plan

will deliver a new generation of products and services, making banking more

accessible and convenient for millions of people."

The JROC

will collaborate with industry stakeholders and oversee progress towards the

five key themes and the design of the future entity. They will provide a

progress report in Q4 2023 and a detailed plan for the transition from OBIE to

the future entity. The roadmap's full timetable is outlined

in the publication.

What Is the Future of Open

Banking?

After

Brexit, the UK is eager to advance open banking to draw in more fintech

companies, especially since the European Union is preparing to launch its own

comprehensive open banking scheme. While regulators have praised the successful

implementation of open banking technology in the UK fintech industry, industry

leaders cautioned against becoming too complacent.

According

to Chris Hayward, the Policy Chief at the City of London Corporation, which manages

London's financial district, the UK's fintech industry ranks third worldwide,

with a total investment of $12.5 billion in 2022, following the United States

and China.

Fintechs

and challenger banks are

projected to grow in the coming years. According to Business Insider

Intelligence, digital banks will have over 75 million subscribers in the United

States alone by 2023. This indicates a 25% growth over the current user base.

Value of open banking to consumers and businesses (2019). Source: Gov.uk

API

integration is a significant focus in the industry, involving linking

various software systems via APIs. APIs enable secure and efficient sharing of

data between software systems. Within banking, API integration facilitates the

exchange of consumer data among different financial institutions and enables

the creation of innovative new services.

The Global

Opportunity Analysis and Industry Forecast report states that the size of the

global online banking market was worth $11.43 billion in 2019 and is

expected to grow to $31.81 billion by 2027.

FCA Wants Greater Investor

Protection

In the

meantime, the FCA has released its business plan for 2023-2024, outlining its

roadmap for the next 12 months in accordance with the three-year development

strategy introduced a year ago. Its primary objective is to enhance overall

investor protection.

Meanwhile,

the UK is taking steps to prepare for cryptocurrency regulation by launching a

public consultation to create a draft law on regulating digital assets.

To further

bolster the safety of retail traders, the UK financial market supervisor has

appointed joint Executive Directors of Enforcement and Market Oversight, Steve

Smart and Therese Chambers, following Mark Steward's retirement in October last

year.

Additionally,

the FCA and the Advertising Standards Authority (ASA) have collaborated on a

campaign to educate financial influencers and prevent the promotion of illegal

'get rich quick' schemes. The agencies have partnered with prominent social

media influencer Sharon Gaffka.

Furthermore, the FCA is actively expanding its regulatory efforts, as evidenced by its rejection

of 8,582 financial promotions in 2022, seeking their amendment or removal by

authorized firms, which is an increase of 1,400% from the 573 financial promotions it

rejected in 2021.

Damian's adventure with financial markets began at the Cracow University of Economics, where he obtained his MA in finance and accounting. Starting from the retail trader perspective, he collaborated with brokerage houses and financial portals in Poland as an independent editor and content manager. His adventure with Finance Magnates began in 2016, where he is working as a business intelligence analyst.

Singapore Goes Nearly Cashless, Now Eyes Cross-Border Payments, Stablecoins and FX

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights