One of the revelations of the BIS's latest FX survey was that non-dealer institutions aren't only the largest segment of FX's $5.3 trillion market, but compose of the majority of it. We take a look at this important trend.

Sifting through the Bank of International Settlements (BIS) Triennial FX Survey, arguably the most important trend taking place is the growth of non-dealer bank participation. Within the report, the survey polls participant dealers in regards to trading details such as volumes by currency, counterparty type and region.

Topping the list of counterparties was the ‘other financial institution’ segment. Responsible for $2.8 trillion, or 53% of the survey’s $5.3 trillion a day total for global FX volumes, the segment includes smaller banks that do not act as dealers in the FX market, proprietary traders within investment banks, and institutional investors such as pension, hedge and mutual funds. Volumes in this group rose 48% from $1.9 trillion in 2010, to the most recent $2.8 trillion. During the 2010 survey the other financial institutions overtook reporting dealers, with market share continuing to climb over the last three years.

There are several factors that have led to the rising volumes of the non-dealer. Perhaps the main cause has been advances of electronic trading which has provided easier opportunities for Tier 2/3 banks to offer eFX solutions to their clients. Also, a factor is the dwindling profit margins posted on FX volumes, leading major banks to focus their marketing efforts to reach less competitive countries that provide the opportunity to achieve higher revenues per million dollars traded. As a result, banks in countries such as Poland, Turkey, as well as South-East Asian nations have become recent entrants to the eFX world.

On a more macro-level, globalization as a whole can’t be underestimated. As long as cross-boundary trade increases, so does demand among firms for foreign exchange services. This demand represents itself through the increased needs of businesses for FX solutions from regional banks. In addition, larger regional banks are able to leverage their expertise to price their local currency more aggressively to foreigners.

Explaining how technology has evolved the industry, Peter A. Bondesen, Sales Manager EMEA at FlexTrade stated to Forex Magnates that, “Improvements in technology that is available to firms is an important factor. For smaller banks, technology was a stumbling block to enter the FX market.” As a result, Bondesen added that new entrants aren’t only aggregating liquidity to resell it to their customers, but are using their “regional expertise in the local currency” to provide pricing to the rest of the world. Specifically, Bondesen noted that through implementation of eFX solutions, Scandinavian regional banks have succeeded to become the main markets in their respective currencies by connecting their liquidity to major financial centers and trading venues.

Due to the economic efficiencies available in technology, smaller firms are also able to source customized solutions to better fit both their buy and sell-side needs. Explaining this, Harpal Sandhu, CEO, Integral Development Corp added to Forex Magnates that, “Our experience is in line with what the BIS report states, which is that “smaller banks” and “institutional investors” are growth areas.” He added that, “We have seen a dramatic customer growth in these areas because these market participants require an OTC platform that offers the flexibility so they can do whatever they want with it, for their own benefits or those of their customers.”

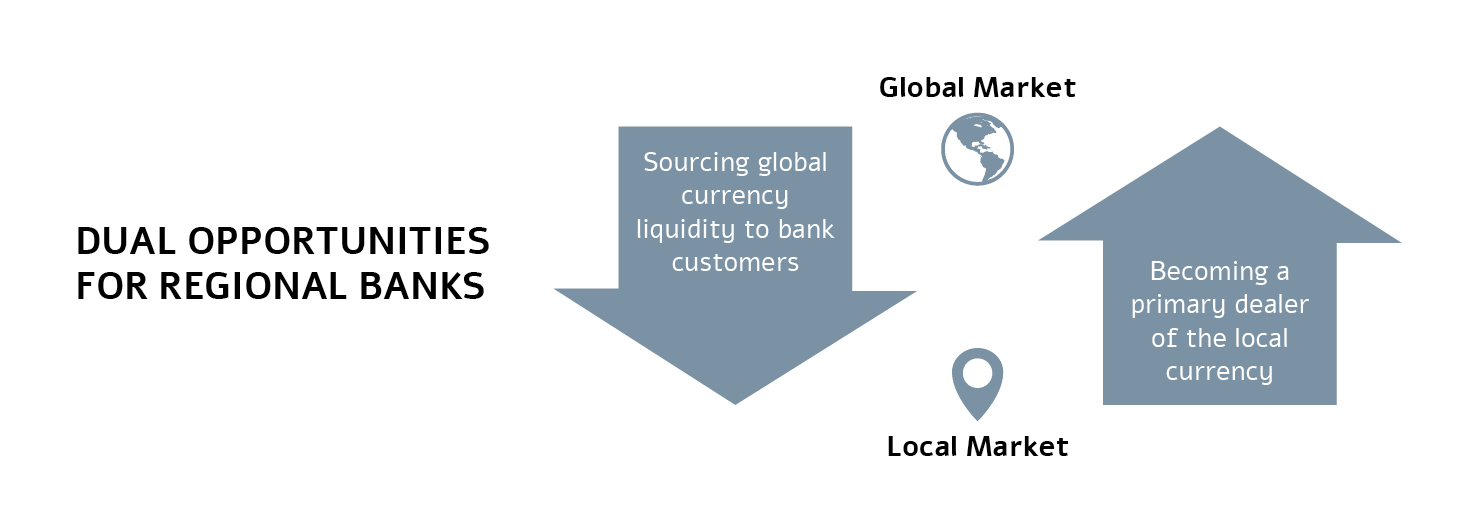

As a result, it is becoming a ‘two-way street’ where banks are able to grow their FX businesses by sourcing global pricing for their local customers, as well as becoming liquidity providers of their local currency to the rest of the world. Meeting this dual demand, Illit Geller, CEO of Tradair explained that there are “Two solutions categories; the ECN - where liquidity of the ECN can be rebranded by the regional bank for its customers, and liquidity optimization management (LOM) which provide a tier1 bank type solution for regional banks pricing and distribution."

Illit Geller, CEO of TradAir

In terms of technology, this had led to the creation of different types of products to fit the primary needs of banks. Geller explained that in regards to regional banks that are using their expertise to provide pricing of their local currency to the rest of the world, firms require greater customization and risk controls as she stated, “It is not enough to provide similar technology solutions to those of the 1st tier banks, regional banks require tight trader controls, different algorithms and workflow management suited for their unique currency needs.”

Similarly, firms seeking cost-efficient solutions to offer eFX services to clients are also witnessing an ever expanding product line to choose from, as providers like Integral have been offering solutions that require little to no upfront costs to launch. Having established client bases, these solutions allow regional banks to both resell prime dealer liquidity to their clients as well as price their own market-making initiatives. Although much of the initial business that regional banks are receiving is based on upselling services to existing clients, firms are also using the FX services to gain new customers. Over the long run, Bondesen believes that banks with the “Most efficient setups will be able to show this to customers to win clients. More than just reselling, they will be able to win new clients with great services.”

Fragmented but still centralized

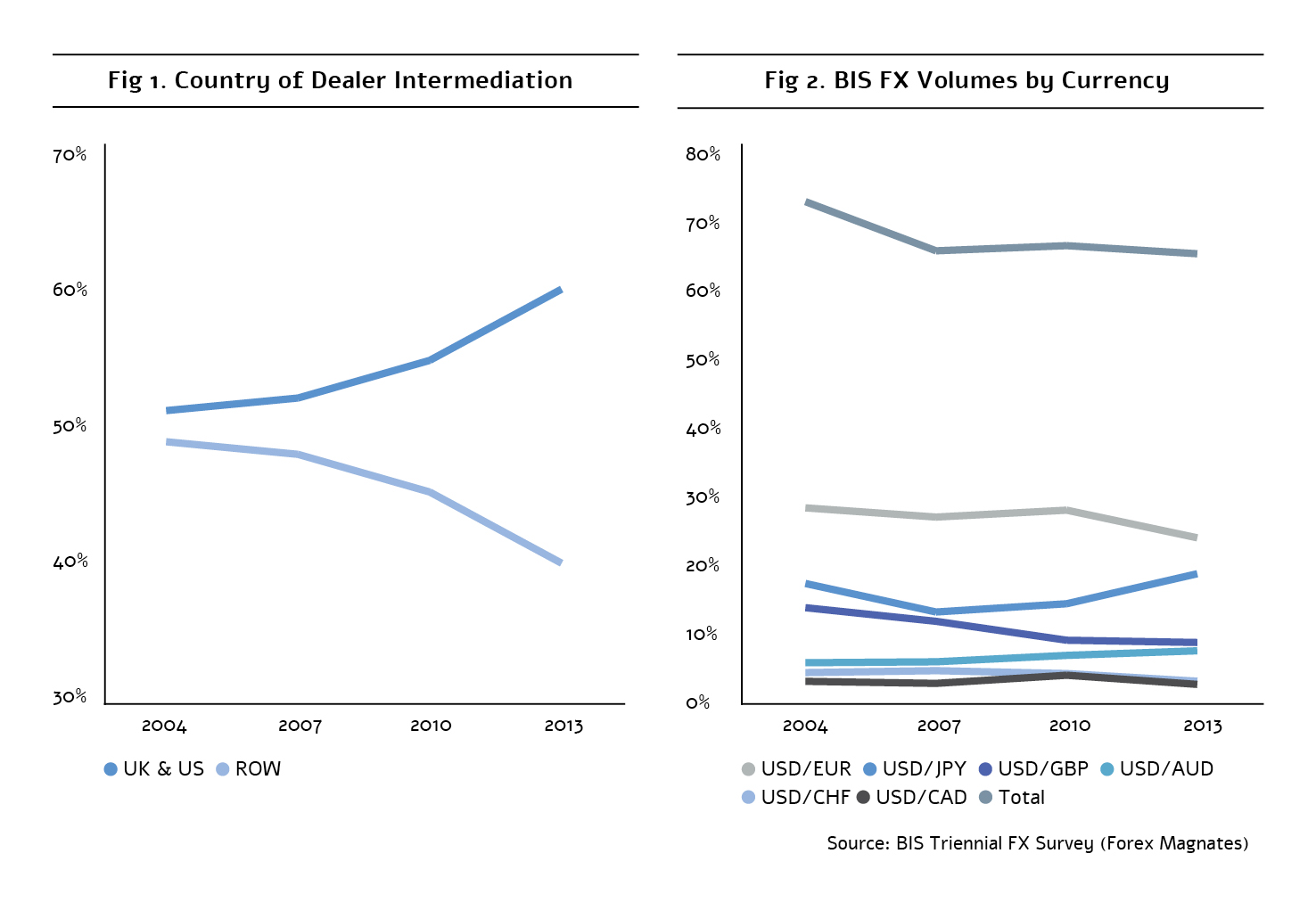

Interestingly though, as the FX market has become increasingly fragmented, as witnessed by the increased importance of non-dealers, the UK and US’s hold on the market has increased. Between 2010 to 2013, combined UK and US volumes rose from 54.7% to 59.8% (Figure 1–data is based on jurisdiction that was used to intermediate a dealer's trade). This occurred even as market share of major currencies has been trending lower (Figure 2). The numbers demonstrate that despite the increase of global FX demand, international firms are favoring to work with established centers when deciding where to source or send their liquidity.

Factoring into this trend has been the ease of access to connect with the major FX centers, as well as tight pricing. As a result, it has become easier and cheaper than ever for institutional investors and regional banks to source liquidity of major currencies for the proprietary trading and customer needs.

Benefiting from the demand of global firms to partner with UK and US dealers as their counterparties, telecom networking firms have been quickly rolling out cross-boundary low latency services. Among solutions, one of the main services is the installment of private point to point networks between financial centers. In this setup, telecom firms create local access points where foreign traders can connect to high-speed networks. For example, through a private network between Stockholm and London, Swedish traders can reduce latency by connecting directly to local access points, instead of relying on public networks to send their data to and from the United Kingdom.

Asian Opportunities

Harpal Sandhu, CEO, Integral Development Corp

While these networks do provide an opportunity to access the liquid UK and US markets, they are still a substitute to localized pricing. As such, foreign firms do suffer from increased slippage costs and higher latency than local traders. In this regard, Bondesen believes there is an opportunity for the creation of localized hubs of primary liquidity. Specifically, he mentioned that the build-up of local Asian FX liquidity centers is an important trend taking place in the industry.

As a result, dealers and ECNs that are able to create trading venues where pricing is independent of UK and US financial centers, will be well situated to leverage their regional location when marketing their liquidity. In this regard, Singapore has currently taken the lead among Asian countries as a regional center of sourcing liquidity. In the latest BIS report, Singapore led Asian countries in terms of FX intermediation with $383 billion in daily volumes. This compared to $374 billion in Japan and $275 billion of daily FX trading in Hong Kong.

An Aggregators' World

Rising along with the overall FX industry volumes and specifically the activity among non-dealers are aggregators. These are the firms that provide the technology to combine multiple liquidity sources into one tradable feed. In addition, providers are creating risk management solutions that allow users to create their pricing to clients, and become forex market makers to their customers. Services include products to dynamically adjust spreads, as well as decide which customer order flow to hedge externally or warehouse internally. Due to the increase use of these services, smaller financial institutions are effectively able to become dealers and provide eFX services. In addition, rather than needing to tap into public trading venues, using aggregator technology, buy-side traders are creating their own ECNs as they combine multiple pricing relationships into one tradable feed.

Speaking about this trend in the FX industry earlier this year, EBS CEO, Gil Mandelzis, referred to the future as the ‘Decade of the Aggregator’ and believed it was one of the main growth areas in the industry. Not surprisingly, this potential has spawned the creation of many new firms entering the aggregation market. As a result, this has led to the question of whether the market has become too saturated with third party aggregators.

James Sinclair, CEO, MarketFactory

Providing an opinion, Sinclair explained that the diversity of the market and multitude of needs are allowing many firms to operate in the space as he stated, “Far from becoming a crowded space, this is becoming a space where different firms serve different segments and offer different value propositions. Aggregator is too broad a term. Some aggregators are allied, paid by or even owned by banks; others are more akin to an ECN.”

A $6 trillion-a-day market?

As mentioned above, one of the corollaries of the increase of smaller firms implementing eFX solutions is the ability for them to become dealers to their clients. The result is that much of the ‘other financial institution’ segment volume flow isn’t reaching primary dealers and being reported within the BIS’s statistics. Analyzing the retail market in October, Forex Magnates estimated that the volumes were at least double the $78 billion- a-day reported by the BIS, based on brokers handling flow internally. Similarly, of the $2.8 trillion from non-dealers reported by the BIS, it doesn’t include non-hedged trades that never get factored within primary dealer books. However, unlike retail firms where warehoused liquidity comprises over 50% of order flow, market-making among regional banks is estimated to be between 20-40%.

To calculate the entire market though requires an understanding of just how much of the reported $2.8 trillion is sell side driven. Based on the BIS figures, of the $2.8 trillion, $1.183 trillion of the volumes were composed of FX Spot trading. Using the spot figure as the foundation for deriving sell-side market making volumes and attributing that 30% of originates from non-banks, we can estimate that an additional 14%-28% from the $1.183 trillion is being traded. Applying the mid-point 21% ratio calculates to around $250 billion in non-reported volumes. When adding an approximate (low estimate) of $80 billion a day in non-reported retail volumes, the combined FX market sums up to $5.63 trillion in daily volume taking place in April 2013.

Admittedly, these calculations are rough estimates. Additionally, they are based on April 2013 trading results, with the market since subsiding somewhat. Nonetheless, taking into account the growth of non-dealer participants, both in the retail market as well as regional banks, does point to a rising portion of unreported volumes. Therefore, while we may not be at the point where $6 trillion a day in volume is consistently taking place, thanks to the diversity of growth engines in the FX industry, we aren’t too far away from eclipsing another trillion dollar barrier.

Sifting through the Bank of International Settlements (BIS) Triennial FX Survey, arguably the most important trend taking place is the growth of non-dealer bank participation. Within the report, the survey polls participant dealers in regards to trading details such as volumes by currency, counterparty type and region.

Topping the list of counterparties was the ‘other financial institution’ segment. Responsible for $2.8 trillion, or 53% of the survey’s $5.3 trillion a day total for global FX volumes, the segment includes smaller banks that do not act as dealers in the FX market, proprietary traders within investment banks, and institutional investors such as pension, hedge and mutual funds. Volumes in this group rose 48% from $1.9 trillion in 2010, to the most recent $2.8 trillion. During the 2010 survey the other financial institutions overtook reporting dealers, with market share continuing to climb over the last three years.

There are several factors that have led to the rising volumes of the non-dealer. Perhaps the main cause has been advances of electronic trading which has provided easier opportunities for Tier 2/3 banks to offer eFX solutions to their clients. Also, a factor is the dwindling profit margins posted on FX volumes, leading major banks to focus their marketing efforts to reach less competitive countries that provide the opportunity to achieve higher revenues per million dollars traded. As a result, banks in countries such as Poland, Turkey, as well as South-East Asian nations have become recent entrants to the eFX world.

On a more macro-level, globalization as a whole can’t be underestimated. As long as cross-boundary trade increases, so does demand among firms for foreign exchange services. This demand represents itself through the increased needs of businesses for FX solutions from regional banks. In addition, larger regional banks are able to leverage their expertise to price their local currency more aggressively to foreigners.

Explaining how technology has evolved the industry, Peter A. Bondesen, Sales Manager EMEA at FlexTrade stated to Forex Magnates that, “Improvements in technology that is available to firms is an important factor. For smaller banks, technology was a stumbling block to enter the FX market.” As a result, Bondesen added that new entrants aren’t only aggregating liquidity to resell it to their customers, but are using their “regional expertise in the local currency” to provide pricing to the rest of the world. Specifically, Bondesen noted that through implementation of eFX solutions, Scandinavian regional banks have succeeded to become the main markets in their respective currencies by connecting their liquidity to major financial centers and trading venues.

Due to the economic efficiencies available in technology, smaller firms are also able to source customized solutions to better fit both their buy and sell-side needs. Explaining this, Harpal Sandhu, CEO, Integral Development Corp added to Forex Magnates that, “Our experience is in line with what the BIS report states, which is that “smaller banks” and “institutional investors” are growth areas.” He added that, “We have seen a dramatic customer growth in these areas because these market participants require an OTC platform that offers the flexibility so they can do whatever they want with it, for their own benefits or those of their customers.”

As a result, it is becoming a ‘two-way street’ where banks are able to grow their FX businesses by sourcing global pricing for their local customers, as well as becoming liquidity providers of their local currency to the rest of the world. Meeting this dual demand, Illit Geller, CEO of Tradair explained that there are “Two solutions categories; the ECN - where liquidity of the ECN can be rebranded by the regional bank for its customers, and liquidity optimization management (LOM) which provide a tier1 bank type solution for regional banks pricing and distribution."

Illit Geller, CEO of TradAir

In terms of technology, this had led to the creation of different types of products to fit the primary needs of banks. Geller explained that in regards to regional banks that are using their expertise to provide pricing of their local currency to the rest of the world, firms require greater customization and risk controls as she stated, “It is not enough to provide similar technology solutions to those of the 1st tier banks, regional banks require tight trader controls, different algorithms and workflow management suited for their unique currency needs.”

Similarly, firms seeking cost-efficient solutions to offer eFX services to clients are also witnessing an ever expanding product line to choose from, as providers like Integral have been offering solutions that require little to no upfront costs to launch. Having established client bases, these solutions allow regional banks to both resell prime dealer liquidity to their clients as well as price their own market-making initiatives. Although much of the initial business that regional banks are receiving is based on upselling services to existing clients, firms are also using the FX services to gain new customers. Over the long run, Bondesen believes that banks with the “Most efficient setups will be able to show this to customers to win clients. More than just reselling, they will be able to win new clients with great services.”

Fragmented but still centralized

Interestingly though, as the FX market has become increasingly fragmented, as witnessed by the increased importance of non-dealers, the UK and US’s hold on the market has increased. Between 2010 to 2013, combined UK and US volumes rose from 54.7% to 59.8% (Figure 1–data is based on jurisdiction that was used to intermediate a dealer's trade). This occurred even as market share of major currencies has been trending lower (Figure 2). The numbers demonstrate that despite the increase of global FX demand, international firms are favoring to work with established centers when deciding where to source or send their liquidity.

Factoring into this trend has been the ease of access to connect with the major FX centers, as well as tight pricing. As a result, it has become easier and cheaper than ever for institutional investors and regional banks to source liquidity of major currencies for the proprietary trading and customer needs.

Benefiting from the demand of global firms to partner with UK and US dealers as their counterparties, telecom networking firms have been quickly rolling out cross-boundary low latency services. Among solutions, one of the main services is the installment of private point to point networks between financial centers. In this setup, telecom firms create local access points where foreign traders can connect to high-speed networks. For example, through a private network between Stockholm and London, Swedish traders can reduce latency by connecting directly to local access points, instead of relying on public networks to send their data to and from the United Kingdom.

Asian Opportunities

Harpal Sandhu, CEO, Integral Development Corp

While these networks do provide an opportunity to access the liquid UK and US markets, they are still a substitute to localized pricing. As such, foreign firms do suffer from increased slippage costs and higher latency than local traders. In this regard, Bondesen believes there is an opportunity for the creation of localized hubs of primary liquidity. Specifically, he mentioned that the build-up of local Asian FX liquidity centers is an important trend taking place in the industry.

As a result, dealers and ECNs that are able to create trading venues where pricing is independent of UK and US financial centers, will be well situated to leverage their regional location when marketing their liquidity. In this regard, Singapore has currently taken the lead among Asian countries as a regional center of sourcing liquidity. In the latest BIS report, Singapore led Asian countries in terms of FX intermediation with $383 billion in daily volumes. This compared to $374 billion in Japan and $275 billion of daily FX trading in Hong Kong.

An Aggregators' World

Rising along with the overall FX industry volumes and specifically the activity among non-dealers are aggregators. These are the firms that provide the technology to combine multiple liquidity sources into one tradable feed. In addition, providers are creating risk management solutions that allow users to create their pricing to clients, and become forex market makers to their customers. Services include products to dynamically adjust spreads, as well as decide which customer order flow to hedge externally or warehouse internally. Due to the increase use of these services, smaller financial institutions are effectively able to become dealers and provide eFX services. In addition, rather than needing to tap into public trading venues, using aggregator technology, buy-side traders are creating their own ECNs as they combine multiple pricing relationships into one tradable feed.

Speaking about this trend in the FX industry earlier this year, EBS CEO, Gil Mandelzis, referred to the future as the ‘Decade of the Aggregator’ and believed it was one of the main growth areas in the industry. Not surprisingly, this potential has spawned the creation of many new firms entering the aggregation market. As a result, this has led to the question of whether the market has become too saturated with third party aggregators.

James Sinclair, CEO, MarketFactory

Providing an opinion, Sinclair explained that the diversity of the market and multitude of needs are allowing many firms to operate in the space as he stated, “Far from becoming a crowded space, this is becoming a space where different firms serve different segments and offer different value propositions. Aggregator is too broad a term. Some aggregators are allied, paid by or even owned by banks; others are more akin to an ECN.”

A $6 trillion-a-day market?

As mentioned above, one of the corollaries of the increase of smaller firms implementing eFX solutions is the ability for them to become dealers to their clients. The result is that much of the ‘other financial institution’ segment volume flow isn’t reaching primary dealers and being reported within the BIS’s statistics. Analyzing the retail market in October, Forex Magnates estimated that the volumes were at least double the $78 billion- a-day reported by the BIS, based on brokers handling flow internally. Similarly, of the $2.8 trillion from non-dealers reported by the BIS, it doesn’t include non-hedged trades that never get factored within primary dealer books. However, unlike retail firms where warehoused liquidity comprises over 50% of order flow, market-making among regional banks is estimated to be between 20-40%.

To calculate the entire market though requires an understanding of just how much of the reported $2.8 trillion is sell side driven. Based on the BIS figures, of the $2.8 trillion, $1.183 trillion of the volumes were composed of FX Spot trading. Using the spot figure as the foundation for deriving sell-side market making volumes and attributing that 30% of originates from non-banks, we can estimate that an additional 14%-28% from the $1.183 trillion is being traded. Applying the mid-point 21% ratio calculates to around $250 billion in non-reported volumes. When adding an approximate (low estimate) of $80 billion a day in non-reported retail volumes, the combined FX market sums up to $5.63 trillion in daily volume taking place in April 2013.

Admittedly, these calculations are rough estimates. Additionally, they are based on April 2013 trading results, with the market since subsiding somewhat. Nonetheless, taking into account the growth of non-dealer participants, both in the retail market as well as regional banks, does point to a rising portion of unreported volumes. Therefore, while we may not be at the point where $6 trillion a day in volume is consistently taking place, thanks to the diversity of growth engines in the FX industry, we aren’t too far away from eclipsing another trillion dollar barrier.

Institutional FX Volumes Surge 25% in January 2026 as Dollar Volatility Returns

Featured Videos

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights