OPEC members may try to keep prices elevated over the coming weeks, but the talk of an output freeze is a mere distraction.

Bloomberg

This article was written by Idan Levitov, head analyst for anyoption.com.

Although jawboning from OPEC member states has been enough to squeeze market shorts and bring oil prices back above $40.00 per barrel over the last few weeks, these remarks remain a minor distraction in the bigger picture outlook for the energy complex. Ignoring the commentary and focusing on the fundamentals shows that inventories remain significantly elevated across the globe, with a new glut emerging in refined products as the impact of Chinese teapot refining exports are felt at ports around the world.

Now that inventories are back on the rise following traditional summer stockpile drawdowns, the threat of an output freeze has been enough to dissuade oil shorts at least temporarily. However, on a more medium-term basis, lack of cohesion amongst OPEC members combined with rising US production and the possibility of resurgent Nigerian output could derail recent price gains, forcing crude back to the downside.

Discord Remains in Abundance

Markets have been preparing for the possibility of another discussion of a production ceiling amongst OPEC and select non-OPEC members in an effort to put a floor in prices that have remained volatile over the last few months. Although rumors about production freezes neatly coincided with a steep drop off in crude oil prices, trying to find a consensus amongst OPEC members these days is nearly impossible.

Despite Saudi Arabia torpedoing the last output freeze talks Doha, it could very well be Iran that walks away from the table during the upcoming round of negotiations as the Islamic Republic works to restore production to pre-sanctions levels.

Meanwhile, Saudi Arabian output continues to climb after reaching a record of 10.67 million barrels per day (bpd) in production during July. Furthermore, they are expected to show further gains in August towards 10.90 million bpd, overtaking Russia’s 10.85 million bpd as the globe’s largest producer.

While part of this could be attributed to higher seasonal demand domestically, it could be intended as a move to maintain and grow market share during a time of extreme market turbulence. Nevertheless, bringing all the parties, both OPEC and non-OPEC to the table and enforcing an agreement remains a distant possibility.

Outside of OPEC is the resurgent American growth and rising global inventories. In the US, inventories rose by an astounding 2.501 million barrels last week after falling by a similar amount the prior week, marking the biggest stockpile build in 3 months. Rising inventories have also been accompanied by increased domestic production, which was rising at the fastest pace since May of 2015 until falling by 57,000 bpd last week to 8.548 million bpd. Additionally, a rising rig count could further complicate the outlook.

According to Baker Hughes data, from Friday August 19th, the oil drill rig count rose by 10 rigs, marking 8-straight weeks of increases, leading to higher production potential over coming weeks. Considering all these factors with the possibility of a revival of 700,000 bpd in output from Nigeria, the stage remains set for oversupply to persist for the second half of 2016.

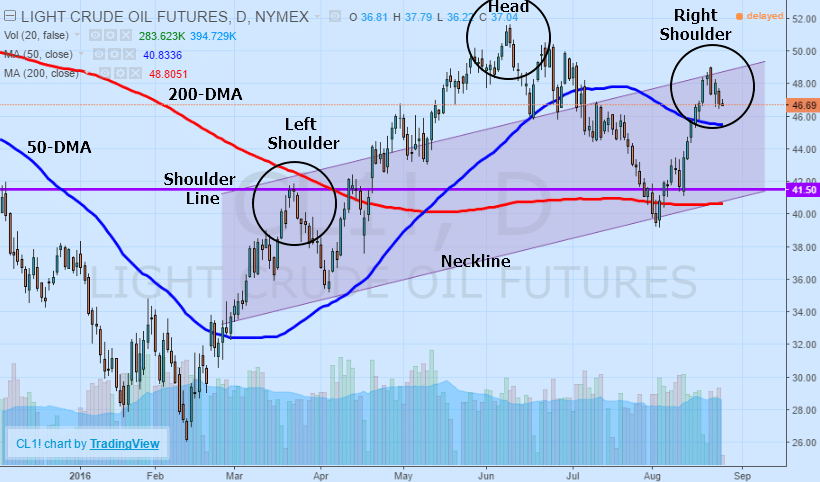

Technically Speaking

Looking at oil prices from a technical perspective, the bull market in prices remains intact, however, recent gains may be the product of a short squeeze and not necessarily fundamentals. With CFTC data showing net long positions rising last week, it may indicate significant short covering. Bearing in mind this factor, the current rally is only supported by few indicators, namely the moving averages which are trending below the price action.

Another downturn in prices might be slowed by support from both the 50 and 200-day moving averages. However, an emerging head and shoulders bearish pattern may add to any downside momentum. With the right shoulder of the pattern forming, the next major stop for price action may be $41.50 on the downside if the 50-day moving average, paving the way towards support at the 200-day moving average coinciding with the neck line of the head and shoulders pattern.

Looking Ahead

Although OPEC members may release more tape bombs over the coming weeks to keep prices elevated, the smokescreen that is output freeze jawboning should be appreciated for what it is, namely a distraction. With production levels rising globally and the possibility of rebounding Nigerian production in the fold, the major developments that could seriously derail recent gains in oil prices remains data related to output and stockpiling.

Should Nigeria manage to come to an agreement with the Niger Delta Avengers, it could see output revived, endangering any hope of a market equilibrium that keeps prices elevated. With very few upside catalysts and significant downside risks, the most recent rally in oil prices may be nothing more than a short squeeze as the speculators reload short positions at higher prices.

This article was written by Idan Levitov, head analyst for anyoption.com.

Although jawboning from OPEC member states has been enough to squeeze market shorts and bring oil prices back above $40.00 per barrel over the last few weeks, these remarks remain a minor distraction in the bigger picture outlook for the energy complex. Ignoring the commentary and focusing on the fundamentals shows that inventories remain significantly elevated across the globe, with a new glut emerging in refined products as the impact of Chinese teapot refining exports are felt at ports around the world.

Now that inventories are back on the rise following traditional summer stockpile drawdowns, the threat of an output freeze has been enough to dissuade oil shorts at least temporarily. However, on a more medium-term basis, lack of cohesion amongst OPEC members combined with rising US production and the possibility of resurgent Nigerian output could derail recent price gains, forcing crude back to the downside.

Discord Remains in Abundance

Markets have been preparing for the possibility of another discussion of a production ceiling amongst OPEC and select non-OPEC members in an effort to put a floor in prices that have remained volatile over the last few months. Although rumors about production freezes neatly coincided with a steep drop off in crude oil prices, trying to find a consensus amongst OPEC members these days is nearly impossible.

Despite Saudi Arabia torpedoing the last output freeze talks Doha, it could very well be Iran that walks away from the table during the upcoming round of negotiations as the Islamic Republic works to restore production to pre-sanctions levels.

Meanwhile, Saudi Arabian output continues to climb after reaching a record of 10.67 million barrels per day (bpd) in production during July. Furthermore, they are expected to show further gains in August towards 10.90 million bpd, overtaking Russia’s 10.85 million bpd as the globe’s largest producer.

While part of this could be attributed to higher seasonal demand domestically, it could be intended as a move to maintain and grow market share during a time of extreme market turbulence. Nevertheless, bringing all the parties, both OPEC and non-OPEC to the table and enforcing an agreement remains a distant possibility.

Outside of OPEC is the resurgent American growth and rising global inventories. In the US, inventories rose by an astounding 2.501 million barrels last week after falling by a similar amount the prior week, marking the biggest stockpile build in 3 months. Rising inventories have also been accompanied by increased domestic production, which was rising at the fastest pace since May of 2015 until falling by 57,000 bpd last week to 8.548 million bpd. Additionally, a rising rig count could further complicate the outlook.

According to Baker Hughes data, from Friday August 19th, the oil drill rig count rose by 10 rigs, marking 8-straight weeks of increases, leading to higher production potential over coming weeks. Considering all these factors with the possibility of a revival of 700,000 bpd in output from Nigeria, the stage remains set for oversupply to persist for the second half of 2016.

Technically Speaking

Looking at oil prices from a technical perspective, the bull market in prices remains intact, however, recent gains may be the product of a short squeeze and not necessarily fundamentals. With CFTC data showing net long positions rising last week, it may indicate significant short covering. Bearing in mind this factor, the current rally is only supported by few indicators, namely the moving averages which are trending below the price action.

Another downturn in prices might be slowed by support from both the 50 and 200-day moving averages. However, an emerging head and shoulders bearish pattern may add to any downside momentum. With the right shoulder of the pattern forming, the next major stop for price action may be $41.50 on the downside if the 50-day moving average, paving the way towards support at the 200-day moving average coinciding with the neck line of the head and shoulders pattern.

Looking Ahead

Although OPEC members may release more tape bombs over the coming weeks to keep prices elevated, the smokescreen that is output freeze jawboning should be appreciated for what it is, namely a distraction. With production levels rising globally and the possibility of rebounding Nigerian production in the fold, the major developments that could seriously derail recent gains in oil prices remains data related to output and stockpiling.

Should Nigeria manage to come to an agreement with the Niger Delta Avengers, it could see output revived, endangering any hope of a market equilibrium that keeps prices elevated. With very few upside catalysts and significant downside risks, the most recent rally in oil prices may be nothing more than a short squeeze as the speculators reload short positions at higher prices.

Idan is the VP trading for anyoption.com. He is a seasoned professional with years of experience trading and has a vast knowledge of the financial markets. An expert in the binary options hedging field - Idan provides insights, guidance and coordination in business planning, risk management and technology strategies. He holds a BA in Economics Management and is now busy finishing his MBA in Finance. Idan is the VP trading for anyoption.com. He is a seasoned professional with years of experience and a vast knowledge of the financial markets. An expert in the binary options hedging field - Idan provides insights, guidance and coordination in business planning, risk management and technology strategies. He holds a BA in Economics Management and is now busy finishing his MBA in Finance.

Capital Index UK Changes Name to Vantos Markets Following Tough Trading Year

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights