Buy now, pay later, also known as BNPL, has become very popular among retail consumers. The process of receiving interest-free payment installments has opened an easy credit line to consumers for online shopping, flight booking, hotel reservations, and numerous other services.

However, as of today, the industry is mainly operating without any regulations. The lack of widespread regulation has exposed the sector to high levels of fraud and distress to borrowers, saddling some with unaffordable debts, and thus attracting the attention of market regulators.

The industry is prone to two basic types of fraud. One is called synthetic identity fraud with which scammers join bits and pieces of consumers' stolen identities to lend on behalf of them, while the other is account takeover of legitimate BNPL customers. Though data on BNPL frauds are scarce, a report by anti-fraud company Sift revealed that fraud attacks on such fintech platforms went up by 54 percent year over year.

The situation is also grim in the UK as a survey found that a third of British BNPL consumers are facing 'unmanageable' troubles in repayment of installments with rising costs of living, putting them in a debt spiral. Many UK citizens, mostly the young generation, went on shopping sprees with the easy credit line, but later found themselves in massive debts.

Citizens Advice, an independent organization in the UK helping people with debt, found that 51 percent of 18 to 34-year-olds in the UK have BNPL debts, compared to 39 percent in the age group of 35 to 54 years and 24 percent of 55 years and above. It also cited the example of a 32-year-old who bought £600 worth of clothes using a BNPL firm to pay in installments. Though she did not receive the goods and canceled the payments, she was "barraged with calls, emails, and letters from a debt collector - all for buying some clothes online."

Upcoming Regulations

Surprisingly, the United Kingdom government came out as one of the first to bring regulations to this booming but unregulated sector. The government is planning to mandate lenders to carry out affordability checks, ensuring that the loans are affordable. Further, there will be curbs on promotion rules for BNPL services.

Also, the lenders in the UK offering BNPL services have to take the approval of the Financial Conduct Authority (FCA ). It will allow borrowers to take complaints to the Financial Ombudsman Service (FOS).

“By holding Buy-Now Pay-Later to the high standards we expect of other loans and forms of credit, we are protecting consumers and fostering the safe growth of this innovative market in the UK,” said John Glen, the Economic Secretary of the UK Treasury.

While there is chatter among other regulators on bringing restrictions around BNPL, the UK has released its plans. However, these are still in the consultation stage, and the UK government is planning to publish draft legislation towards the end of this year.

“BNPL platforms operate within a current exemption to regulation (Article 60F(2) to the Regulated Activities Order 2001), which exempts certain types of interest-free credit agreements. The exemption was not meant for the retail market, and one of the concerns is that this easy access to interest-free credit will cause consumers to over-borrow,” Remonda Kirketerp-Moller, the Founder and CEO, Muinmos explained.

A Popular Fintech Niche

The rise of the BNPL services was astonishing. The industry grew from $33 billion in 2020 to $120 billion last year, according to estimates, and is expected to grow at an annual rate of 26 percent.

Several BNPL startups are dominating the BNPL industry. Names like Afterpay and Klarna have attracted significant attention over the years due to their high valuations and growth.

Apple became the latest to dive into the BNPL space. The company is launching Apple Pay Later in September, integrating the services with its existing Apple Pay ecosystem. Unlike BNPL players, Apple said that it is going to do a 'soft' credit check of the consumer and a review of their transaction history with Apple.

“Whilst BNPL is primed for years of success, with new operators entering the field including PayPal, Amazon and Square, those in the sector must remain vigilant to the threat of fraud. As investment rises in BNPL, unfortunately so will the case of fraud. During this period of significant growth, there’s definitely an urgent need for regulation within the UK BNPL market,” said Jimmy Fong, the Chief Commercial Officer at SEON.

BNPL in the UK

Similar to most of the global markets, the demand for BNPL also exploded in the United Kingdom. A report by Barclays Bank and debt charity StepChange further revealed that 30 percent of Britons are now using BNPL services to purchase goods and services. Also, the average number of purchases funding BNPL doubled to 4.8 purchases since February with the average outstanding balance now around £254.

Another report by Finder.com reveals that the impact of Covid pushed the adaption of BNPL platforms. More than half of the UK's BNPL users started to use the services during the Covid-19 lockdown period. Also, this payment mode is more popular among the young generation as 54 percent of UK users are millennials.

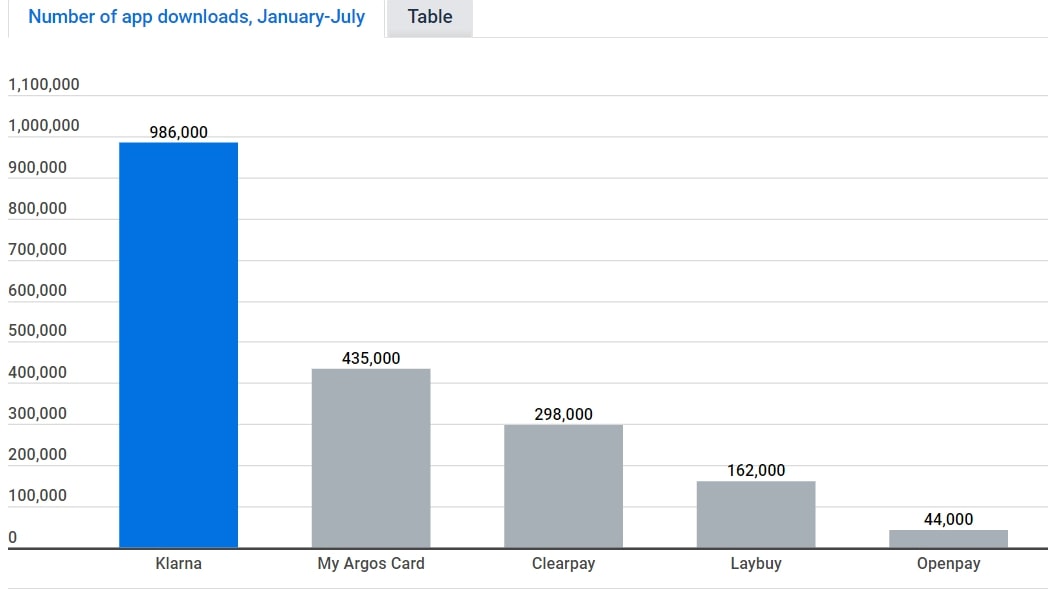

As for the platforms, Klarna dominates the UK markets with around 986,000 downloads of its app by the end of June 2020. The blooming future of such platforms is also clear as 8.6 million Brits plan to use BNPL services in the future and 9.5 million people said that they would avoid retail platforms not offering any BNPL options.

The Necessity of Regulations

Regulations for any emerging industry become necessary when it captures a significant market, and there are risks to the consumers. BNPL checks all of these criteria.

“With the increased expansion of BNPL-type experiences into more direct to consumer offerings (rather than facilitated through a merchant), we would expect to see their fraud teams tested in different ways,” said Naftali Harris, the Founder and CEO of SentiLink.

“There's a lot of nuance in the types of fraud a BNPL provider will see depending on their product strategy and merchant mix, and this type of nuance is something that is probably under-appreciated by those who have never worked in risk before. While there are multiple parties to a typical transaction, it is the BNPL companies that bear the risk of losses from defaults or fraudulent loans. If the loans are sold, some of that risk shifts to capital market providers. As such, both merchants and consumers need to be evaluated for risk.”

However, the impact of regulations on the BNPL industry remains to be seen as the UK and other regulators implement the laws. Though the regulations are not anticipated to be like the regular banking industry, they will still make a significant impact on the industry.

“It’s tough to say because we don’t know what the regulation will entail exactly. The worst-case scenario for the industry is if it ends up similar to the payday loan regulations, which would force the market to consolidate or go under. Best case, it eliminates consumer harming practices and makes way for frictionless BNPL being a part of our everyday online payment method options,” Fong said.

Is It Justified?

However, regulators should have enough consideration to justify the regulatory imposition. This should be even higher for a sector that is operating with an exemption.

Muinmos’ Kirketerp-Moller said: “As this sector relies, basically, on an exemption from regulation, I think the considerations should not be so substantial. If there is real potential for harm to the consumer (and it seems there is, even if we’re talking about relatively small sums); and a potential larger systematic harm (and here, it is the very fast growth of this sector which indicates there is); I think that’s enough to justify minimizing or withdrawing the exemption (and imposing regulatory requirements such as appropriateness checks, reporting duties in the favour of credit ratings, and better KYC processes).”

Now the wait is around the draft legislation of the UK government. It is to be seen if the lawmakers only impose basic checks or some stringent rules that bring harm to the industry.