Last week, the financial markets were focused on the August Nonfarm Payrolls (NFP) report. The data, released on Friday, September 6, showed a modest increase of 142,000 jobs, following downward revisions to the previous two months. While the unemployment rate dipped to 4.2%, the NFP report sent ripples through the markets.

The NFP release came as market participants were eagerly anticipating the Federal Reserve's next move on interest rates. With the Fed on hold since July 2023, markets had been pricing in a 100% probability of a rate cut at the upcoming September 17-18 meeting.

However, the NFP data introduced uncertainty about the magnitude of that cut. Prior to the report, a 25 basis point cut was favoured, but the mixed signals could sway the Fed towards a more aggressive 50 basis point reduction.

The EUR/USD exchange rate experienced a volatile week before ending slightly up (+0.32%), after declining by 1.29% the week before. Let’s take a closer look at what could affect the EUR/USD exchange rate this week.

US Consumer Price Index (CPI)

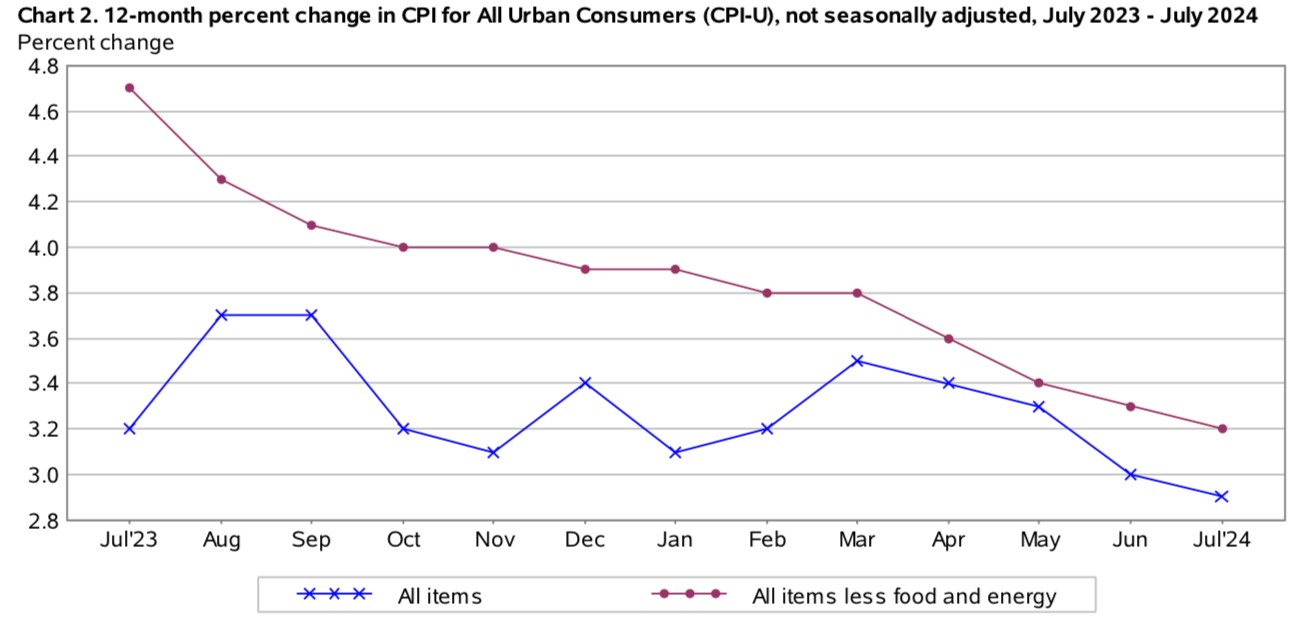

The United States saw a continued decline in inflation rates during July 2024, marking a positive trend. The annual inflation rate, as measured by the Consumer Price Index (CPI), dropped to 2.9% in July, the lowest level since March 2021. This deceleration represents a significant step towards the Federal Reserve's target of 2% annual inflation.

Turning to core inflation, inflation not taking into account volatile food and energy prices, figures also showed that inflationary pressures are gradually easing. Core inflation rate fell to the lowest reading in over three years in July to 3.2%.

Looking ahead, economists anticipate further progress in taming inflation when the CPI data for last month is published on Wednesday, August 11, at 12:30 PM GMT. Projections for August 2024 suggest that the annual inflation rate could drop to 2.6%, and core inflation could remain at 3.2%.

US Producer Price Index (PPI)

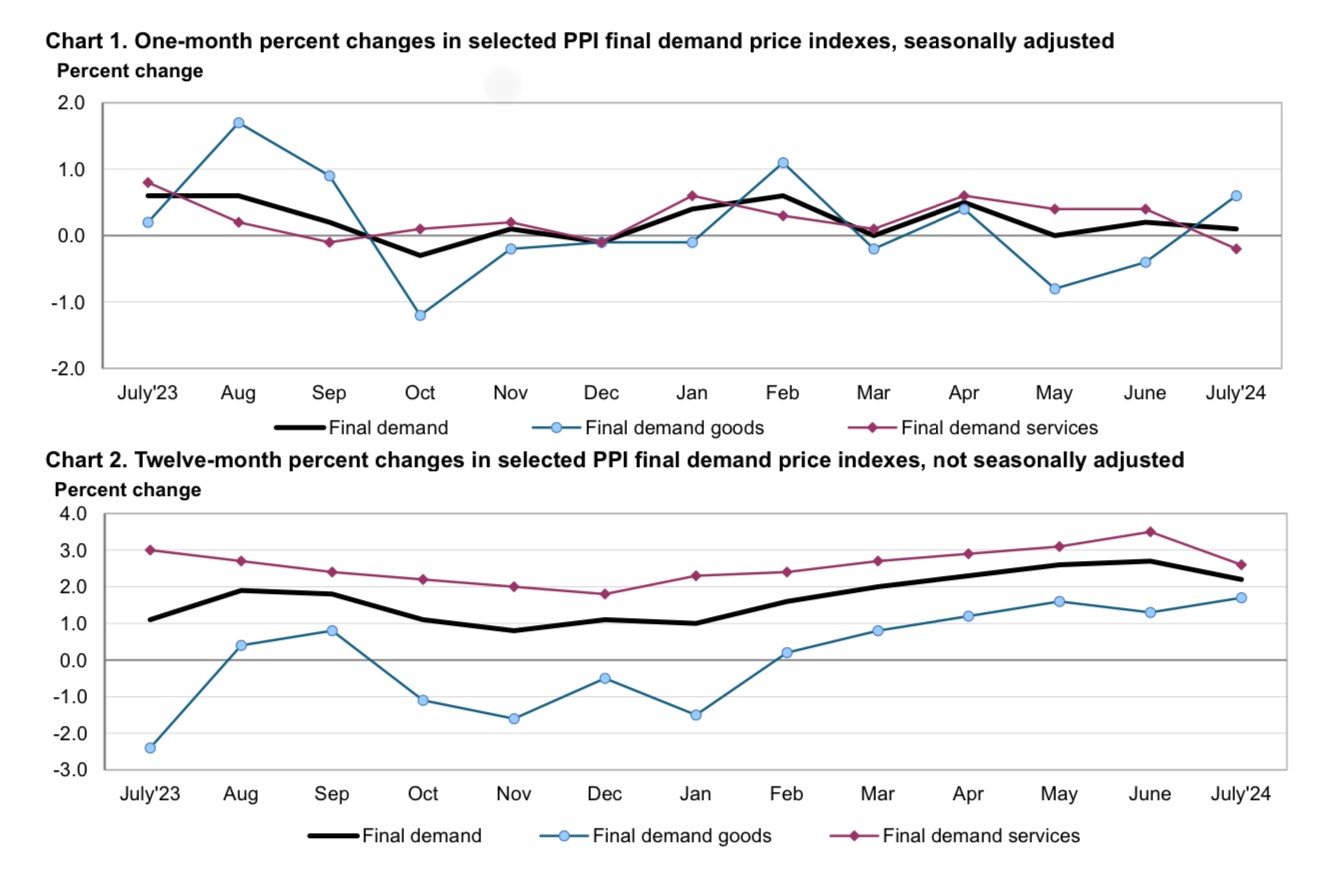

The U.S. Producer Price Index (PPI) for final demand, a key indicator of inflation pressures of goods sold to manufacturers, rose by a less-than-expected 0.1% in July.

This marks a slowdown from the previous month's 0.2% increase and is the smallest monthly rise since February 2023. The moderation in PPI suggests that businesses are facing diminishing pricing power, indicating that inflationary pressures are easing.

The decline in PPI is primarily driven by a significant decrease in service prices, which fell by the most in nearly 1-1.5 years. This suggests that businesses are finding it more difficult to pass on higher costs to consumers in the service area. The price of services usually accounted for the increase of this inflation indicator.

Looking ahead, market participants expect either monthly PPI inflation to remain at 0.1% or increase to 0.2% for last month will be published on Thursday, August 12, at 12:30 PM GMT.

European Central Bank (ECB) Monetary Policy Meeting

Recent data from Eurostat, the statistical office of the European Union, shows that annual inflation in the euro area is expected to be 2.2% in August 2024, down from 2.6% in July.

This decrease suggests that the European Central Bank’s (ECB) efforts to curb inflation are beginning to show results, giving the institution more confidence in its forecasts of gradual disinflation.

However, the ECB faces a delicate balancing act: while the downward trend in inflation is promising, there remains a significant risk that easing monetary policy too quickly could reignite inflationary pressures, potentially raising inflation expectations once again.

Meanwhile, the broader economic recovery in the Eurozone appears to be losing momentum. In the second quarter of 2024, seasonally adjusted GDP in both the euro area and the EU grew by only 0.2% compared to the previous quarter, according to Eurostat. This marks a slowdown from the 0.3% growth recorded in the first quarter of 2024.

Year-on-year, GDP increased by 0.6% in the euro area and by 0.8% in the EU during the second quarter, slightly up from the 0.5% and 0.7% growth rates, respectively, seen in the first quarter.

In comparison, the United States experienced more robust economic performance during the same period. U.S. GDP grew by 0.7% in the second quarter of 2024, up from 0.4% in the first quarter. Year-on-year, the U.S. economy expanded by 3.1% in the second quarter, an increase from the 2.9% growth observed in the first quarter.

The Eurozone's economic landscape is highly dynamic, with conditions that can shift rapidly due to unforeseen events, potentially affecting both inflation and growth. In response to these evolving circumstances, the European Central Bank remains vigilant, consistently monitoring economic indicators. The ECB is poised to adjust its monetary policy as needed to maintain inflation on a sustainable and controlled trajectory, responding to the latest data.

Traders are now anticipating an interest rate cut from the ECB in its upcoming meeting next week on Thursday, September 12. The focus will be on any signals from the central bank that could suggest another rate reduction in October. The ECB began lowering rates from their record high of 4% in June, but refrained from a second cut in July, citing concerns over services inflation, which remained above 4%. However, traders now seem to fully expect a cut to 3.5% at Thursday's meeting when the decision will be released at 12:15 PM GMT.

Attention will be directed towards the ECB's announcement and the subsequent press conference, where policymakers' perspectives on the longer-term inflation outlook will be crucial. Currently, market participants are evenly divided on whether the ECB will proceed with a third rate cut this year, potentially in October.

EUR/USD Technical Outlook

The EUR/USD exchange rate experienced a sharp rally, appreciating by 4.78% during the period from August 24 to August 30, and reaching its highest level since early July 2024. This surge pushed the EUR/USD above the upper band of the Bollinger Band indicator, a technical analysis tool that measures volatility. In the final week of August, the EUR/USD reversed course, declining by 1.29%. This pullback brought the pair back below the overbought territory indicated by the Relative Strength Index (RSI). Still, the EUR/USD closed last week with a slight gain of 0.32%.

The information provided does not constitute investment research. The material has not been prepared in accordance with the legal requirements designed to promote the independence of investment research and as such is to be considered to be a marketing communication.

All information has been prepared by ActivTrades (“AT”). The information does not contain a record of AT’s prices, or an offer of or solicitation for a transaction in any financial instrument. No representation or warranty is given as to the accuracy or completeness of this information.

Any material provided does not have regard to the specific investment objective and financial situation of any person who may receive it. Past performance is not a reliable indicator of future performance. AT provides an execution-only service. Consequently, any person acting on the information provided does so at their own risk.