The Chicago Mercantile Exchange has filed its annual report to the SEC today, containing some key currency trading metrics and shedding light on its evaluation of the markets and regulations.

In 2013, the estimated percentage of clearing and transaction fees revenue contributed by foreign exchange trading was 8% of the total revenues of all the CME's products, up from 7% in the previous two years. Average Daily Volume of foreign exchange contracts was 886,000 in 2013, up 4.9% from 2012.

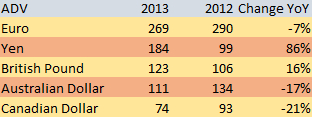

The overall increase in foreign exchange contract volume in 2013 was attributable to an increase in yen and GBP contract volumes. The increase in yen volume was largely due to higher Volatility resulting from reduced efforts by the Japanese central bank to control exchange rates in early 2013. Increased volatility and economic uncertainty within Great Britain in 2013 contributed to an overall increase in GBP contract volumes.

Key FX Products

As a result of a decrease in demand for commodity resources in China because of an economic slowdown in the Chinese market, demand decreased for currencies from countries that heavily depend on raw material exports, such as the Australian and Canadian dollars.

Over-the-Counter (OTC) Clearing

Writing about the effort to globalize its business, the CME report mentions that the group applied for regulatory approval to create CME Europe Limited, a London-based FCA supervised derivatives exchange. Pending approval, product offerings will range across multiple-asset classes beginning with foreign exchange.

According to the report, the group believes CME Europe will Leverage the central counterparty model and allow it to align more closely with its regional customers in both listed and OTC markets, providing additional opportunities to expanding its non-U.S. customer base.

Regarding the US market, the CME will continue to focus on new customer onboarding for swaps clearing services, expanding OTC product offerings and working with the buy and sell-sides. In 2013, three phases of the clearing mandate of the Dodd-Frank Wall Street Reform Act were implemented in the United States. During the year, the CME cleared OTC transactions worth more than $15.3 trillion, and open interest as of December 31, 2013 was $9.1 trillion.

Despite all of the above, the CME report states that "There is no guarantee that our OTC initiatives will be successful." As the regulatory environment for trading and clearing remains uncertain the group cannot be certain that it will be able to operate profitably under the new legislation.

The example given in the report, provisions within Dodd-Frank include changes to the CFTC's core principles, which could require modifications to the way certain contracts trade or require that such products be de-listed as futures and re-listed as swaps. Also, numerous capital changes and provisions in Basel III may result in uncleared, bilateral OTC derivatives being less expensive than cleared derivatives.

In addition, a number of market participants and exchanges have developed competing platforms and products, including new swap execution facilities. The group concludes that it cannot be certain it will be able to compete effectively or that its initiatives will be successful.