One of the trusted providers of data and Analytics serving financial professionals including the Foreign Exchange industry, Bloomberg L.P and its subsidiaries, through its Indexes line of business, has unveiled a new product called the Bloomberg US Dollar Index, according to a recent corporate announcement.

The benchmark, under the bloomberg ticker symbol "BBDXY", provides investors a new way to assess, trade or invest in the value of the dollar against major global currencies as the growth in emerging market economies has brought new currencies to the forefront of FX market trading.

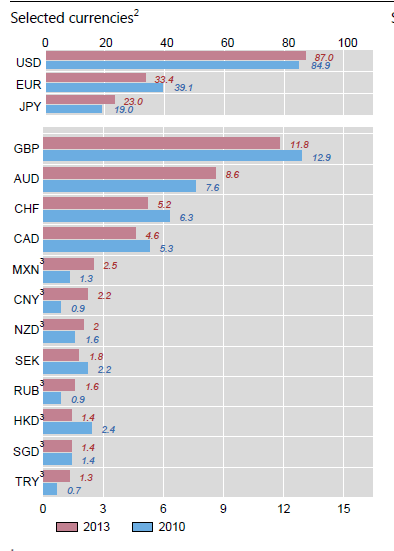

The U.S dollar continues to be the key currency against which other currencies are measured, and accounted for 87% of all currency pair transactions in April 2013 (on one side of the trade) according to recent BIS reports.

The value in creating an index, that can be used as a benchmark for tracking and investing purposes, becomes of great value as a means to reduce the complexity of tracking each currency independently and then against one another. The dominant and widely used Dollar Index (DXY) has little changed in 30 years, and thus may merit a new approach to index construction such as that unveiled by Bloomberg Indexes.

Percentage of April 2013 Turnover and April 2010 Turnover. Source: Bank for International Settlements - 2013 Triennial Survey

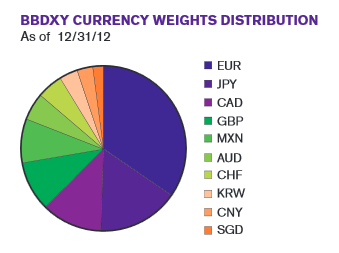

This need for an up-to-date index is more apparent relative to currencies that have recently increased their global market share of trading volumes, such as the Mexican peso, which recently came amongst the top ten in rank of global currency trading volumes, and thus overtaking the New Zealand dollar and Swedish krona. The Chinese currency, the renminbi also surged over the last few years becoming the ninth most traded pair (vs. the USD) in Apil 2013, as China moves towards a more free floating monetary policy. Also added is the Korean won and Singapore dollar (ranked 17th and 15th respectively according to BIS). A list of selected currencies and their percentage of trading volumes can be seen in the diagram on the left. The full list of currency symbols in the Bloomberg US Dollar Index can be seen below in the BBDXY pie chart.

The value of using an index as a benchmark for consolidating the pricing of a broader basket of underlying asset classes and instruments can be useful in many ways to investors, traders, money managers, banks and brokerage companies and in various applications. For example, these indexes can be used to create ETF products as well as CFD and OTC derivatives by brokerage providers who then offer the products as tradable instruments to clients.

Source: Bloomberg Indexes

The indexes can be used in constructing portfolios, determining asset allocation and measuring market sentiment as well as benchmarking investment strategies and trading systems, including calculating any subsequent tracking errors or information ratios for systems aiming to model the performance of the index. The first to license the Bloomberg Index is WisdomTree Investments, an exchange-traded fund (ETF) provider and asset manager that will use the products as a benchmark for ETFs.

A Need For Change

According to Forex Magnates' research, the unique aspects of the methodology behind the index construction put forth by Bloomberg is that every year when it re-balances, new currencies may be included as market conditions change, and thus serves as a framework for long-term use despite future shifts in market volumes.

More specifically, during the annual readjustment phase, the top 20 currencies in terms of trading activity versus the U.S. dollar, as defined by the Federal Reserve in its Broad Index of the Foreign Exchange Value of the Dollar and top 20 currencies from the Triennial Central Bank Survey of Foreign Exchange and Derivatives Market Activity (Table: Currency Distribution of Global Foreign Exchange Market Turnover), together form the union of sets of top 10 currencies of both lists.

The currencies pegged to the U.S. dollar are adjusted for various parameters and then the assigned weights are based on trading and Liquidity which are then added to the combined set thus arriving at a final index weight (after taking into account other related calculations as per the Index Membership and Weights for the BBDXY Methodology).

The final results ensure that from year-to-year, only currencies meeting the above criteria are included and thus reflective of the change in top tier rank of global currencies (with regards to their respective market share).

Dynamic versus Static Index Composition

This unique index construction may provide a clear way to stay up to speed on the top ten currencies as they change from year to year, by looking at the net-price derived from the underlying basket consisting from the BBDXY price at any given time.

In addition, there is also a total return index (BBDXT) that assumes investment of collateral returns in local markets using one month forward implied yields, and an inverse total return index (BBDXI) that tracks a short position in the U.S. dollar inclusive of funding costs. Although the price return index is generated in real-time under the ticker BBDXY, the total return index and the inverse index are generated once a day under the tickers BBDXT and BBDXI. These expand upon previously launched Indexes by Bloomberg, including the Bloomberg JP Morgan Asia Currency Index (ADXY) and the Bloomberg JP Morgan Latin American Currency Index (LACI).

According to the company's product description, unlike the traditional US Dollar Index (DXY), the BBDXY is not dominated by the euro, and also includes major emerging market currencies such as Korean won, Mexican peso and Chinese renminbi —all major trading partners of the U.S. with increasing liquidity. Moreover, its is positioned as more dynamic via the annual rebalancing process that captures the changing state of currency markets as opposed to a fixed index composition.

Recent and Legacy FX Indexes

Over the last 5 years, there have been a few initiatives to create indexes that reflect foreign exchange prices as the decentralized nature of the foreign exchange markets creates the pricing challenge with regards to standardizing fx rates. Some examples of such efforts include the The S&P Currency Arbitrage Index, which was designed to model a carry trade strategy and consisted of positions in the G10 currencies based on their relative interest rates versus the U.S.dollar, based on underlying currencies including the Australian dollar, British pound, Canadian dollar, Euro, Japanese yen, New Zealand dollar, Norwegian krone, Swedish krona and the Swiss franc (excluding the U.S. dollar).

The S&P Currency Arbitrage Index was different in the sense that its basket represented a long position in currencies that have a higher interest rate than the U.S. dollar and a short position in currencies that have a lower interest rate than the U.S. dollar, and each currency weighted proportionally to its interest rate spread and inversely proportional to its volatility, and thus increases weights of currencies with higher spreads and lower volatility. S&P literally has constructed thousands of indexes and the above is just one example.

More recently, The Dow Jones FXCM Indexes were launched, offered collaboratively by S&P Dow Jones Indices and FXCM, for the U.S. dollar and Japanese yen respectively. The Dow Jones FXCM US Dollar index was built by equal weighting the following currency pairs: EUR/USD, GBP/USD, USD/JPY and AUD/USD. The Dow Jones Yen Index, reflects changes in the value of the Japanese yen measured against a basket equal weighting four currency pairs including the :USD/JPY, EUR/JPY, AUD/JPY and NZD/JPY,as of the index inception date and at rebalancings. While these indexes both update every 15 seconds as calculated, rebalancing requires a 5 day notice period if certain thresholds are met.

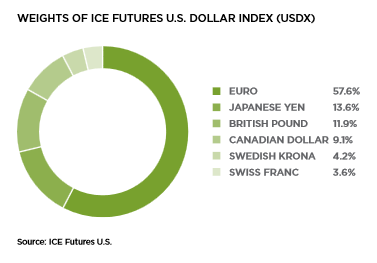

Source: ICE USDX

The oldest of the constructed indexes is the above mentioned US Dollar Index which is used by the Intercontinental Exchange (ICE) and tradable as a futures contract in the U.S. The ICE U.S. Dollar Index (USDX) futures contract is widely used as a benchmark for the international value of the US dollar against a basket of currencies. Despite its uniqueness, the USDX is fixed in composition since its 1973 introduction, and has since changed only once when the euro was launched in January 1999, replacing a number of European currencies. The net representation of the European legacy currencies in the USDX remained fixed at 57.6%, according to a report published by ICE.

The evolution of currency indexes could lead closer towards the centralization of foreign exchange markets altogether, as the need for greater transparency and pricing tends to be of increasing importance. When coupled with the efficiency of current FX Market dynamics and technology developments, this eventuality of a single market framework (centralized location/exchange) could become inevitable over the next ten or twenty years as foreign exchange regulations become more globalized and prices more standardized.