The past few weeks have been filled with ample speculation in relation to the effects of an impending referendum in Switzerland on whether or not the central bank should hold 20% of its reserves in physical gold and whether it should repatriate its existing reserves to home turf. With speculation rising in the run-up to the referendum, the market has priced in a NO vote.

With chances of a YES vote taking over being very slim, at least according to preliminary polls, the gold referendum is doomed according to the precious metals market. Just as was with the Scottish referendum, despite some polling hiccups, the noise accompanying the event is much bigger of an event than the vote itself.

This is not to say that the event should be ignored by the market - the public’s attitude towards the market is quite important in fact. While this gold referendum most likely won't be passed, the next one could - it will only take another global debt cycle to unfold. Before the global financial crisis, gold was trading at around $800 after an 8 year bull market.

The nail in the coffin of the referendum might have been another part of the question posed to the most direct democracy in the world - as part of the purchases, the Swiss National Bank (SNB) is not to sell its gold… period. Last year, the SNB registered a $10.4 billion loss, which forced it to cancel dividend Payments to the Swiss government for the first time in its history.

The fact remains, that the Swiss economy is not isolated in any way from the rest of the world and any hike in its gold holdings will inevitably translate into a much stronger currency in times of financial troubles - a dilemma which the central bank has been facing ever since the demise of Lehman Brothers and the Euro Zone earthquakes.

No matter how much gold bugs would like to see a YES vote, the Swiss economy is not likely to deviate from conventional thinking dominating today's economy, it would take a much harder financial system shock to put this question back on the agenda.

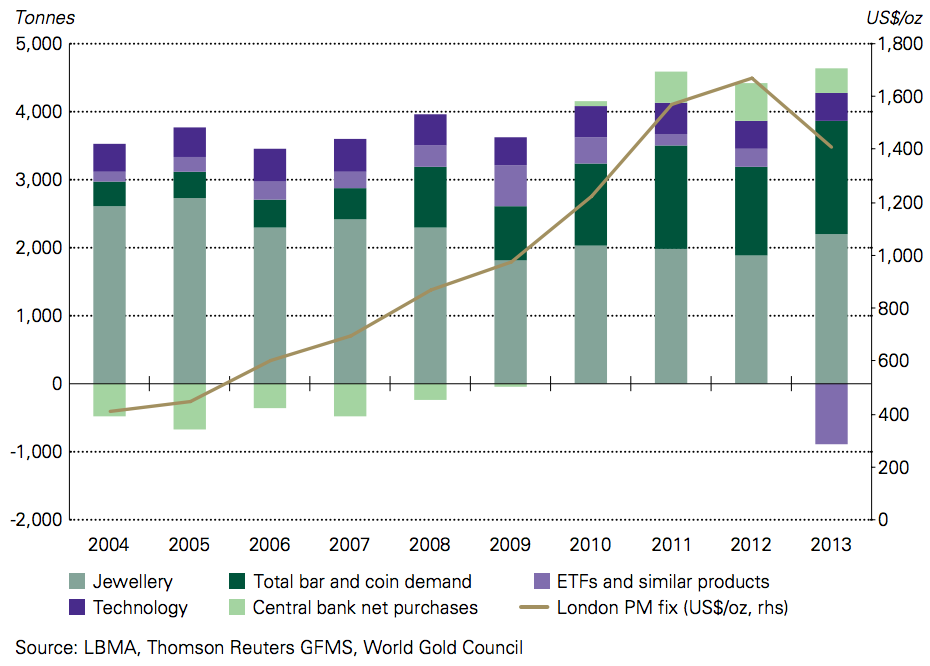

Finally, it's still worth mentioning that the 1,500 tonnes, which the SNB would have to purchase in case of a YES vote, for some reason has been dismissed by pundits as an insignificant amount. Global gold demand data for 2013 tends to contrast with these views.

Global Gold Demand by Category