This article was written by Ashley Aberneithy, CEO of Analytic AI.

It’s commonplace for risk managers to group their portfolio into risk books. The process of isolating risk within their portfolio involves risk managers creating distinct groups for different types of trader. The risk manager might place large size traders into one group, whereas high frequency traders may go into another group.

[gptAdvertisement]

The London Summit 2017 is coming, get involved!

The risk manager then hedges each group independently, i.e. the high frequency traders might be best served by an automated hedging process (STP) whereas certain traders might just be shut down or flagged as fraudulent. How accurately these groupings reflect the characteristics of the firm's portfolio directly impacts a firm's bottom line and financial institutions dedicate a large amount of time into analyzing traders and building these classification groupings.

Has a trader exhibited certain characteristics within their past trading behavior?

Many risk managers ask the question ‘has a trader exhibited certain characteristics within their past trading behavior that can be used to predict the best classification for them going forwards?’ but the main problem with this approach is that (a) the accuracy of this method is questionable (b) this analysis is very time consuming and (c) due to the large number of inputs the analysis highly subjective and prone to error.

In many cases risk managers might just not even have enough data about the trader to make these decisions.

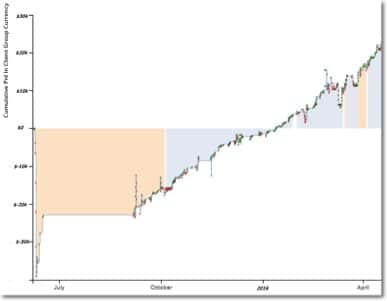

Figure 1 showing how machine learning algorithms can reclassify traders very quickly

Artificial intelligence solutions aim to ‘quantitatively assess’ common heuristics and behavioural traits which exist amongst financial market traders

Machine learning and AI based algorithms are more effective at modeling risk groupings compared with their human counterparts, however they are not a silver bullet; these algorithms are extremely complex to build and it’s common for them to work on historical data, but fail when faced with new data. Building these solutions also requires specialist skillsets in machine learning and quantitative Risk Management ; skills, which are in short supply and high, demand.

When I speak to firms it’s not uncommon for them to complain about spending months, even years, with varying degrees of success, researching these automated solutions for optimizing their risk groups. There is hope however! We are starting to see an emergence of cost effective artificial intelligence within the financial space and some specialist vendors providing both out-of-the-box solutions as well as more customized solutions to fit the needs of specific firms.

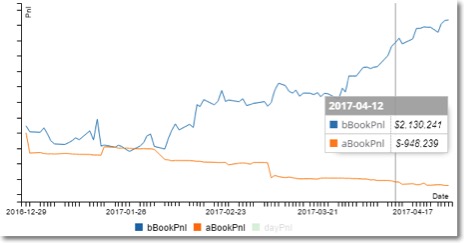

Figure 2 shows a screenshot of a machine learning algorithm that can optimising a firm's profit at a portfolio level.

How do you know using this type of automated solution is right for your firm? Many of these firms offer backtesting solutions which allow firms to forecast how these algorithms can perform on your data going forwards. The numbers provided might be enough for you decide to make the switch, or at least augment your existing classification process with an AI based solution.

The other main driver is Scalability , if you need a solution which can scale no matter the trade volumes, 24 hours a day, then moving to an algorithmic solution could be a good solution for your firm.