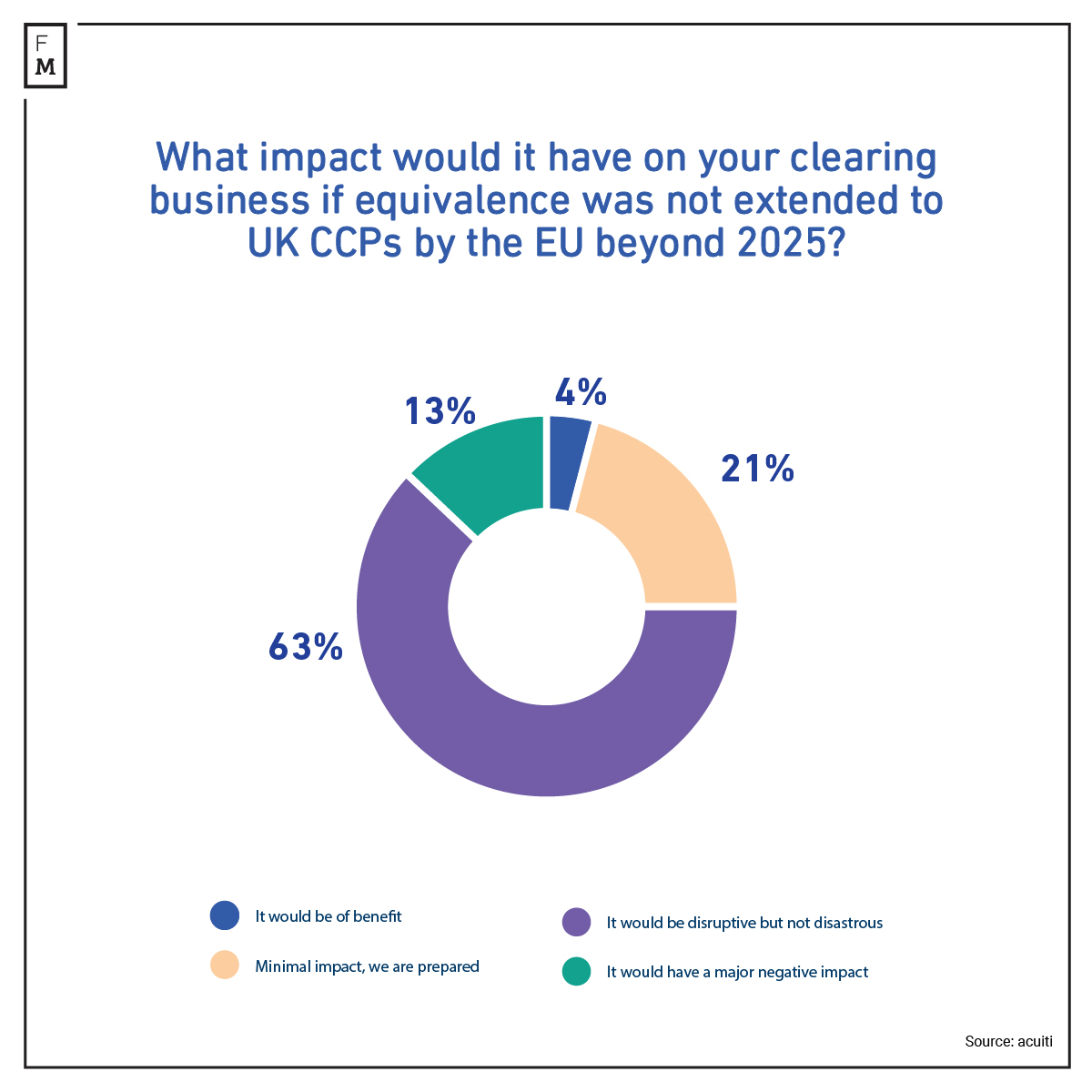

Among participants, 63% view the potential end to UK-EU equivalence in 2025 as disruptive but not disastrous.

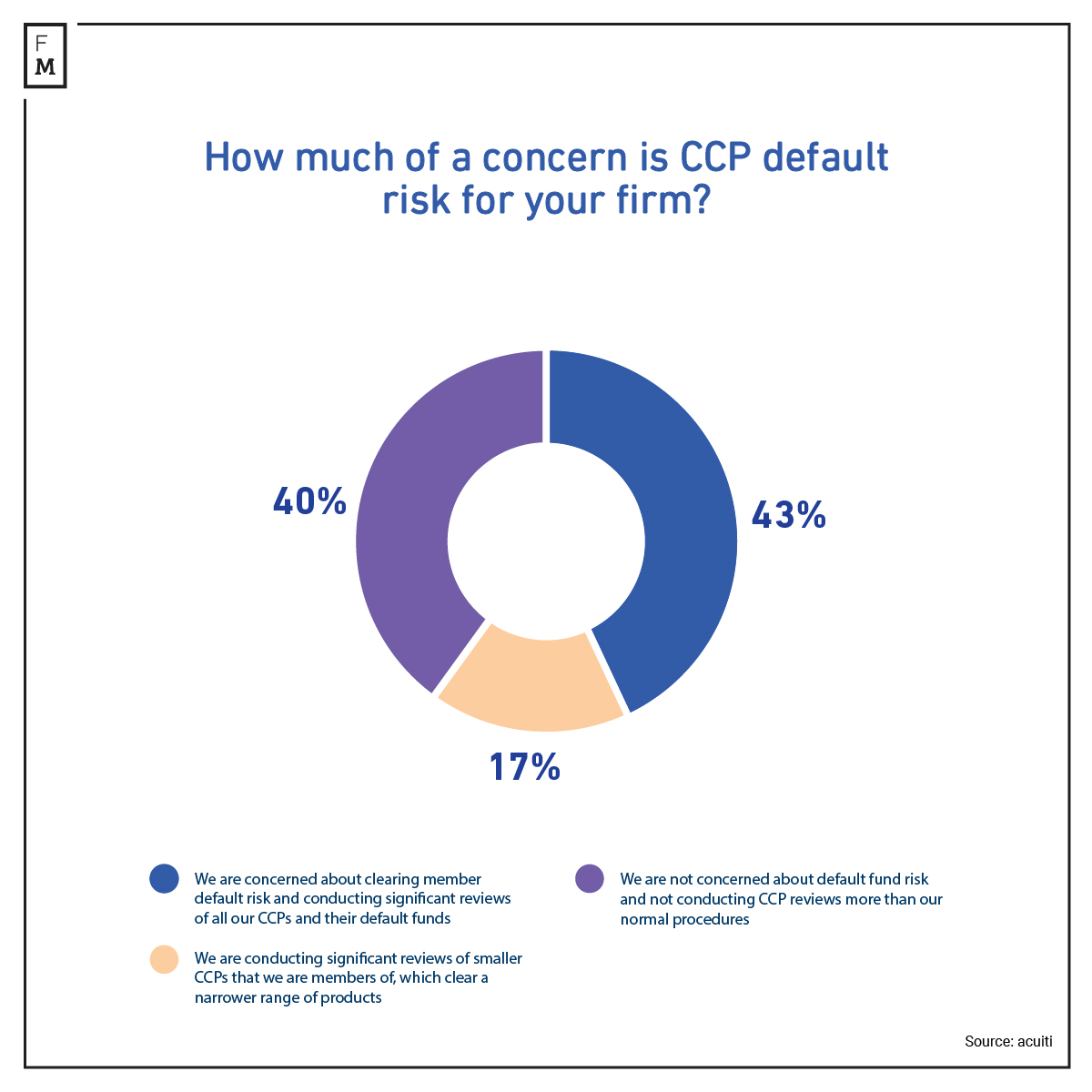

Less than half are reviewing default risk across all CCPs and default funds.

FM

The Q4 Sell-Side Clearing

Management Insight Report, produced in collaboration with report partner

HelloZero, focuses on streamlining futures and options data processing. This

quarter's analysis delves into EMIR 3.0, CCP default risk, DORA, manual

clearing training, and the Basel III endgame impact.

A comprehensive

examination of reconciliations explores changes and remaining challenges in

reducing operational risk and enhancing efficiency and customer service since

the 2021 study on sell-side listed derivatives market reconciliations.

Insights from the Sell-Side Clearing Industry

European regulators are

conducting a review of the EMIR framework, aiming to strengthen European

derivatives markets through central clearing of OTC instruments and reduce

reliance on third-country clearing houses post-Brexit.

The UK and EU, after agreeing on

equivalence to avoid regulatory disruptions, face a potential end to

equivalence in 2025. While the risk has diminished, market participants are

better prepared for a break, with 63% assuming it is disruptive but not

disastrous, signaling improved readiness compared to previous years.

EU Equivalence for UK CCPs

The increased volatility in

various asset classes has heightened the risk of defaulting on trading

positions, prompting clearing firms to focus on Central Counterparties (CCPs)

and the potential of default fund contributions.

Concerns about clearing member

default risk are widespread, with 43% conducting significant reviews of all

CCPs and their default funds. Some are particularly focused on

smaller CCPs, susceptible to volatility in a narrower range of products.

Overall, 40% express no concern about default fund risk and are not conducting

CCP reviews beyond normal procedures.

CCP Default Risk

Exchanges have been increasingly aiming

to establish a direct connection with end clients rather than relying on the

traditional sell-side intermediary. This shift has been driven by a desire to enhance

the visibility of who is trading on the exchange and to stimulate client demand

for new products and services.

While 55% of the network

acknowledges increased requests from exchanges for greater transparency and

visibility, concerns about the competitive threat from exchanges exist among

some, with almost half not entirely comfortable providing such information.

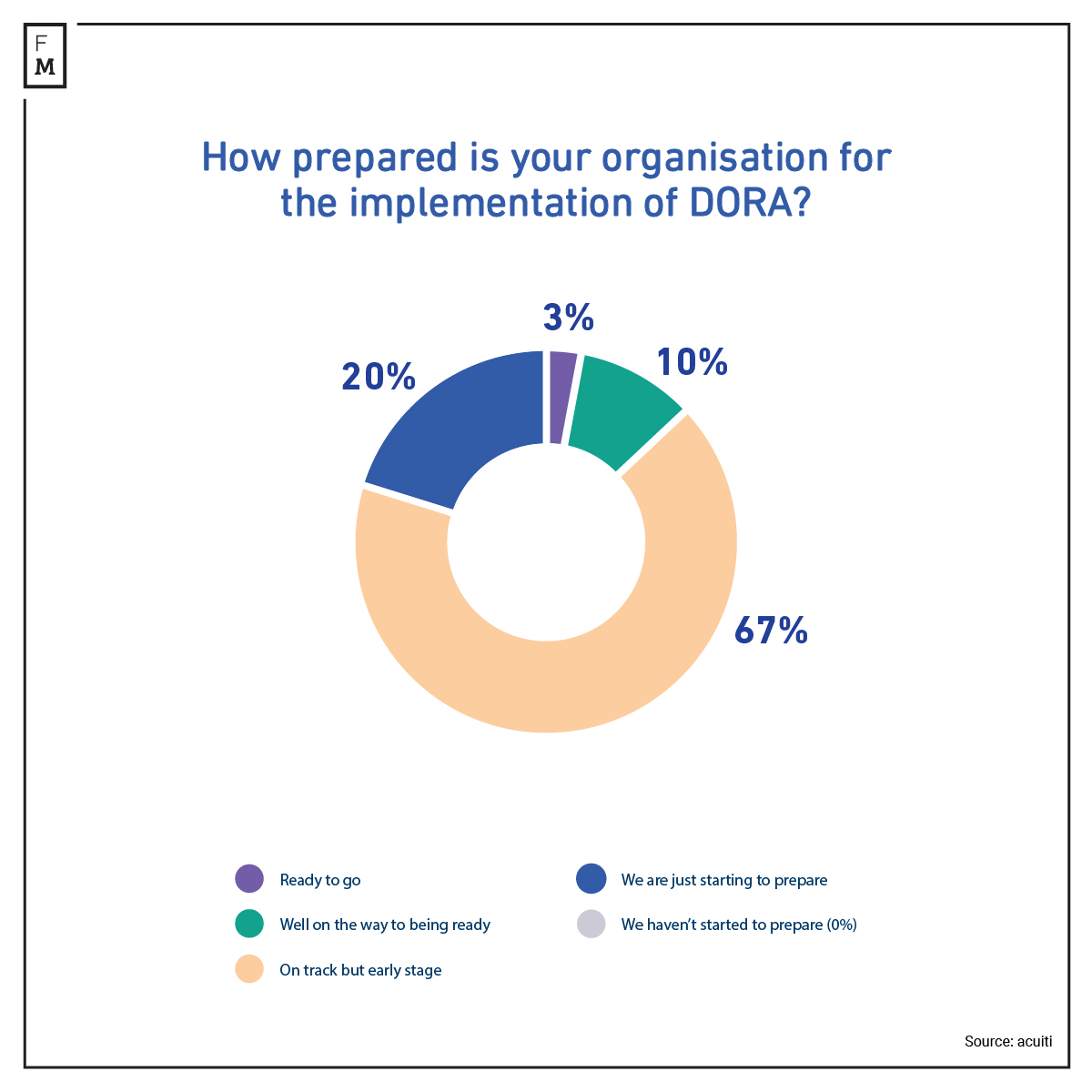

The EU's Digital Operational

Resilience Act (DORA), effective in early 2025, necessitates firms to map

third-party relationships and conduct extensive due diligence on digital supply

chains. Challenges in preparing for DORA

include operational resource allocation, understanding threat analysis

criteria, and obtaining information from vendors. Despite the compliance task's

magnitude, a majority, 67% of the network believes they are on track for DORA

readiness, with varying levels of preparation.

DORA Implementation

Banks,

alongside preparing for DORA, are anticipating the impact of the Basel III

endgame regulation. Global systemically important banks (G-SIBs) express concerns about potential increases in

regulatory capital requirements, with counterparty risk requirements identified

as having the most significant cost implications for clearing services. While

44% foresee cost implications, 25%currently see no significant

impact on the cost of clearing services from the Basel III endgame.

Since

March 2020, post the surge of Covid-19, clearing firms prioritized reconciliation system improvements. The 2021

Acuiti and HelloZero study highlighted industry-wide efforts, with a "good enough" attitude, and reliance on manual processes, and

spreadsheets, especially among tier 1 banks.

In

the last two years, 39% of firms, including 44% of tier 1 banks, fully

automated reconciliation processes, focusing on day-to-day efficiency, cost

reduction, and resource allocation to higher-value tasks. Significant

investments in reconciliation software, driven by the goal of increasing

efficiency and capacity, have been made by over two-thirds of respondents.

Larger

firms have shifted investment focus from headcount to automation. Currently, 2%

predominantly use manual processes, 59% partially automate, and 39% use fully

automated reconciliation for derivatives trades, showcasing widespread

integration of automated processes.

The

adoption of artificial

intelligence (AI) for reconciliation processes is in its early stages, with

58% of respondents in the investigation stage, 13% in early implementation, and

only 8% having fully implemented AI. This indicates a cautious approach to

leveraging AI to reduce dependencies, wage pressures, and operational

vulnerabilities in reconciliation systems.

Sell-side

firms in the derivatives industry have made significant strides in improving

reconciliation software efficiency since the 2021 Acuiti report. The use of

spreadsheets has decreased, automation has increased, and reliance on key staff

members has diminished.

While

not fully automated across the market, the continual investment in

reconciliations is having a positive impact on satisfaction levels, with over half of the respondents expressing satisfaction with their processes. However, intentions

to invest in reconciliation software are declining, with just under a fifth

planning to invest and over half not considering it, indicating a potential

risk despite the progress made since 2020.

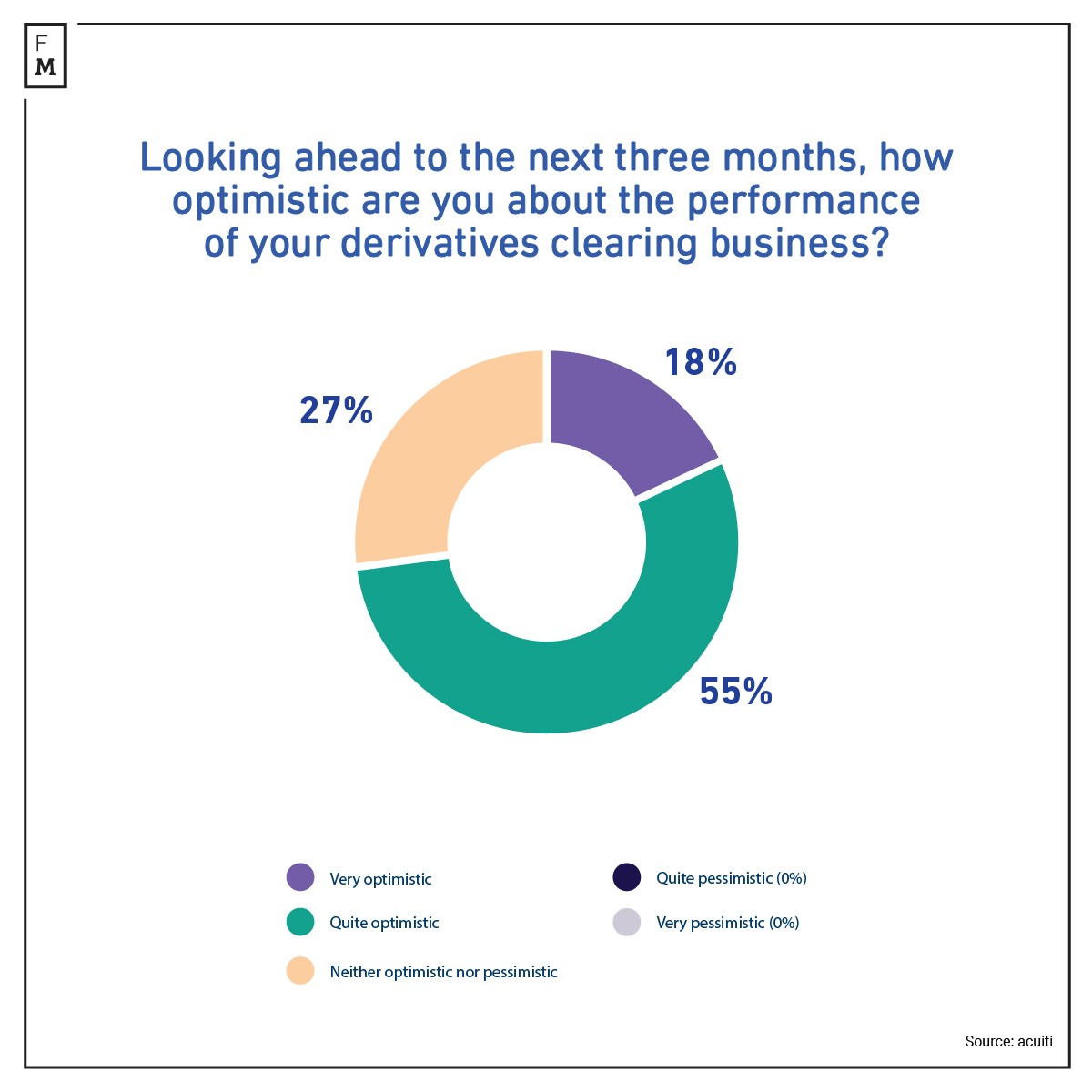

The

network has expressed optimism about the next three months' business prospects in

derivatives clearing, with a sentiment score of 73, marking an increase from

the previous quarter's score of 68. Among respondents, 18% are very optimistic, 55% are quite optimistic, although 27% remain neutral about the outlook.

Derivatives Clearing Business Performance

Sell-side

firms in derivatives have improved reconciliation software efficiency, reducing

reliance on spreadsheets and increasing automation. While

progress is evident, achieving a fully automated environment remains ongoing,

emphasizing continuous investment.

High

satisfaction levels suggest positive strides, but declining intentions to

invest pose risks, including capacity issues in volatile markets. Maintaining a

competitive edge requires ongoing investment, recognizing reconciliations as

crucial for success. Despite challenges, the overall optimism about business

prospects for the next three months indicates a positive outlook for the industry.

The Q4 Sell-Side Clearing

Management Insight Report, produced in collaboration with report partner

HelloZero, focuses on streamlining futures and options data processing. This

quarter's analysis delves into EMIR 3.0, CCP default risk, DORA, manual

clearing training, and the Basel III endgame impact.

A comprehensive

examination of reconciliations explores changes and remaining challenges in

reducing operational risk and enhancing efficiency and customer service since

the 2021 study on sell-side listed derivatives market reconciliations.

Insights from the Sell-Side Clearing Industry

European regulators are

conducting a review of the EMIR framework, aiming to strengthen European

derivatives markets through central clearing of OTC instruments and reduce

reliance on third-country clearing houses post-Brexit.

The UK and EU, after agreeing on

equivalence to avoid regulatory disruptions, face a potential end to

equivalence in 2025. While the risk has diminished, market participants are

better prepared for a break, with 63% assuming it is disruptive but not

disastrous, signaling improved readiness compared to previous years.

EU Equivalence for UK CCPs

The increased volatility in

various asset classes has heightened the risk of defaulting on trading

positions, prompting clearing firms to focus on Central Counterparties (CCPs)

and the potential of default fund contributions.

Concerns about clearing member

default risk are widespread, with 43% conducting significant reviews of all

CCPs and their default funds. Some are particularly focused on

smaller CCPs, susceptible to volatility in a narrower range of products.

Overall, 40% express no concern about default fund risk and are not conducting

CCP reviews beyond normal procedures.

CCP Default Risk

Exchanges have been increasingly aiming

to establish a direct connection with end clients rather than relying on the

traditional sell-side intermediary. This shift has been driven by a desire to enhance

the visibility of who is trading on the exchange and to stimulate client demand

for new products and services.

While 55% of the network

acknowledges increased requests from exchanges for greater transparency and

visibility, concerns about the competitive threat from exchanges exist among

some, with almost half not entirely comfortable providing such information.

The EU's Digital Operational

Resilience Act (DORA), effective in early 2025, necessitates firms to map

third-party relationships and conduct extensive due diligence on digital supply

chains. Challenges in preparing for DORA

include operational resource allocation, understanding threat analysis

criteria, and obtaining information from vendors. Despite the compliance task's

magnitude, a majority, 67% of the network believes they are on track for DORA

readiness, with varying levels of preparation.

DORA Implementation

Banks,

alongside preparing for DORA, are anticipating the impact of the Basel III

endgame regulation. Global systemically important banks (G-SIBs) express concerns about potential increases in

regulatory capital requirements, with counterparty risk requirements identified

as having the most significant cost implications for clearing services. While

44% foresee cost implications, 25%currently see no significant

impact on the cost of clearing services from the Basel III endgame.

Since

March 2020, post the surge of Covid-19, clearing firms prioritized reconciliation system improvements. The 2021

Acuiti and HelloZero study highlighted industry-wide efforts, with a "good enough" attitude, and reliance on manual processes, and

spreadsheets, especially among tier 1 banks.

In

the last two years, 39% of firms, including 44% of tier 1 banks, fully

automated reconciliation processes, focusing on day-to-day efficiency, cost

reduction, and resource allocation to higher-value tasks. Significant

investments in reconciliation software, driven by the goal of increasing

efficiency and capacity, have been made by over two-thirds of respondents.

Larger

firms have shifted investment focus from headcount to automation. Currently, 2%

predominantly use manual processes, 59% partially automate, and 39% use fully

automated reconciliation for derivatives trades, showcasing widespread

integration of automated processes.

The

adoption of artificial

intelligence (AI) for reconciliation processes is in its early stages, with

58% of respondents in the investigation stage, 13% in early implementation, and

only 8% having fully implemented AI. This indicates a cautious approach to

leveraging AI to reduce dependencies, wage pressures, and operational

vulnerabilities in reconciliation systems.

Sell-side

firms in the derivatives industry have made significant strides in improving

reconciliation software efficiency since the 2021 Acuiti report. The use of

spreadsheets has decreased, automation has increased, and reliance on key staff

members has diminished.

While

not fully automated across the market, the continual investment in

reconciliations is having a positive impact on satisfaction levels, with over half of the respondents expressing satisfaction with their processes. However, intentions

to invest in reconciliation software are declining, with just under a fifth

planning to invest and over half not considering it, indicating a potential

risk despite the progress made since 2020.

The

network has expressed optimism about the next three months' business prospects in

derivatives clearing, with a sentiment score of 73, marking an increase from

the previous quarter's score of 68. Among respondents, 18% are very optimistic, 55% are quite optimistic, although 27% remain neutral about the outlook.

Derivatives Clearing Business Performance

Sell-side

firms in derivatives have improved reconciliation software efficiency, reducing

reliance on spreadsheets and increasing automation. While

progress is evident, achieving a fully automated environment remains ongoing,

emphasizing continuous investment.

High

satisfaction levels suggest positive strides, but declining intentions to

invest pose risks, including capacity issues in volatile markets. Maintaining a

competitive edge requires ongoing investment, recognizing reconciliations as

crucial for success. Despite challenges, the overall optimism about business

prospects for the next three months indicates a positive outlook for the industry.

Nomura Partly Attributes 10% Profit Drop to Crypto Losses, Curbs Risk at Laser Digital

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights