The company’s CEO Drew Niv highlighted in the conference call after the FXCM Inc earnings report yesterday that the firm intended to repay its loan to Leucadia National by the end of 2015 primary through assets sales.

After FXCM Inc (NYSE:FXCM) reported its earnings and trading volumes figures yesterday, the company’s CEO Drew Niv and CFO Robert Lande have taken to the earnings call. FXCM’s senior management revealed crucial details about the company's future plans after the dramatic events of the 15th of January.

The main takeaway from the earnings call is that as expected, there will be a major restructuring of FXCM Inc's (NYSE:FXCM) business in the coming months. The company’s CEO Drew Niv outlined that aside from selling its institutional businesses, which was already clearly communicated by the firm, it intends to part with its FXCM Japan and FXCM Hong Kong subsidiaries.

In the aftermath of the Swiss National Bank’s decision to scrap the floor under the EUR/CHF, FXCM Inc (NYSE:FXCM) was forced to shore up its balance sheet. The company was forced to recapitalize, signing a $300 million loan agreement with Leucadia National with a starting interest rate of 10%, growing by 1.5% each quarter.

Revision of Losses from January 15th and Sale of FXCM Japan and Hong Kong

Estimated losses from the Swiss National Bank's induced Volatility on the currency markets have increased to $276 million from the initially reported $225 million. This figure matches the net proceeds which FXCM Inc (NYSE:FXCM) got from the Leucadia National loan agreement.

The company’s CEO, Drew Niv, highlighted during the earnings call that the firm intends to make significant reductions in its obligations to Leucadia National through the sale of non-core assets. The main surprise from this statement is in the details, as the CEO of FXCM Inc (NYSE:FXCM) stated that the firm decided to exit its business in Japan and Hong Kong.

Speaking during the earnings call, Mr. Niv said, “We have decided to exit the Japanese and Hong Kong retail markets selling our locally regulated subsidiary in each country. The sales will not only generate meaningful proceeds, but will also liberate over $50 million of cash which currently resides in these two entities.”

“We have multiple bids for each subsidiary and are seeing significant competition for these properties. We are in active discussions to select the best bid and move towards closing in the near future,” he explained.

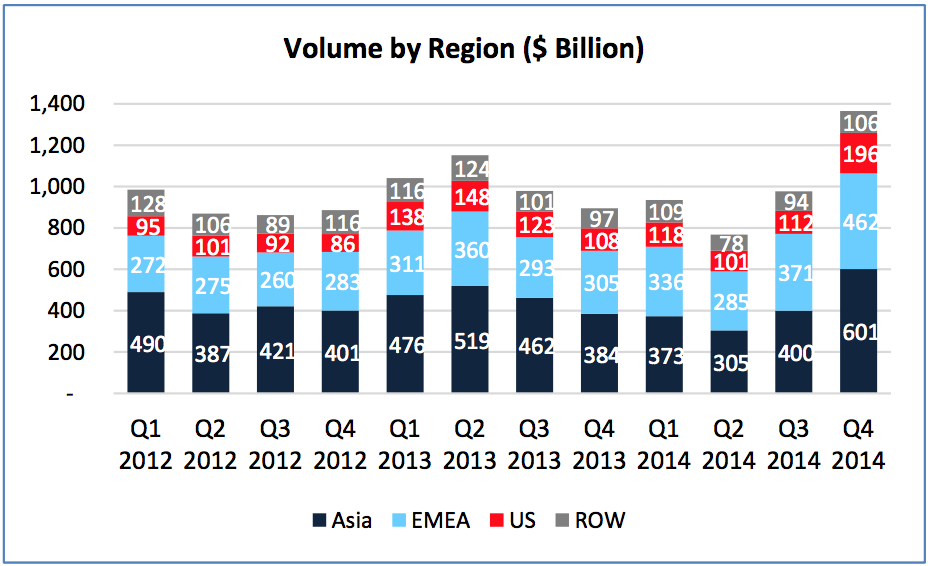

FXCM Trading Volume by Region, Source: FXCM

From the $50 million which Mr. Niv mentioned, $22 million in cash lie on the balance sheet of FXCM Japan, while the remaining $28 million are in the Hong Kong subsidiary of FXCM Inc.

The company's CEO Drew Niv stated, “We believe that the sale proceeds plus cash freed from the balance sheet of these entities could exceed $250 million, which would go a long way towards repaying if not fully repaying the Leucadia loan.”

Considering the lucrative Japanese market and the expansion appetite of many companies to acquire businesses in the region, the sale of this unit could net FXCM somewhere between $40 and $50 million.

The Hong Kong unit of the firm generated about $2.5 million in non-GAAP adjusted EBITDA in 2014. The jurisdiction and the lack of wide media coverage of the Swiss National Bank conundrum which FXCM faced, likely saved the value of the brand and clients continued to hold their accounts with the brokerage.

The main proceeds from potential sales will come from the non-core business of FXCM Inc (NYSE:FXCM). Back in 2012, FXCM acquired Lucid Markets for $176 million, with the estimated total costs of the investment totaling $192 million.

Considering the pressure under which FXCM is to sell its institutional business, and the outflow of institutional clients from FXCM, the company is not likely to recover its investment in this business.

The other big institutional business of FXCM, FastMatch, has experienced dwindling volumes in the aftermath of the Swiss National Bank debacle leading to decreased volumes.

FXCM owns 35% of FastMatch and the stake is on the sale list of the company alongside its high-frequency trading investment in V3. The company paid around $16 million for a 50.1 percent stake in V3, with the rest of the unit owned by Lucid Markets.

Retail Revenue per Million Drops to $69, Clients to Choose Dealing Desk or Not

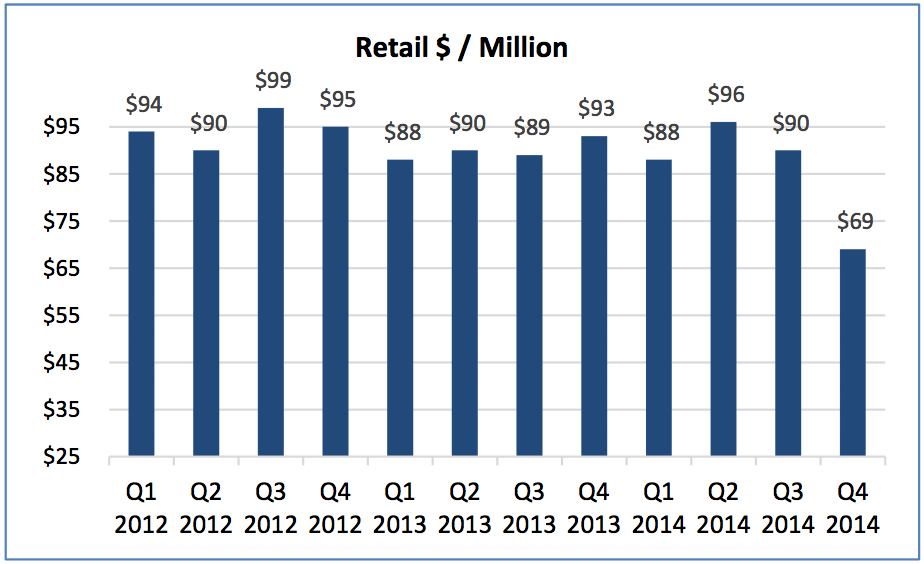

FXCM Retail Revenue per Million, Source: FXCM

The retail revenues per million (RPM) which FXCM reported for the fourth quarter of 2014 totaled $69. This is $1 below the estimate which the company made in its previous earnings report.

In order to optimize its RPM, FXCM Inc (NYSE:FXCM) has announced that it will be returning the dealing desk model for clients with equity below $20,000.

The company’s CEO Drew Niv said during the earnings call, “To accelerate growth in our core business we will launch a hybrid desk model for small retail FX accounts. These are accounts with less than $20,000 of deposits. While these accounts maybe large in number, they still represent much less than half of our trading volume.”

FXCM Inc aims to balance between dealing desk and agency model execution in order to maximize its RPM. The brokerage will present a choice for clients between higher Leverage options with dealing desk execution and agency execution with lower leverage.

Following the announcement, shares of FXCM Inc (NYSE:FXCM) traded up 15% in pre-market trading on the New York Stock Exchange at $2.48.

After FXCM Inc (NYSE:FXCM) reported its earnings and trading volumes figures yesterday, the company’s CEO Drew Niv and CFO Robert Lande have taken to the earnings call. FXCM’s senior management revealed crucial details about the company's future plans after the dramatic events of the 15th of January.

The main takeaway from the earnings call is that as expected, there will be a major restructuring of FXCM Inc's (NYSE:FXCM) business in the coming months. The company’s CEO Drew Niv outlined that aside from selling its institutional businesses, which was already clearly communicated by the firm, it intends to part with its FXCM Japan and FXCM Hong Kong subsidiaries.

In the aftermath of the Swiss National Bank’s decision to scrap the floor under the EUR/CHF, FXCM Inc (NYSE:FXCM) was forced to shore up its balance sheet. The company was forced to recapitalize, signing a $300 million loan agreement with Leucadia National with a starting interest rate of 10%, growing by 1.5% each quarter.

Revision of Losses from January 15th and Sale of FXCM Japan and Hong Kong

Estimated losses from the Swiss National Bank's induced Volatility on the currency markets have increased to $276 million from the initially reported $225 million. This figure matches the net proceeds which FXCM Inc (NYSE:FXCM) got from the Leucadia National loan agreement.

The company’s CEO, Drew Niv, highlighted during the earnings call that the firm intends to make significant reductions in its obligations to Leucadia National through the sale of non-core assets. The main surprise from this statement is in the details, as the CEO of FXCM Inc (NYSE:FXCM) stated that the firm decided to exit its business in Japan and Hong Kong.

Speaking during the earnings call, Mr. Niv said, “We have decided to exit the Japanese and Hong Kong retail markets selling our locally regulated subsidiary in each country. The sales will not only generate meaningful proceeds, but will also liberate over $50 million of cash which currently resides in these two entities.”

“We have multiple bids for each subsidiary and are seeing significant competition for these properties. We are in active discussions to select the best bid and move towards closing in the near future,” he explained.

FXCM Trading Volume by Region, Source: FXCM

From the $50 million which Mr. Niv mentioned, $22 million in cash lie on the balance sheet of FXCM Japan, while the remaining $28 million are in the Hong Kong subsidiary of FXCM Inc.

The company's CEO Drew Niv stated, “We believe that the sale proceeds plus cash freed from the balance sheet of these entities could exceed $250 million, which would go a long way towards repaying if not fully repaying the Leucadia loan.”

Considering the lucrative Japanese market and the expansion appetite of many companies to acquire businesses in the region, the sale of this unit could net FXCM somewhere between $40 and $50 million.

The Hong Kong unit of the firm generated about $2.5 million in non-GAAP adjusted EBITDA in 2014. The jurisdiction and the lack of wide media coverage of the Swiss National Bank conundrum which FXCM faced, likely saved the value of the brand and clients continued to hold their accounts with the brokerage.

The main proceeds from potential sales will come from the non-core business of FXCM Inc (NYSE:FXCM). Back in 2012, FXCM acquired Lucid Markets for $176 million, with the estimated total costs of the investment totaling $192 million.

Considering the pressure under which FXCM is to sell its institutional business, and the outflow of institutional clients from FXCM, the company is not likely to recover its investment in this business.

The other big institutional business of FXCM, FastMatch, has experienced dwindling volumes in the aftermath of the Swiss National Bank debacle leading to decreased volumes.

FXCM owns 35% of FastMatch and the stake is on the sale list of the company alongside its high-frequency trading investment in V3. The company paid around $16 million for a 50.1 percent stake in V3, with the rest of the unit owned by Lucid Markets.

Retail Revenue per Million Drops to $69, Clients to Choose Dealing Desk or Not

FXCM Retail Revenue per Million, Source: FXCM

The retail revenues per million (RPM) which FXCM reported for the fourth quarter of 2014 totaled $69. This is $1 below the estimate which the company made in its previous earnings report.

In order to optimize its RPM, FXCM Inc (NYSE:FXCM) has announced that it will be returning the dealing desk model for clients with equity below $20,000.

The company’s CEO Drew Niv said during the earnings call, “To accelerate growth in our core business we will launch a hybrid desk model for small retail FX accounts. These are accounts with less than $20,000 of deposits. While these accounts maybe large in number, they still represent much less than half of our trading volume.”

FXCM Inc aims to balance between dealing desk and agency model execution in order to maximize its RPM. The brokerage will present a choice for clients between higher Leverage options with dealing desk execution and agency execution with lower leverage.

Following the announcement, shares of FXCM Inc (NYSE:FXCM) traded up 15% in pre-market trading on the New York Stock Exchange at $2.48.

Financial Commission Approves Monstrade Giving Clients Mediation and €20K Coverage

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights