IG Group, one of world's largest Forex and CFD brokers, published its results today and unsurprisingly all the numbers show decrease in activity. A few days ago its UK competitor London Capital Group published similarly depressing results as well.

IG Group Holdings plc (“IG” or “the Group”) today announces interim results for the six month period ended 30 November 2012.

Operating Summary

- Satisfactory results against an extremely strong prior year comparator

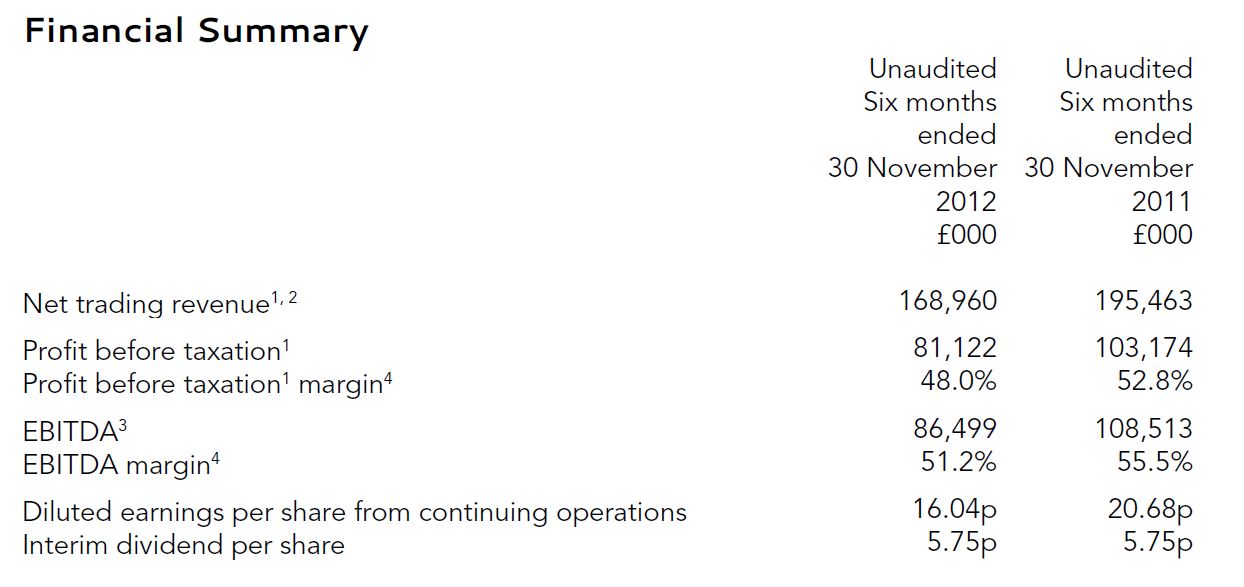

- Net trading revenue1 down 14% at £169.0 million

- Profit before tax1,3 down 21% to £81.1 million

- Diluted EPS1,3 down 22% at 16.04p

- £59.3 million of own funds generated from operations

- Interim dividend of 5.75p per share, flat on prior year

- Continued market share growth in three biggest markets

Tim Howkins, CEO IG Grouup (right)

Tim Howkins, Chief Executive, commented:

“Market conditions so far this year have been challenging for the industry. Against the backdrop of low market volatility and fragile consumer sentiment we have delivered a satisfactory set of results. We continue to maintain an appropriate level of investment in IT and marketing, mindful of the need to balance short term profitability against investment for the long term. This, along with our strong financial position, supports the increasing market lead we have in a number of the countries in which we operate and we believe will help deliver industry-leading growth rates over the longer term.”

Chief Executive’s statement, For the six months ended 30 November 2012

Our net trading revenue for the six months to 30 November 2012 was £169.0m, a decrease of 14% on the same period in the prior year. With operating costs flat year-on-year, profit before tax was down by 21% at £81.1m. The prior year was marked by extreme volatility in global financial markets, producing particularly strong comparators, which was in stark contrast to the very subdued markets throughout the current period.

Market conditions so far this year have been challenging for the industry. Although markets rose in 2012, with the FTSE100 up 10% in the six months to the end of November, this was against a backdrop of the longest sustained period of low volatility for over five years and trading volumes in underlying markets at multi-year lows. There is also continuing global economic uncertainty, fragile consumer sentiment and the ongoing market intervention by the Bank of England, the Federal Reserve and the European Central Bank which is dampening market reaction to newsflow. All of these factors impact on the behaviour of our existing and potential clients and in the period we saw reductions in the overall number of clients actively trading, the revenue we generated per client and the number of new clients signing up. However, there is nothing to suggest that the weakness in the first half is structural. On the few days in the period when we saw larger market movements our clients responded accordingly and our revenue on those days was, as would be expected, much higher. Further, we continued to gain market share in some of our key markets.

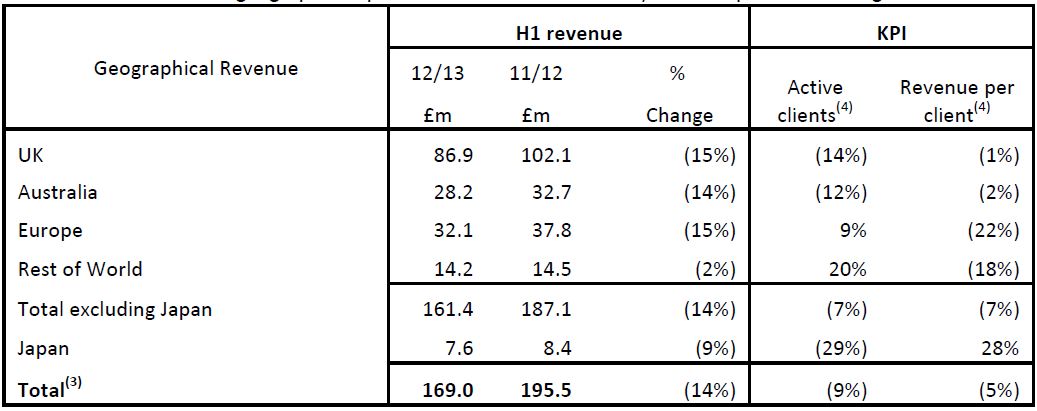

Geographic results

The table below shows a geographical split of the revenue achieved by the Group and the changes in active clients and revenue per client.

Our longer established UK and Australian businesses both performed similarly with the number of active clients falling by 14% and 12% respectively - reflecting the fact that within these large client bases fewer clients found markets sufficiently interesting to trade than was the case a year ago. However, in both businesses we saw only a very slight decline in revenue per client as the core of more experienced traders found opportunities even in the quiet markets.

Our European businesses delivered varying levels of client growth. The strongest growth came from our newest offices in Sweden and the Netherlands, albeit off low bases. Of the longer established offices Spain and Germany both delivered good growth in active client numbers while Italy and France were weaker. All of these businesses saw sharp falls in revenue per client. This reflects primarily the different mix of assets traded to that in the UK and Australia, with client activity on equity indices being most impacted by the decline in market volatility.

Within Rest of World we saw the strongest growth in client numbers from our US and South African businesses, while Singapore delivered active client growth of 6%. In line with the other less mature markets, all three businesses experienced a fall in revenue per client.

There have been a number of developments affecting our US business, Nadex. In July, PFG Best, the only broker connected to Nadex, went into bankruptcy. Although PFG Best was not a significant contributor to Nadex’s revenue this was a disappointing set-back. However, our other route to market, direct to retail, has made good progress and over the last nine months the number of members trading on the exchange has grown from around 600 to over 1,000 per month, though revenue per customer has fallen. Encouragingly, in early December the CFTC took enforcement action against two unregulated providers offering over the counter binary options illegally in the US from offshore; we hope they will extend this action against other illegal operators. Although Nadex remains a long term project, given the encouraging growth in active members trading on the exchange I am increasingly confident that we can take this business to profitability within a reasonable timeframe. It remains to be seen what the scale of opportunity will prove to be for this business over the longer term.

As previously reported, our Japanese business was impacted by the reductions in leverage limits, the last of which was introduced by the regulator in August 2011. Although the regulatory situation here remains challenging, we continue to concentrate our efforts on recruiting higher value clients which helps explain the strong increase in revenue per client and fall in active client numbers during the period.

Competitive positioning

These quiet market conditions demonstrate the benefits of IG’s scale and market leadership. Recent market research shows us gaining market share in the UK, Australia and Singapore. In both the UK and Australia we further extended our market leadership and in Singapore we became joint market leader in the forex market for the first time. We now have a 44% share of the UK spread betting market and a 37% market share of the Australian CFD market(2). Although this simple measure of customer accounts is useful, our strategy remains to target higher value active and professional traders, whereas some of our competitors target lower value clients. We are therefore less focused on driving up our overall market share and more focused on driving up our share of the most active traders and therefore our share of the total available revenue.

There are some signs that competition on price in our main markets is becoming less intense. One of our larger global competitors had competed aggressively on price for a year or so, but has recently reverted to pricing levels similar to ours. Their failure to gain market share with this pricing strategy supports our belief that clients are generally more focused on quality of execution, service and technology than on price alone.

A number of our competitors have been either loss making or only marginally profitable for several years. In these subdued markets there is evidence that they are finding conditions increasingly difficult, with announcements of large-scale redundancies and withdrawals from entire markets and we are also witnessing them cutting back heavily on their marketing expenditure.

Managing our costs

Against this industry backdrop we have taken what we believe to be a cautious and measured approach to managing our cost base. We currently anticipate that our operating costs this year will slightly below last year. Some costs, most obviously bonuses, have flexed with financial performance. We have trimmed our planned marketing spend, but given the reductions in marketing by our competitors we have not harmed our share of voice. We have also made some reductions to our headcount, as part of a process to ensure that each team within the business is right-sized for current levels of client activity. In IT development given the level of turmoil at some of our competitors we believe we can afford to proceed at a slightly slower pace than originally planned.

The steps we have so far taken on costs are sufficient to ensure that on our prudent view of full year revenue we are able to maintain a strong profit margin, although slightly below recent levels. I believe we can achieve this without putting our longer term growth at risk, particularly when the challenges faced by others in the industry are taken into account.

Growing our revenue

There is a risk that the current market and economic conditions last for some time. If these conditions do persist then we might reasonably expect low levels of revenue growth from our more established businesses in the UK and Australia, but higher levels of growth from our newer businesses in Europe, South Africa, Singapore and the US. These higher growth markets currently comprise a little over a quarter of total revenue.

We are pursuing a number of initiatives designed to drive near-term incremental revenue growth, which are not dependent on a return to a better external environment. These initiatives include some upgrades to our product offering, enhancements to our client recruitment, retention and reactivation procedures and on-going improvements to the dealing platforms and other tools which we offer our clients.

International expansion

Along with the enhancements to our offering in our more mature countries, the development of our less mature markets and expansion into further new markets remain key drivers of our longer-term growth.

Subsequent to the period end we have opened a small representative office in Dublin, Ireland. This is the only market outside the UK where spread betting is offered. Following a number of changes in the competitive landscape in Ireland we believe that the market is currently poorly served and that there are opportunities to gain market share in the near term.

We expect to open an office in Norway during the second half. Again this is a market where we believe competitive changes mean that there are near-term opportunities.

Neither of these countries represent large opportunities, but they are low cost, low risk and represent little incremental load on the infrastructure of the business.

We continue to evaluate other markets and expect to open at least one further office during our next financial year.

Investment in Technology

Our continued investment in our technology offering has been central to our market leadership in the industry. During the period we completed the initial roll-out of our mobile applications in all the countries in which we operate and across all of the main mobile operating systems. We now have the broadest suite of mobile applications in the industry and we believe that our decision to develop these as native applications, allowing clients to use the full functionality of their device, will provide the most rewarding user experience. The business continues to see an increase in the proportion of both client trades and account openings coming through mobile.

We continue to develop our Insight research tool, which we first launched nearly a year ago. This platform is now available to almost all our clients worldwide and we have recently released versions across a number of our mobile apps. Client feedback has been extremely positive and we will continue to further enhance Insight in response to client demand.

Online marketing now accounts for around a third of our total advertising expenditure and we believe provides an extremely efficient route to deliver highly targeted messages to an increasingly technologically astute audience. As well as additional skilled employees we are investing in technology which helps us track and improve the efficiency of our spend here.

Developing our brand

During the period we re-launched our IG brand in all the countries in which we operate other than Japan, where we will re-launch the brand in the second half and the US, where we operate under the Nadex brand.

The re-launch ensures that we provide a consistent look and experience across all of our clients’ interactions with us, including web sites, dealing platforms and advertising. This look and experience brings the external face of IG into line with the service and delivery excellence that we have built through our investment in technology and reflects our market position as a leading provider of online trading.

Initial reaction to the brand re-launch has been very favourable and the feedback has been positive in market research amongst our clients, our competitors’ clients and those who are considering online trading. I believe this investment has been an important step in positioning us for further growth.

Regulation and taxation

The regulation and taxation of the financial services industry continues to evolve and we are devoting an increasing amount of senior management time to monitoring developments and interacting with regulators, law makers and others. While there are currently a number of developments which we are monitoring closely I do not currently anticipate that any of these will have a material impact on the group. I have summarised the main areas that we are monitoring below.

There are two separate processes going on with regard to a Financial Transaction Tax (FTT) in certain European countries. A number of countries are at differing stages of introducing unilateral FTTs for their own purposes. France has already introduced a tax which applies only to cash equities and does not currently apply to either our client transactions or our hedge transactions. Italy has just announced quite a complex FTT, the precise meaning and implications of which we are still analysing, but it would appear to give us a competitive advantage for CFDs on Italian equities while potentially increasing the cost to our clients of trading the Italian index, but not by an unmanageable amount. Crucially it has no impact on forex, non-Italian equities and equity indices or commodities. Eleven EU member states are currently at an early stage in an “enhanced cooperation” process to introduce a harmonised FTT across those countries. Our discussions with senior EU representatives of a number of those countries suggest that reaching agreement on anything other than a very narrow scope FTT is likely to be difficult and that even that level of agreement may take considerable time. Overall, therefore, while we continue to closely monitor FTT developments at both a country and EU level we view this subject as unlikely to have significant adverse impact on the group.

Following a consultation paper in May 2012 the Monetary Authority of Singapore (MAS) has not yet published final rules nor indicated a possible start date, for reductions in leverage limits on forex. These rules are not expected to apply to high net worth individuals (accredited investors) and are expected to take account of a client’s ability to reduce their risk using stops. Both these factors would significantly mitigate any adverse impact that these rules, if and when eventually introduced, might otherwise have had. We are cooperating with a number of other CFD providers in Singapore and are together in discussions with MAS, seeking their approval of a client education module as part of the client knowledge assessment regime. If approved, we would expect this to improve our ability to open accounts in Singapore.

Regulators in Japan are reviewing the regulation of financial binary options. During the first half these accounted for approximately a third of our Japanese revenue. Though we continue to monitor the situation carefully, at this stage it appears unlikely this will have a significant adverse impact on this business.

The Australian regulator continues to scrutinise the treatment of client money. IG has always adopted a higher level of client money protection than required by Australian law and continues to lobby for a strengthening of the client money rules. We are a founding member of ‘The CFD Forum’, an industry body which sets out standards of conduct for its members on a number of matters, including treatment of client money.

Litigation

As previously disclosed, in 2010 the Group received a claim in relation to the insolvency of Echelon Wealth Management Limited (Echelon), a former client of the Group. The claimants (three former clients of Echelon) allege that IG is liable for the losses they suffered from the insolvency of Echelon. The claimants allege their losses amount to €100 million, comprising €12 million actual losses plus, in two of their cases, subsequent loss of profits of approximately €90 million, based on an alleged rate of return of 146% per annum since the collapse of Echelon. The claim went to trial at the end of 2012. It is expected that judgement will be handed down during the first half of 2013. The Group has always viewed the claim as speculative and has not made provision in respect of the claim. This view did not change during the course of the trial.

Cashflow and Liquidity

The Group continues to be highly cash generative and produced £59.3 million of own funds from operations during the period, after taxes of £29.6 million. There was a £32.2 million decrease in own funds after capital expenditure and the payment of the final dividend and working capital movements that relate to the prior financial year.

At the end of the period we had £380.0 million of cash resources, including £266.3 million of cash at brokers. The cash is placed at brokers to support our hedging activities and to facilitate near-term movements in the collateral requirements. This was up by £58.3 million from the prior year end, reflecting shifts in client positions. In addition we retain undrawn bank credit facilities of £180.0 million.

We perform regular stress testing of our liquidity needs in various scenarios and regulators are looking increasingly closely at liquidity arrangements. We believe that our current level of liquidity is adequate but not excessive.

Dividend

The Board has declared an interim dividend of 5.75p, amounting to £20.9 million which will be paid at the end of February. This is unchanged on last year. This reflects the Board’s confidence in IG’s continuing ability to generate strong cashflow.

Current trading and outlook

The period since the year end, aside from the Christmas and New Year holiday, has seen similar market conditions and levels of activity to those experienced during the first half. As we reported in December, if these activity levels persist revenue for the second half of the year is likely to be in line with the first half.

We continue to maintain an appropriate level of investment in IT and marketing, mindful of the need to balance short term profitability against investment for the long term. This investment and our strong financial position support the increasing market lead we have in a number of the countries in which we operate and we believe will help deliver industry-leading growth rates over the longer term.

Despite the current quiet market conditions and fragile economic outlook, I remain confident in our long term growth prospects.

Tim Howkins Chief Executive Officer 15 January 2013