BIS concerned about implications for price discovery.

But, market unconvinced transparency has been compromised.

Op-ed

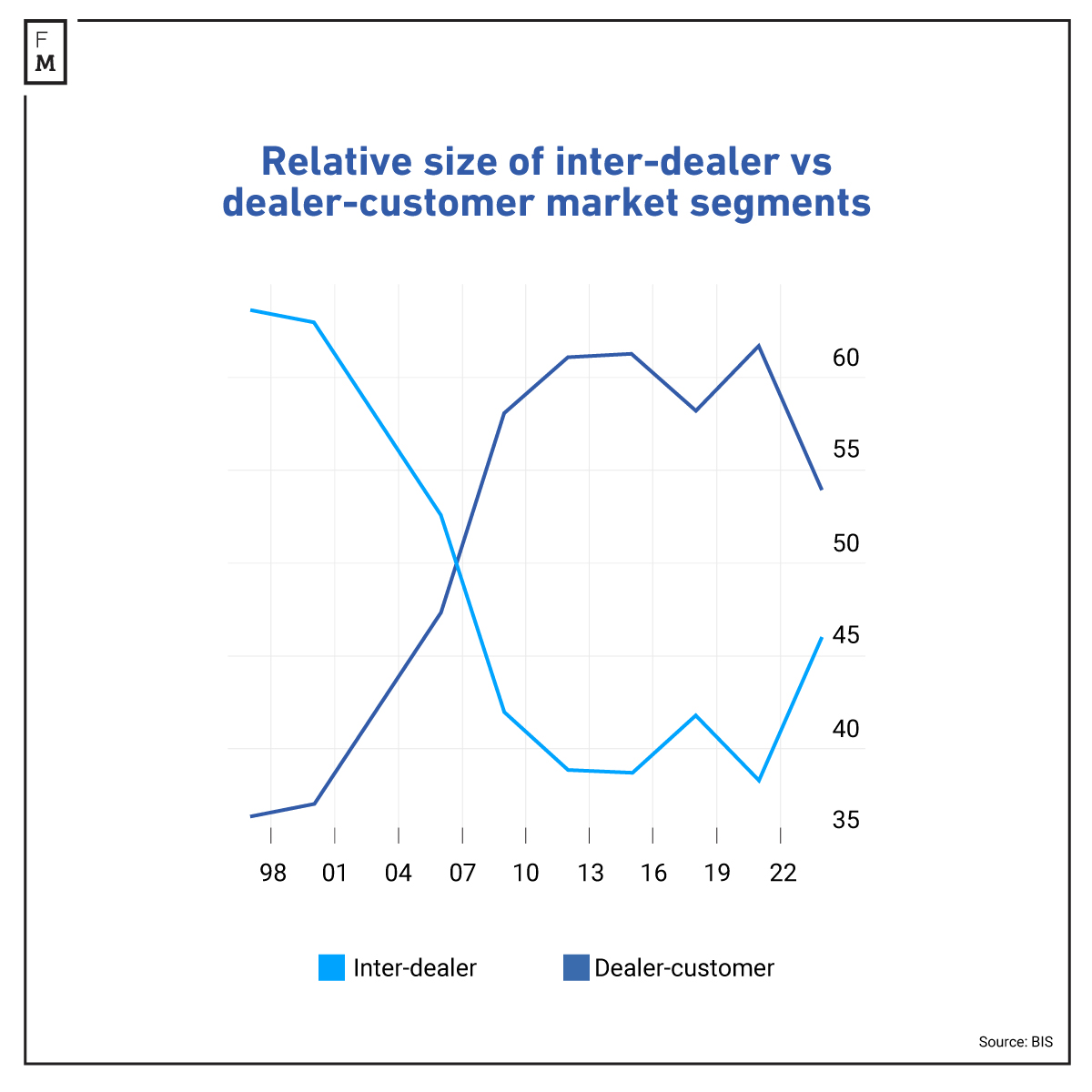

Increased inter-dealer trading is one of the least surprising consequences of the return of volatility to the FX market after a lengthy period of stability as dealers looking to reduce risk.

The most recent BIS triennial central bank survey found that inter-dealer trading had grown significantly between April 2019 and April 2022 to account for more than 45% of all FX trading volumes, reversing a period of decline that began in the mid-2000s. More than half of all swap trading was done between dealers.

The share of FX trading using various bilateral methods, where information about the trade remains private, also increased. As a result, in the inter-dealer market, trading volumes executed via electronic brokers (where trade attributes such as prices can be seen by all participants) continued to decline.

Geoff Kot, Global Head, Financial Markets Electronic Trading & Platforms, Standard Chartered

According to Vlad Sushko, a senior economist at the BIS, this implies a decrease in the transparency of the FX market. While accepting that this trend has so far not hampered market functioning, he says it could harm price discovery for the market as a whole.

Maxime Mordelet, an Institutional Digital Asset & E-forex Liquidity Manager at Swissquote agrees, observing that lower trading volumes on public venues reduces the amount of information available for market participants.

“In my opinion, the shift towards bilateral forms of trading has negative implications for price discovery since it reduces the source of information being available in primary and secondary sources of liquidity on which smaller banks or non-banks rely on to construct their own mid-price,” Mordelet stated.

However, Geoff Kot, the Global Head of Financial Markets Electronic Trading & Platforms at Standard Chartered reckons technology has mitigated many of the potential downsides of increased inter-dealer trading and greater fragmentation of FX market structure.

“There are now many technology solutions to aggregate pricing and deploy more sophisticated algorithmic execution strategies to optimise execution across various dimensions including price, speed and market impact,” Kot mentioned.

Where previously these technologies would have been bespoke implementations by the most sophisticated market participants, they are now cheaper and easier to access for a broader range of participants.

“At the same time the growth and availability of independent execution analytics services and mandatory transaction reporting for certain trade types means the information available to customers to make informed decisions regarding FX service provision is greater than ever,” added Kot.

Unlike many other asset classes, FX has never had a central exchange that represents a true picture of the market, so the idea of reducing transparency is relative.

Inter-dealer trading and the lack of a central price discovery mechanism for FX can make it more difficult for market participants to get a clear picture of the supply and demand dynamics and this can limit their ability to determine fair value.

However, it is important to note that inter-dealer trading also provides significant benefits, such as increasing liquidity and offering more efficient price discovery.

That is the view of Gerald Melia, the Head of Sales at StoneX Pro, who believes that the impact of inter-dealer trading on transparency may vary depending on the specific market and measures that are in place to promote transparency.

“For example, we have seen an increase in the popularity and demand for listed FX futures,” Melia pointed out. “FX Futures add more transparency so this indicates that this is what the market wants. We feel that the FX market operates optimally when OTC and listed FX futures co-habit in the same market.”

Melia is unconcerned about the potential impact of the shift towards bilateral forms of trading on price discovery, observing that professional FX clients are highly informed and that many have a background in treasury and finance.

“Additionally, markets have become less opaque with the availability of market data and industry benchmarks,” he says. “In saying that, we recommend that FX participants access and utilise consultants with FX, finance and capital market experience and leverage their experience and knowledge to maximise the benefits of new technology and trading venues.”

Sushko attributes the decline in dealer trading with customers to the risk-off environment. Mordelet agrees that this is a significant factor, although he also refers to a decrease in risk appetite from larger banks and more interest in reducing risk, either across internal desks or externally through interest-based quoting.

The BIS survey attributes some of the decline in dealer-customer trading to the contraction in international investment likely, resulting in a reduction in gross external portfolio positions. It further noted the decline in the market share of principal trading firms, which may be a function of these firms migrating to other asset classes with greater opportunities.

“However, it is also likely that the improvement of technology amongst dealers has also contributed to the decline in principal trading firms’ market share,” said Kot. “Pricing and execution algorithms have become more sophisticated, and the depth and persistence of liquidity from dealers is more highly valued during volatile market conditions.”

Most current forecasts for the economy and markets are negative or, at best, uncertain, and this drives investors from risk-on assets such as stocks, junk bonds and emerging market currencies to safer assets like government bonds, gold and developed country currencies.

“This can have a short term volume-increasing effect as investments move to safe haven assets, usually denominated in more stable currencies,” stated Melia. “Once this cycle of migration of capital has been completed, FX volumes naturally decrease.”

But, he acknowledged that this is not the full story since risk-off usually refers to the narrow spectrum of investments and risk management and ignores corporate investment. As the economic outlook worsens and uncertainty prevails, companies pull back on ordering raw materials and investments in projects to increase their international market share.

“This, in turn, can lead to changes in FX trading/hedging strategies as companies adjust their positions based on their outlook for different currencies and the perceived level of risk in those markets,” concluded Melia.

Increased inter-dealer trading is one of the least surprising consequences of the return of volatility to the FX market after a lengthy period of stability as dealers looking to reduce risk.

The most recent BIS triennial central bank survey found that inter-dealer trading had grown significantly between April 2019 and April 2022 to account for more than 45% of all FX trading volumes, reversing a period of decline that began in the mid-2000s. More than half of all swap trading was done between dealers.

The share of FX trading using various bilateral methods, where information about the trade remains private, also increased. As a result, in the inter-dealer market, trading volumes executed via electronic brokers (where trade attributes such as prices can be seen by all participants) continued to decline.

Geoff Kot, Global Head, Financial Markets Electronic Trading & Platforms, Standard Chartered

According to Vlad Sushko, a senior economist at the BIS, this implies a decrease in the transparency of the FX market. While accepting that this trend has so far not hampered market functioning, he says it could harm price discovery for the market as a whole.

Maxime Mordelet, an Institutional Digital Asset & E-forex Liquidity Manager at Swissquote agrees, observing that lower trading volumes on public venues reduces the amount of information available for market participants.

“In my opinion, the shift towards bilateral forms of trading has negative implications for price discovery since it reduces the source of information being available in primary and secondary sources of liquidity on which smaller banks or non-banks rely on to construct their own mid-price,” Mordelet stated.

However, Geoff Kot, the Global Head of Financial Markets Electronic Trading & Platforms at Standard Chartered reckons technology has mitigated many of the potential downsides of increased inter-dealer trading and greater fragmentation of FX market structure.

“There are now many technology solutions to aggregate pricing and deploy more sophisticated algorithmic execution strategies to optimise execution across various dimensions including price, speed and market impact,” Kot mentioned.

Where previously these technologies would have been bespoke implementations by the most sophisticated market participants, they are now cheaper and easier to access for a broader range of participants.

“At the same time the growth and availability of independent execution analytics services and mandatory transaction reporting for certain trade types means the information available to customers to make informed decisions regarding FX service provision is greater than ever,” added Kot.

Unlike many other asset classes, FX has never had a central exchange that represents a true picture of the market, so the idea of reducing transparency is relative.

Inter-dealer trading and the lack of a central price discovery mechanism for FX can make it more difficult for market participants to get a clear picture of the supply and demand dynamics and this can limit their ability to determine fair value.

However, it is important to note that inter-dealer trading also provides significant benefits, such as increasing liquidity and offering more efficient price discovery.

That is the view of Gerald Melia, the Head of Sales at StoneX Pro, who believes that the impact of inter-dealer trading on transparency may vary depending on the specific market and measures that are in place to promote transparency.

“For example, we have seen an increase in the popularity and demand for listed FX futures,” Melia pointed out. “FX Futures add more transparency so this indicates that this is what the market wants. We feel that the FX market operates optimally when OTC and listed FX futures co-habit in the same market.”

Melia is unconcerned about the potential impact of the shift towards bilateral forms of trading on price discovery, observing that professional FX clients are highly informed and that many have a background in treasury and finance.

“Additionally, markets have become less opaque with the availability of market data and industry benchmarks,” he says. “In saying that, we recommend that FX participants access and utilise consultants with FX, finance and capital market experience and leverage their experience and knowledge to maximise the benefits of new technology and trading venues.”

Sushko attributes the decline in dealer trading with customers to the risk-off environment. Mordelet agrees that this is a significant factor, although he also refers to a decrease in risk appetite from larger banks and more interest in reducing risk, either across internal desks or externally through interest-based quoting.

The BIS survey attributes some of the decline in dealer-customer trading to the contraction in international investment likely, resulting in a reduction in gross external portfolio positions. It further noted the decline in the market share of principal trading firms, which may be a function of these firms migrating to other asset classes with greater opportunities.

“However, it is also likely that the improvement of technology amongst dealers has also contributed to the decline in principal trading firms’ market share,” said Kot. “Pricing and execution algorithms have become more sophisticated, and the depth and persistence of liquidity from dealers is more highly valued during volatile market conditions.”

Most current forecasts for the economy and markets are negative or, at best, uncertain, and this drives investors from risk-on assets such as stocks, junk bonds and emerging market currencies to safer assets like government bonds, gold and developed country currencies.

“This can have a short term volume-increasing effect as investments move to safe haven assets, usually denominated in more stable currencies,” stated Melia. “Once this cycle of migration of capital has been completed, FX volumes naturally decrease.”

But, he acknowledged that this is not the full story since risk-off usually refers to the narrow spectrum of investments and risk management and ignores corporate investment. As the economic outlook worsens and uncertainty prevails, companies pull back on ordering raw materials and investments in projects to increase their international market share.

“This, in turn, can lead to changes in FX trading/hedging strategies as companies adjust their positions based on their outlook for different currencies and the perceived level of risk in those markets,” concluded Melia.

Paul Golden is an experienced freelance financial journalist with a strong institutional background. Over the past two decades, he has written for globally recognised financial publications, covering topics such as market structure, regulation, trading behaviour, and economic policy.

Financial Commission Approves Monstrade Giving Clients Mediation and €20K Coverage

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights