The FSA is effectively outsourcing its supervisory powers to overseas regulators.

RegTech has been cutting costs, streamlining processes and shortening times-to-market for decades.

Op-ed

The Bad Kind of Glocal

'Glocal' is a term mostly used positively to describe

something which enjoys both the advantages of a global mindset and the benefits

of a local community.

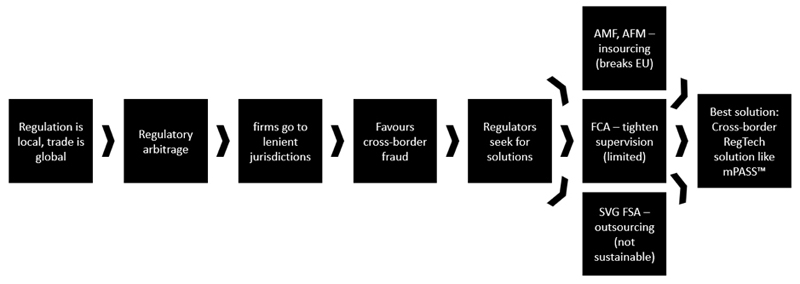

However, 'Glocal' has its dark side, too. For example, since

regulation is local, but trade is global, companies are incentivised to set shop

in a jurisdiction whose regulatory and supervisory regimes are relatively

lenient and provide services from there.

The combination of a jurisdiction with a lenient regulatory

and supervisory regime, as well as companies who choose to set shop in it for that

reason, make it very hard for those who see themselves deceived by said

companies to recover their funds from them.

Therefore, 'Glocal' doesn’t always mean enjoying the best

of the two; it can sometimes actually be suffering their worst.

The Regulatory Challenge and Process

Insourcing – the French and Dutch Approach to Regtech

The above-described phenomenon is nothing new, of course.

What is new is the way regulators are attempting to deal with it?

In December 2021 the AFM and AMF (French and Dutch

regulators) published a very unusual joint

statement, in which they stated they “increasingly observe practices of

financial firms obtaining a license and European passport in other EU member

states than that of their target audience,” and that these firms especially

are prominent when it comes to “offering high-risk products (such as CFDs)

as well as in terms of the complaints received from consumers on their

practices”.

Therefore, the AFM and AMF asked to transfer supervision

over those firms to them – a quite dramatic move, as it contradicts the

very notion of a unified European market.

Effectively, what the AFM and AMF were saying was that they

no longer wish to 'outsource' the supervision over French and Dutch residents

to other EU regulators; and wish to 'insource' the supervision back to them.

Apart from being contradictory to the very notion of the EU,

this type of 'reverse supervision' seems also quite impractical, as both the

criteria for its imposing are fluid and imprecise, at best; and as the actual

abilities of a regulatory authority to exercise effective supervision over a body

in a different jurisdiction is unclear.

Outsourcing – the Saint Vincent and Grenadine Approach

Just over a year later, on January 6, 2023, the Saint

Vincent and the Grenadines (SVG) Financial Services Authority (FSA) took the

exact opposite approach.

In a memorandum titled “Requirements for Business

Companies (BCs) and Limited Liability Companies (LLCs) Engaging in Forex

Business Activity,” the FSA stated the following:

“Owing to the sharp increase in the frequency and number

of complaints and allegations of fraud against SVG registered BCs and LLCs

which are engaged in FOREX trading or brokerage and the potential detrimental

effects on the reputation of St. Vincent and the Grenadines as an International

Financial Centre, the Financial Services Authority (FSA) has adopted the

following policy decision… Companies

wishing to engage in FOREX business must provide a certified copy of requisite

licences/approval from the jurisdiction(s)/authorities where their business

activities will be conducted…”

Remonda Kirketerp-Moller, Founder and CEO, Muinmos

Without such evidence, states the memorandum, applications

for new licenses will be rejected; and existing brokers have until 10.03.23 to

provide said evidence to the FSA, or risk being sanctioned.

This is a very unusual step taken by the FSA. Of course, strictly

speaking, in order to legally operate in a jurisdiction, one usually requires

to obtain a license there (there might also be other legal possibilities, though,

such as reverse solicitation or 'soft licensing' of various sorts).

However, here the FSA is effectively outsourcing its

supervisory powers to overseas regulators, saying it will only grant a license

(except for those who wish to operate only in SVG) to a firm that has been

previously licensed by a different regulatory authority.

This can be very effective, in the sense that the FSA

understands it cannot regulate the actions of financial institutions in their

operations elsewhere, and it is also aware firms are mis-using its license to

harm investors in those jurisdictions, and therefore wishes to remove from its

shores those specific firms who are interested in an unfair advantage.

However, this seems non-sustainable on a large scale, as it

is doubtful many regulators will follow suit. After all, this means that there

will be very little value to an offshore license. Also, not all regulators are able

to withstand the incentive to provide a lenient regulatory environment in order

to attract investments. And, this is before we even mention the paradox that

might be created, if ALL the regulators in the world (or at least many of them)

will implement a similar criterion…

Watch the recent FMLS22 panel discuss Regulation Roundup: Everything you need to know for 2023.

The Traditional Approach – Tightening Supervision

In December 2022, the FCA tackled the same issue of

cross-border trading. In a quite direct “Dear CEO” letter, the FCA highlighted

problems of bad practices in CFD trading, related among others to firms trading

in the UK via a temporary passporting regime, and made it clear it intends to

prioritise this issue, and expects firms to take clear action on this.

Contrary to the SVG FSA and the AMF, AFM approaches, the

FCA’s approach can be described as a “traditional” – tightening of supervision.

The advantages of this approach are clear; but so are its disadvantages. Among

other things, the FCA can only deal with the matter in its own “backyard”; and

that is, of course, only half the solution.

The Market Already Knows – Regulatory Challenges Are

Solved by Regulatory Technology

One regulator tightens its supervision; others ask to

insource it; another to outsource it. The variety of approaches is wide, and it

won’t come as too big of a surprise if a regulator would even choose to

ban electronic trading in their jurisdiction altogether (drastic as it may

sound). However, we would like to

suggest a better solution, harmonisation through technology.

As any market-maker or participant already knows, regulatory

challenges are solvable or at least are considerably eased by the use of

appropriate technology. Regulatory Technology solutions, or 'RegTech

solutions', have been cutting costs, streamlining processes and shortening

times-to-market for decades now, and are an essential and inseparable part of

the day-to-day practice of compliance, onboarding, reporting etc. teams in financial

institutions.

It makes perfect sense, then, to look for a RegTech solution

for this problem of cross-border trading as well. And, the solution exists, Muinmos’

mPASS™, an automated investor protection module, which automatically

categorises a client, assesses suitability and appropriateness, assigns it with

a risk profile etc., according to the legal systems of both the financial

institution’s domicile AND that of the client.

The implementation of such a system, of course, won’t solve

all the issues concerning cross-border trading. But, it will provide a much

better compliance starting point; can be implemented fast and at a relatively low cost; and is a lot more realistic than expecting all the regulators in the

world to ask for each other’s licenses before granting their own (something

that is also, as stated above, actually paradoxical).

Such is the power of RegTech: it can solve a regulatory

problem with relative ease and at a relatively fast pace, low cost, and to the

benefit of all regulators, firms and investors alike. In the context

discussed here, mPASS™ even presents a unique opportunity to create a unified

legal benchmark, thus eliminating regulatory arbitrage, proving that technology,

very much like trade, has the potential to transcend jurisdictional boundaries.

Remonda Kirketerp-Møller is the CEO/Founder of Muinmos

The Bad Kind of Glocal

'Glocal' is a term mostly used positively to describe

something which enjoys both the advantages of a global mindset and the benefits

of a local community.

However, 'Glocal' has its dark side, too. For example, since

regulation is local, but trade is global, companies are incentivised to set shop

in a jurisdiction whose regulatory and supervisory regimes are relatively

lenient and provide services from there.

The combination of a jurisdiction with a lenient regulatory

and supervisory regime, as well as companies who choose to set shop in it for that

reason, make it very hard for those who see themselves deceived by said

companies to recover their funds from them.

Therefore, 'Glocal' doesn’t always mean enjoying the best

of the two; it can sometimes actually be suffering their worst.

The Regulatory Challenge and Process

Insourcing – the French and Dutch Approach to Regtech

The above-described phenomenon is nothing new, of course.

What is new is the way regulators are attempting to deal with it?

In December 2021 the AFM and AMF (French and Dutch

regulators) published a very unusual joint

statement, in which they stated they “increasingly observe practices of

financial firms obtaining a license and European passport in other EU member

states than that of their target audience,” and that these firms especially

are prominent when it comes to “offering high-risk products (such as CFDs)

as well as in terms of the complaints received from consumers on their

practices”.

Therefore, the AFM and AMF asked to transfer supervision

over those firms to them – a quite dramatic move, as it contradicts the

very notion of a unified European market.

Effectively, what the AFM and AMF were saying was that they

no longer wish to 'outsource' the supervision over French and Dutch residents

to other EU regulators; and wish to 'insource' the supervision back to them.

Apart from being contradictory to the very notion of the EU,

this type of 'reverse supervision' seems also quite impractical, as both the

criteria for its imposing are fluid and imprecise, at best; and as the actual

abilities of a regulatory authority to exercise effective supervision over a body

in a different jurisdiction is unclear.

Outsourcing – the Saint Vincent and Grenadine Approach

Just over a year later, on January 6, 2023, the Saint

Vincent and the Grenadines (SVG) Financial Services Authority (FSA) took the

exact opposite approach.

In a memorandum titled “Requirements for Business

Companies (BCs) and Limited Liability Companies (LLCs) Engaging in Forex

Business Activity,” the FSA stated the following:

“Owing to the sharp increase in the frequency and number

of complaints and allegations of fraud against SVG registered BCs and LLCs

which are engaged in FOREX trading or brokerage and the potential detrimental

effects on the reputation of St. Vincent and the Grenadines as an International

Financial Centre, the Financial Services Authority (FSA) has adopted the

following policy decision… Companies

wishing to engage in FOREX business must provide a certified copy of requisite

licences/approval from the jurisdiction(s)/authorities where their business

activities will be conducted…”

Remonda Kirketerp-Moller, Founder and CEO, Muinmos

Without such evidence, states the memorandum, applications

for new licenses will be rejected; and existing brokers have until 10.03.23 to

provide said evidence to the FSA, or risk being sanctioned.

This is a very unusual step taken by the FSA. Of course, strictly

speaking, in order to legally operate in a jurisdiction, one usually requires

to obtain a license there (there might also be other legal possibilities, though,

such as reverse solicitation or 'soft licensing' of various sorts).

However, here the FSA is effectively outsourcing its

supervisory powers to overseas regulators, saying it will only grant a license

(except for those who wish to operate only in SVG) to a firm that has been

previously licensed by a different regulatory authority.

This can be very effective, in the sense that the FSA

understands it cannot regulate the actions of financial institutions in their

operations elsewhere, and it is also aware firms are mis-using its license to

harm investors in those jurisdictions, and therefore wishes to remove from its

shores those specific firms who are interested in an unfair advantage.

However, this seems non-sustainable on a large scale, as it

is doubtful many regulators will follow suit. After all, this means that there

will be very little value to an offshore license. Also, not all regulators are able

to withstand the incentive to provide a lenient regulatory environment in order

to attract investments. And, this is before we even mention the paradox that

might be created, if ALL the regulators in the world (or at least many of them)

will implement a similar criterion…

Watch the recent FMLS22 panel discuss Regulation Roundup: Everything you need to know for 2023.

The Traditional Approach – Tightening Supervision

In December 2022, the FCA tackled the same issue of

cross-border trading. In a quite direct “Dear CEO” letter, the FCA highlighted

problems of bad practices in CFD trading, related among others to firms trading

in the UK via a temporary passporting regime, and made it clear it intends to

prioritise this issue, and expects firms to take clear action on this.

Contrary to the SVG FSA and the AMF, AFM approaches, the

FCA’s approach can be described as a “traditional” – tightening of supervision.

The advantages of this approach are clear; but so are its disadvantages. Among

other things, the FCA can only deal with the matter in its own “backyard”; and

that is, of course, only half the solution.

The Market Already Knows – Regulatory Challenges Are

Solved by Regulatory Technology

One regulator tightens its supervision; others ask to

insource it; another to outsource it. The variety of approaches is wide, and it

won’t come as too big of a surprise if a regulator would even choose to

ban electronic trading in their jurisdiction altogether (drastic as it may

sound). However, we would like to

suggest a better solution, harmonisation through technology.

As any market-maker or participant already knows, regulatory

challenges are solvable or at least are considerably eased by the use of

appropriate technology. Regulatory Technology solutions, or 'RegTech

solutions', have been cutting costs, streamlining processes and shortening

times-to-market for decades now, and are an essential and inseparable part of

the day-to-day practice of compliance, onboarding, reporting etc. teams in financial

institutions.

It makes perfect sense, then, to look for a RegTech solution

for this problem of cross-border trading as well. And, the solution exists, Muinmos’

mPASS™, an automated investor protection module, which automatically

categorises a client, assesses suitability and appropriateness, assigns it with

a risk profile etc., according to the legal systems of both the financial

institution’s domicile AND that of the client.

The implementation of such a system, of course, won’t solve

all the issues concerning cross-border trading. But, it will provide a much

better compliance starting point; can be implemented fast and at a relatively low cost; and is a lot more realistic than expecting all the regulators in the

world to ask for each other’s licenses before granting their own (something

that is also, as stated above, actually paradoxical).

Such is the power of RegTech: it can solve a regulatory

problem with relative ease and at a relatively fast pace, low cost, and to the

benefit of all regulators, firms and investors alike. In the context

discussed here, mPASS™ even presents a unique opportunity to create a unified

legal benchmark, thus eliminating regulatory arbitrage, proving that technology,

very much like trade, has the potential to transcend jurisdictional boundaries.

Remonda Kirketerp-Møller is the CEO/Founder of Muinmos

Remonda Kirketerp-Møller, a qualified solicitor and a renowned expert in RegTech, Fintech and regulatory matters in financial services.

She has held senior executive positions at two highly successful, fast growth global firms, Saxo Bank and CFH Clearing, where she gained first hand experience about the complexities involved in compliance and onboarding.

Remonda founded Danish RegTech company, muinmos ApS in 2012 after spotting a gap in the market to use technology to automate highly complex legal and regulatory challenges in financial services, specifically in client onboarding.

With Remonda at the helm, Muinmos has won multiple awards for its innovative automated. AI-based onboarding solution and has been selected for the prestigious RegTech 100 for the last five consecutive years.

Remonda is also co-author of ‘The RegTech Book’ , published by Wiley in Summer 2019.

Financial Commission Approves Monstrade Giving Clients Mediation and €20K Coverage

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights