An extensive research by Forex Magnates informs readers of what is new and what is not, regarding recent rules that went into effect for firms authorised and/or registered with the UK's Financial Conduct Authority.

A busy start for the new year as the UK's Financial Conduct Authority (FCA) had several of its existing rules in its member-handbook go into effect on January 1st, 2014, and applicable to its regulated and registered firms, such as companies engaged in Foreign Exchange including CFDs and other FCA regulated activities in the UK by online brokers.

A large number of investment firms subject to the Capital Requirements Directive (CRD), under the UK FCA, had the latest version of the legislation under– CRD IV – also come into effect on January 1st, 2014.

The very next day the FCA put out a warning of two websites that were attempting to clone or mimic reputable websites of established FCA firms, in an effort prevent clients from getting scammed by the fake websites trying to trick them into thinking they were [the real] FCA regulated firms. Links to the two warnings can be found here below:

Both of the above clone-warnings remind us of the importance to confirm that the URL of a website when visiting it, clicking it, or even when embedded in what could appear on the surface like the real site, is valid. This is more important than ever as sophisticated phishing, viruses, malware and scammers could be lurking.

What's New in 2014?

The EU directive that helps implements the Basel III agreement, under CRD IV, contains a package of proposals to increase the prudential soundness of banks and its implementation is also designed to cover certain MiFID firms. There were approximately 100 technical standards which the European Banking Authority (EBA) published both before and after 1st of January, 2014 (and/or to be published in 2014), according to a prior announcement at the end of 2013 (when that number estimate was given).

As the independent body that regulates financial firms providing services to consumers has further clenched its hold on its member’s obligations under its authority, after proposals in 2013 and consultation papers – the latter of which is about to have its public comment period close in less than 10 days, changes are aimed to better protect participants and increase investor confidence in the UK as an attractive market destination for both traders and brokerages.

The rules –already under the scope of general rules pertaining to members' obligations under FCA regulations- are positioned to provide greater responsibility surrounding, promotions, bonuses, certain disclosures, suitability reports, and the manner in which firms refer to their FCA regulatory or registration status, even for EEA passported firms registered with the FCA, but not directly regulated in the UK.

What's Not New in 2014?

It seems the last time the handbook was updated was when the FSA posted about it on their now defunct website, as the FCA has already transitioned into power: see https://www.fsa.gov.uk/static/pubs/policy/ps13-05.pdf [note: the FSA site is no longer updated, see FCA site for updates]

Under the Financial Conduct Authority’s Handbook, under Business Standards, in the Conduct of Business Sourcebook (COBS), section 4.2 regarding Communicating with clients, including financial promotions (COBS 4), titled “Fair, clear and not misleading communications,” includes:

(1) A firm must ensure that a communication or a financial promotion is fair, clear and not misleading.

(2) This rule applies in relation to:

a communication by the firm to a client in relation to designated investment business other than a third party prospectus;

(b) a financial promotion communicated by the firm that is not:

i. an excluded communication;

ii. a non-retail communication;

iii. a third party prospectus; and

iv. a financial promotion approved by the firm.

[Note: article 19(2) of MiFID,1 recital 52 to the MiFID implementing Directive and article 77 of the UCITS Directive]

2) SUITABILITY - related

https://fshandbook.info/FS/html/FCA/COBS/9

https://fshandbook.info/FS/html/FCA/COBS/9/2

https://fshandbook.info/FS/html/FCA/COBS/9/4

COBS section 9, on Suitability, including basic advice, and 9.2 on assessing suitability, includes under section 9.4. about Suitability Reports which require that firms provide a suitability report to clients in certain circumstances, such as in the excerpted sections from 9.4 of the handbook:

A firm must provide a suitability report to a retail client if the firm makes a personal recommendation to the client and the client subsequently acquires or offloads a position (established or closes) in various financial investment products, and referenced article 19(8) of MiFID. Further within section 9, firms are required to take reasonable steps to ensure that a personal recommendation, or a decision to trade, is suitable for its client.

3) TIED AGENTS and APPOINTED REPS –related

https://fshandbook.info/FS/html/FCA/SUP/12

https://fshandbook.info/FS/html/FCA/SUP/12/3

https://fshandbook.info/FS/html/FCA/SUP/12/4

https://fshandbook.info/FS/html/FCA/SUP/12/6

Under Regulatory Processes, in the FCA handbook, in the SUP Supervision section 12 about appointed representatives, states the continuing obligations that firms with appointed representatives or EEA tied agents, in addition to key responsibilities firms have for its appointed representatives, as well as what a firm must do once it appoints an appointed representative or an EEA tied agent.

For example, under section 12.6.7 in SUP, it states : The senior management of a firm should be aware that the activities of appointed representatives are an integral part of the business that they manage. The responsibility for the control and monitoring of the activities of appointed representatives rests with the senior management of the firm.

These appear to have already been in place for some time, and not something new as reported by other publications.

4) DISCLOSURES -related

https://fshandbook.info/FS/html/FCA/GEN/4

https://fshandbook.info/FS/html/FCA/GEN/4/Annex1

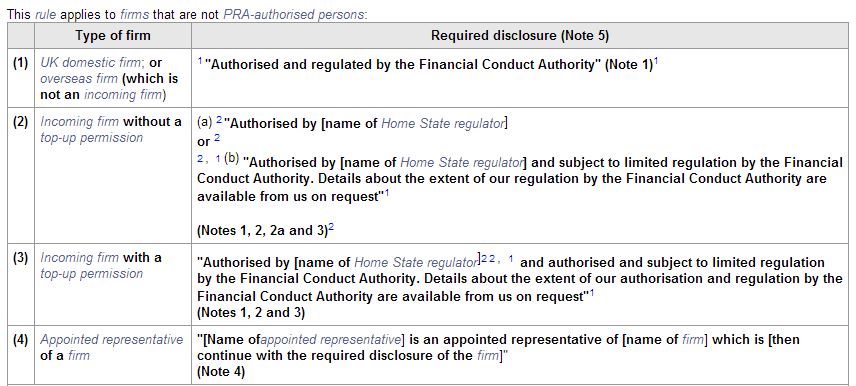

Under its General Provisions (GEN) section of the handbook, the FCA lists under GEN4 Annex 1, the statutory status disclosures that certain firms must make, include general rules applicable under GEN4, and state how certain disclosures and proper wording must be adhered to in communications with customers and when referencing the firms regulatory status, such as the excerpt below from GEN4.3 on Letter disclosure:

A firm must take reasonable care to ensure that every letter (or electronic equivalent) which it or its employees send to a1 retail client1, with a view to, or in connection with the firm carrying on a regulated activity, includes the disclosure in GEN 4 Annex 1 R (firms that are not PRA-authorised persons) or GEN 4 Annex 1AR (PRA-authorised persons) as applicable2.3

Example of the required text on Annex 1 of GEN4, include:

The following footnotes were included along with the above excerpt of Annex1 from GEN4:

Note 1 = A firm must use the formulation "Financial Conduct Authority" and not the abbreviated formulation "FCA".

Note 2 = An incoming firm is free to translate the name of its Home State regulator into English if it wishes. In doing so, it must ensure that the State in which the regulator is based is clear.

Note 2a = An incoming firm without a top-up permission may make either disclosure (a) or disclosure (b) unless it otherwise indicates or implies to the customer that it is regulated or supervised by the FCA, in which case it must make disclosure (b).

Note 4 = If the appointed representative has more than one principal, the disclosure must relate to the principal or principals responsible for the regulated activity or activities concerned. The required disclosure of the firm is that which would apply were the firm to make the disclosure under the rules applicable to it.

Note 5 = Any firm listed in this table is permitted to add words to the relevant required disclosure statement but only if the firm has taken reasonable steps to satisfy itself that the presentation of its statutory status will, as a consequence, be fair, clear and not misleading and be likely to be understood by the average member of the group to whom it is directed or by whom it is likely to be received. For example, an authorised professional firm may wish to make it clear that it is also regulated by its professional body.

[note: the above citations are not meant to be final as the information may be updated subsequently on the FCA website, and is not complete as they are excerpts taken from a longer text where other information was omitted from inclusion herein - for convenience.]

In addition, as per information posted on the now inactive FSA website, the previous name/website predecessor to the FCA, firms will have till 1st April, 2014 to run any old stocks of documentation, such as letterheads with the FSA information, and make the changes to wherever else their status is disclosed where the new attributions to regulatory status must be made, as well as firms no longer permitted use the FSA logo nor ability to use the FCA or PRA logos, respectively. For firms using these, in any format whatsoever, whether referenced electronically, in email or print, they will have until 1st April, 2014 to run down any old stocks, as per the notice in April 2013.

Changes to the FCA Member Handbook that were effective January 1st, 2014

Using a simple advanced search on the FCA website,the following 6 results were returned, with effective dates of January 1st, 2014, and directly related to FX :

Remuneration due on the basis of contracts concluded before 1st January, 2014 which is awarded or paid on or after 1 January, 2014 … and remuneration awarded, but not yet paid, before 1st January, 2014, for services provided in 2013

Remuneration due on the basis of contracts concluded before 1st January, 2011 which is awarded or paid on or after 1st January, 2011 … and remuneration awarded, but not yet paid, before 1st January, 2011, for services provided in 2010...[...]

Intangible assets are the full balance sheet value of goodwill (but not until 14th January, 2008 - see transitional provision 1), capitalised development costs, brand names, trademarks and similar rights and licences … and c = the amount of its intangible assets (but not goodwill until 14th January, 2008...[...]

And any valuation by the standing independent valuer must be undertaken in accordance with UKPS 2.3 of the RICS Valuation Standards (The Red Book) (6th edition published January 2008), or in the case of overseas immovables on an appropriate basis, but subject to COLL 6.3 (Valuation and pricing...[...]

However, in line with article 163 of the CRD , the Banking Consolidation Directive and the Capital Adequacy Directive are repealed from 1st January,2014 and references to these directives are replaced with references to the CRD and the EU CRR in line with the correlation table set out in Annex II to...[...]

For up-to-date Forex Industry Research, stay tuned to the upcoming release of the recently redesigned Forex Magnates Quarterly Industry Report (QIR) for the fourth quarter (QIR4) for 2013.

A busy start for the new year as the UK's Financial Conduct Authority (FCA) had several of its existing rules in its member-handbook go into effect on January 1st, 2014, and applicable to its regulated and registered firms, such as companies engaged in Foreign Exchange including CFDs and other FCA regulated activities in the UK by online brokers.

A large number of investment firms subject to the Capital Requirements Directive (CRD), under the UK FCA, had the latest version of the legislation under– CRD IV – also come into effect on January 1st, 2014.

The very next day the FCA put out a warning of two websites that were attempting to clone or mimic reputable websites of established FCA firms, in an effort prevent clients from getting scammed by the fake websites trying to trick them into thinking they were [the real] FCA regulated firms. Links to the two warnings can be found here below:

Both of the above clone-warnings remind us of the importance to confirm that the URL of a website when visiting it, clicking it, or even when embedded in what could appear on the surface like the real site, is valid. This is more important than ever as sophisticated phishing, viruses, malware and scammers could be lurking.

What's New in 2014?

The EU directive that helps implements the Basel III agreement, under CRD IV, contains a package of proposals to increase the prudential soundness of banks and its implementation is also designed to cover certain MiFID firms. There were approximately 100 technical standards which the European Banking Authority (EBA) published both before and after 1st of January, 2014 (and/or to be published in 2014), according to a prior announcement at the end of 2013 (when that number estimate was given).

As the independent body that regulates financial firms providing services to consumers has further clenched its hold on its member’s obligations under its authority, after proposals in 2013 and consultation papers – the latter of which is about to have its public comment period close in less than 10 days, changes are aimed to better protect participants and increase investor confidence in the UK as an attractive market destination for both traders and brokerages.

The rules –already under the scope of general rules pertaining to members' obligations under FCA regulations- are positioned to provide greater responsibility surrounding, promotions, bonuses, certain disclosures, suitability reports, and the manner in which firms refer to their FCA regulatory or registration status, even for EEA passported firms registered with the FCA, but not directly regulated in the UK.

What's Not New in 2014?

It seems the last time the handbook was updated was when the FSA posted about it on their now defunct website, as the FCA has already transitioned into power: see https://www.fsa.gov.uk/static/pubs/policy/ps13-05.pdf [note: the FSA site is no longer updated, see FCA site for updates]

Under the Financial Conduct Authority’s Handbook, under Business Standards, in the Conduct of Business Sourcebook (COBS), section 4.2 regarding Communicating with clients, including financial promotions (COBS 4), titled “Fair, clear and not misleading communications,” includes:

(1) A firm must ensure that a communication or a financial promotion is fair, clear and not misleading.

(2) This rule applies in relation to:

a communication by the firm to a client in relation to designated investment business other than a third party prospectus;

(b) a financial promotion communicated by the firm that is not:

i. an excluded communication;

ii. a non-retail communication;

iii. a third party prospectus; and

iv. a financial promotion approved by the firm.

[Note: article 19(2) of MiFID,1 recital 52 to the MiFID implementing Directive and article 77 of the UCITS Directive]

2) SUITABILITY - related

https://fshandbook.info/FS/html/FCA/COBS/9

https://fshandbook.info/FS/html/FCA/COBS/9/2

https://fshandbook.info/FS/html/FCA/COBS/9/4

COBS section 9, on Suitability, including basic advice, and 9.2 on assessing suitability, includes under section 9.4. about Suitability Reports which require that firms provide a suitability report to clients in certain circumstances, such as in the excerpted sections from 9.4 of the handbook:

A firm must provide a suitability report to a retail client if the firm makes a personal recommendation to the client and the client subsequently acquires or offloads a position (established or closes) in various financial investment products, and referenced article 19(8) of MiFID. Further within section 9, firms are required to take reasonable steps to ensure that a personal recommendation, or a decision to trade, is suitable for its client.

3) TIED AGENTS and APPOINTED REPS –related

https://fshandbook.info/FS/html/FCA/SUP/12

https://fshandbook.info/FS/html/FCA/SUP/12/3

https://fshandbook.info/FS/html/FCA/SUP/12/4

https://fshandbook.info/FS/html/FCA/SUP/12/6

Under Regulatory Processes, in the FCA handbook, in the SUP Supervision section 12 about appointed representatives, states the continuing obligations that firms with appointed representatives or EEA tied agents, in addition to key responsibilities firms have for its appointed representatives, as well as what a firm must do once it appoints an appointed representative or an EEA tied agent.

For example, under section 12.6.7 in SUP, it states : The senior management of a firm should be aware that the activities of appointed representatives are an integral part of the business that they manage. The responsibility for the control and monitoring of the activities of appointed representatives rests with the senior management of the firm.

These appear to have already been in place for some time, and not something new as reported by other publications.

4) DISCLOSURES -related

https://fshandbook.info/FS/html/FCA/GEN/4

https://fshandbook.info/FS/html/FCA/GEN/4/Annex1

Under its General Provisions (GEN) section of the handbook, the FCA lists under GEN4 Annex 1, the statutory status disclosures that certain firms must make, include general rules applicable under GEN4, and state how certain disclosures and proper wording must be adhered to in communications with customers and when referencing the firms regulatory status, such as the excerpt below from GEN4.3 on Letter disclosure:

A firm must take reasonable care to ensure that every letter (or electronic equivalent) which it or its employees send to a1 retail client1, with a view to, or in connection with the firm carrying on a regulated activity, includes the disclosure in GEN 4 Annex 1 R (firms that are not PRA-authorised persons) or GEN 4 Annex 1AR (PRA-authorised persons) as applicable2.3

Example of the required text on Annex 1 of GEN4, include:

The following footnotes were included along with the above excerpt of Annex1 from GEN4:

Note 1 = A firm must use the formulation "Financial Conduct Authority" and not the abbreviated formulation "FCA".

Note 2 = An incoming firm is free to translate the name of its Home State regulator into English if it wishes. In doing so, it must ensure that the State in which the regulator is based is clear.

Note 2a = An incoming firm without a top-up permission may make either disclosure (a) or disclosure (b) unless it otherwise indicates or implies to the customer that it is regulated or supervised by the FCA, in which case it must make disclosure (b).

Note 4 = If the appointed representative has more than one principal, the disclosure must relate to the principal or principals responsible for the regulated activity or activities concerned. The required disclosure of the firm is that which would apply were the firm to make the disclosure under the rules applicable to it.

Note 5 = Any firm listed in this table is permitted to add words to the relevant required disclosure statement but only if the firm has taken reasonable steps to satisfy itself that the presentation of its statutory status will, as a consequence, be fair, clear and not misleading and be likely to be understood by the average member of the group to whom it is directed or by whom it is likely to be received. For example, an authorised professional firm may wish to make it clear that it is also regulated by its professional body.

[note: the above citations are not meant to be final as the information may be updated subsequently on the FCA website, and is not complete as they are excerpts taken from a longer text where other information was omitted from inclusion herein - for convenience.]

In addition, as per information posted on the now inactive FSA website, the previous name/website predecessor to the FCA, firms will have till 1st April, 2014 to run any old stocks of documentation, such as letterheads with the FSA information, and make the changes to wherever else their status is disclosed where the new attributions to regulatory status must be made, as well as firms no longer permitted use the FSA logo nor ability to use the FCA or PRA logos, respectively. For firms using these, in any format whatsoever, whether referenced electronically, in email or print, they will have until 1st April, 2014 to run down any old stocks, as per the notice in April 2013.

Changes to the FCA Member Handbook that were effective January 1st, 2014

Using a simple advanced search on the FCA website,the following 6 results were returned, with effective dates of January 1st, 2014, and directly related to FX :

Remuneration due on the basis of contracts concluded before 1st January, 2014 which is awarded or paid on or after 1 January, 2014 … and remuneration awarded, but not yet paid, before 1st January, 2014, for services provided in 2013

Remuneration due on the basis of contracts concluded before 1st January, 2011 which is awarded or paid on or after 1st January, 2011 … and remuneration awarded, but not yet paid, before 1st January, 2011, for services provided in 2010...[...]

Intangible assets are the full balance sheet value of goodwill (but not until 14th January, 2008 - see transitional provision 1), capitalised development costs, brand names, trademarks and similar rights and licences … and c = the amount of its intangible assets (but not goodwill until 14th January, 2008...[...]

And any valuation by the standing independent valuer must be undertaken in accordance with UKPS 2.3 of the RICS Valuation Standards (The Red Book) (6th edition published January 2008), or in the case of overseas immovables on an appropriate basis, but subject to COLL 6.3 (Valuation and pricing...[...]

However, in line with article 163 of the CRD , the Banking Consolidation Directive and the Capital Adequacy Directive are repealed from 1st January,2014 and references to these directives are replaced with references to the CRD and the EU CRR in line with the correlation table set out in Annex II to...[...]

For up-to-date Forex Industry Research, stay tuned to the upcoming release of the recently redesigned Forex Magnates Quarterly Industry Report (QIR) for the fourth quarter (QIR4) for 2013.

Capital Index UK Changes Name to Vantos Markets Following Tough Trading Year

Featured Videos

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights