Let’s take a closer look at what could affect the EUR/USD exchange rate this week.

Last week, the financial markets were focused on

the August Nonfarm Payrolls (NFP) report. The data, released on Friday,

September 6, showed a modest increase of 142,000 jobs, following downward

revisions to the previous two months. While the unemployment rate dipped to

4.2%, the NFP report sent ripples through the markets.

The NFP release came as market participants were

eagerly anticipating the Federal Reserve's next move on interest rates. With

the Fed on hold since July 2023, markets had been pricing in a 100% probability

of a rate cut at the upcoming September 17-18 meeting.

However, the NFP data introduced uncertainty

about the magnitude of that cut. Prior to the report, a 25 basis point cut was

favoured, but the mixed signals could sway the Fed towards a more aggressive 50

basis point reduction.

The EUR/USD exchange rate experienced a volatile

week before ending slightly up (+0.32%), after declining by 1.29% the week

before. Let’s take a closer look at what could affect the EUR/USD exchange rate

this week.

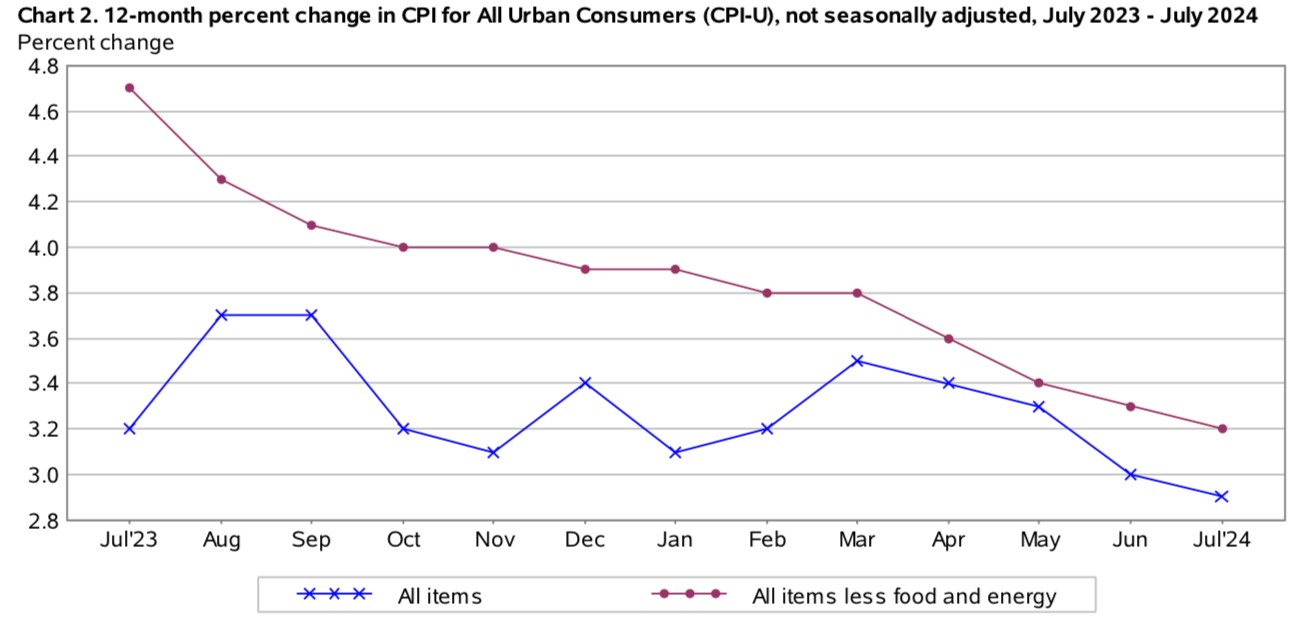

US Consumer Price Index (CPI)

The United States saw a continued decline in

inflation rates during July 2024, marking a positive trend. The annual

inflation rate, as measured by the Consumer Price Index (CPI), dropped to 2.9%

in July, the lowest level since March 2021. This deceleration represents a

significant step towards the Federal Reserve's target of 2% annual inflation.

Turning to core inflation, inflation not taking

into account volatile food and energy prices, figures also showed that

inflationary pressures are gradually easing. Core inflation rate fell to the

lowest reading in over three years in July to 3.2%.

Looking ahead, economists anticipate further

progress in taming inflation when the CPI data for last month is published on

Wednesday, August 11, at 12:30 PM GMT. Projections for August 2024 suggest that

the annual inflation rate could drop to 2.6%, and core inflation could remain

at 3.2%.

Source: Bureau of Labor Statistics

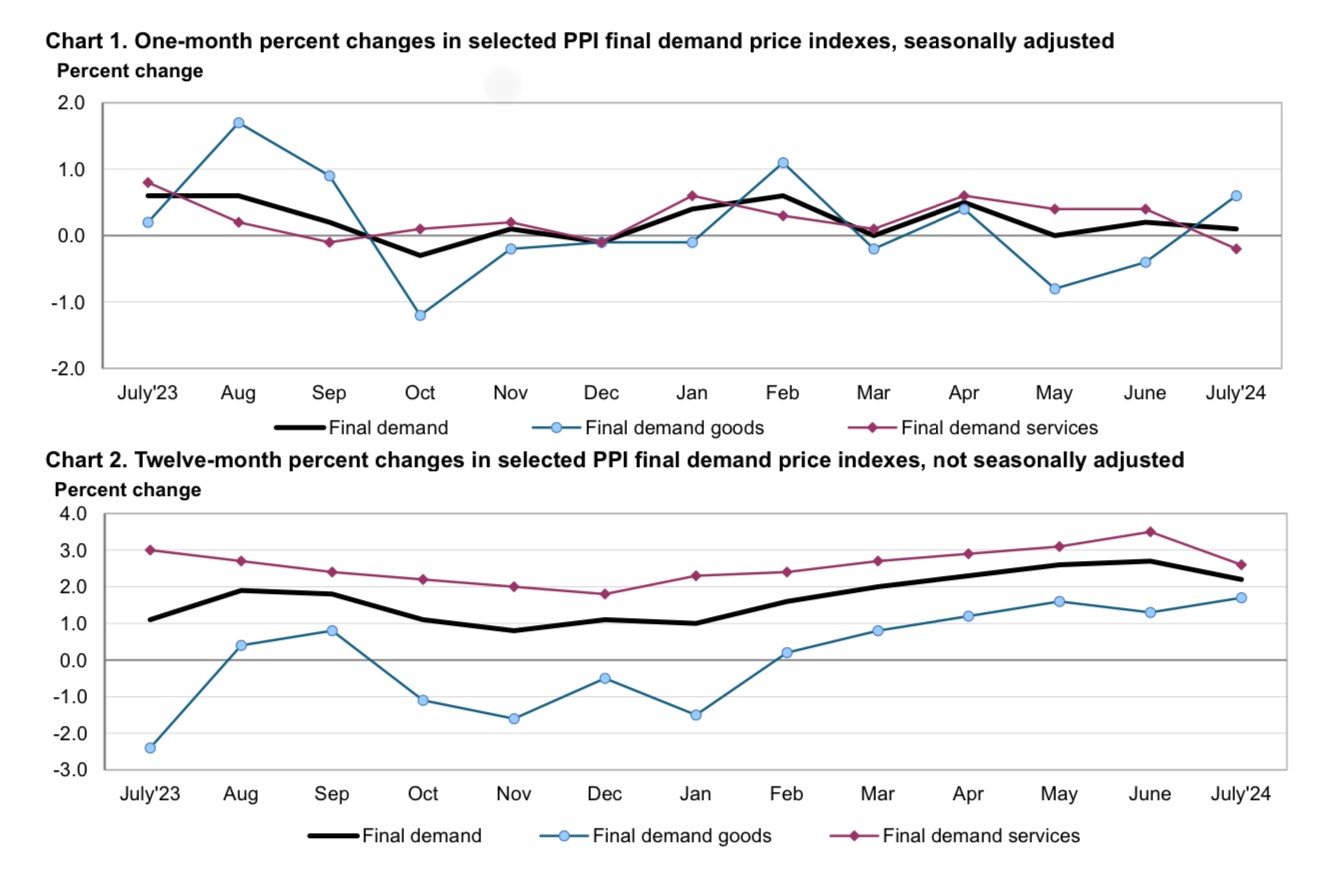

US Producer Price Index (PPI)

The U.S. Producer Price Index (PPI) for final

demand, a key indicator of inflation pressures of goods sold to manufacturers,

rose by a less-than-expected 0.1% in July.

This marks a slowdown from the previous month's

0.2% increase and is the smallest monthly rise since February 2023. The

moderation in PPI suggests that businesses are facing diminishing pricing

power, indicating that inflationary pressures are easing.

The decline in PPI is primarily driven by a

significant decrease in service prices, which fell by the most in nearly 1-1.5

years. This suggests that businesses are finding it more difficult to pass on

higher costs to consumers in the service area. The price of services usually

accounted for the increase of this inflation indicator.

Looking ahead, market participants expect either

monthly PPI inflation to remain at 0.1% or increase to 0.2% for last month will

be published on Thursday, August 12, at 12:30 PM GMT.

Source: Bureau of Labor Statistics

European Central Bank (ECB) Monetary Policy Meeting

Recent data from Eurostat, the statistical

office of the European Union, shows that annual inflation in the euro area is

expected to be 2.2% in August 2024, down from 2.6% in July.

This decrease suggests that the European Central

Bank’s (ECB) efforts to curb inflation are beginning to show results, giving

the institution more confidence in its forecasts of gradual disinflation.

However, the ECB faces a delicate balancing act:

while the downward trend in inflation is promising, there remains a significant

risk that easing monetary policy too quickly could reignite inflationary

pressures, potentially raising inflation expectations once again.

Meanwhile, the broader economic recovery in the

Eurozone appears to be losing momentum. In the second quarter of 2024,

seasonally adjusted GDP in both the euro area and the EU grew by only 0.2%

compared to the previous quarter, according to Eurostat. This marks a slowdown

from the 0.3% growth recorded in the first quarter of 2024.

Year-on-year, GDP increased by 0.6% in the euro

area and by 0.8% in the EU during the second quarter, slightly up from the 0.5%

and 0.7% growth rates, respectively, seen in the first quarter.

In comparison, the United States experienced

more robust economic performance during the same period. U.S. GDP grew by 0.7%

in the second quarter of 2024, up from 0.4% in the first quarter. Year-on-year,

the U.S. economy expanded by 3.1% in the second quarter, an increase from the

2.9% growth observed in the first quarter.

The Eurozone's economic landscape is highly

dynamic, with conditions that can shift rapidly due to unforeseen events,

potentially affecting both inflation and growth. In response to these evolving

circumstances, the European Central Bank remains vigilant, consistently

monitoring economic indicators. The ECB is poised to adjust its monetary policy

as needed to maintain inflation on a sustainable and controlled trajectory,

responding to the latest data.

Traders are now anticipating an interest rate

cut from the ECB in its upcoming meeting next week on Thursday, September 12.

The focus will be on any signals from the central bank that could suggest

another rate reduction in October. The ECB began lowering rates from their

record high of 4% in June, but refrained from a second cut in July, citing

concerns over services inflation, which remained above 4%. However, traders now

seem to fully expect a cut to 3.5% at Thursday's meeting when the decision will

be released at 12:15 PM GMT.

Attention will be directed towards the ECB's

announcement and the subsequent press conference, where policymakers'

perspectives on the longer-term inflation outlook will be crucial. Currently,

market participants are evenly divided on whether the ECB will proceed with a

third rate cut this year, potentially in October.

EUR/USD Technical Outlook

The EUR/USD exchange rate experienced a sharp

rally, appreciating by 4.78% during the period from August 24 to August 30, and

reaching its highest level since early July 2024. This surge pushed the EUR/USD

above the upper band of the Bollinger Band indicator, a technical analysis tool

that measures volatility. In the final week of August, the EUR/USD reversed

course, declining by 1.29%. This pullback brought the pair back below the

overbought territory indicated by the Relative Strength Index (RSI). Still, the

EUR/USD closed last week with a slight gain of 0.32%.

Weekly EUR/USD Chart - Source: ActivTrader

The information

provided does not constitute investment research. The material has not been prepared

in accordance with the legal requirements designed to promote the independence

of investment research and as such is to be considered to be a marketing

communication.

All information

has been prepared by ActivTrades (“AT”). The information does not contain a

record of AT’s prices, or an offer of or solicitation for a transaction in any

financial instrument. No representation or warranty is given as to the accuracy

or completeness of this information.

Any material

provided does not have regard to the specific investment objective and

financial situation of any person who may receive it. Past performance is not a

reliable indicator of future performance. AT provides an execution-only

service. Consequently, any person acting on the information provided does so at

their own risk.

Last week, the financial markets were focused on

the August Nonfarm Payrolls (NFP) report. The data, released on Friday,

September 6, showed a modest increase of 142,000 jobs, following downward

revisions to the previous two months. While the unemployment rate dipped to

4.2%, the NFP report sent ripples through the markets.

The NFP release came as market participants were

eagerly anticipating the Federal Reserve's next move on interest rates. With

the Fed on hold since July 2023, markets had been pricing in a 100% probability

of a rate cut at the upcoming September 17-18 meeting.

However, the NFP data introduced uncertainty

about the magnitude of that cut. Prior to the report, a 25 basis point cut was

favoured, but the mixed signals could sway the Fed towards a more aggressive 50

basis point reduction.

The EUR/USD exchange rate experienced a volatile

week before ending slightly up (+0.32%), after declining by 1.29% the week

before. Let’s take a closer look at what could affect the EUR/USD exchange rate

this week.

US Consumer Price Index (CPI)

The United States saw a continued decline in

inflation rates during July 2024, marking a positive trend. The annual

inflation rate, as measured by the Consumer Price Index (CPI), dropped to 2.9%

in July, the lowest level since March 2021. This deceleration represents a

significant step towards the Federal Reserve's target of 2% annual inflation.

Turning to core inflation, inflation not taking

into account volatile food and energy prices, figures also showed that

inflationary pressures are gradually easing. Core inflation rate fell to the

lowest reading in over three years in July to 3.2%.

Looking ahead, economists anticipate further

progress in taming inflation when the CPI data for last month is published on

Wednesday, August 11, at 12:30 PM GMT. Projections for August 2024 suggest that

the annual inflation rate could drop to 2.6%, and core inflation could remain

at 3.2%.

Source: Bureau of Labor Statistics

US Producer Price Index (PPI)

The U.S. Producer Price Index (PPI) for final

demand, a key indicator of inflation pressures of goods sold to manufacturers,

rose by a less-than-expected 0.1% in July.

This marks a slowdown from the previous month's

0.2% increase and is the smallest monthly rise since February 2023. The

moderation in PPI suggests that businesses are facing diminishing pricing

power, indicating that inflationary pressures are easing.

The decline in PPI is primarily driven by a

significant decrease in service prices, which fell by the most in nearly 1-1.5

years. This suggests that businesses are finding it more difficult to pass on

higher costs to consumers in the service area. The price of services usually

accounted for the increase of this inflation indicator.

Looking ahead, market participants expect either

monthly PPI inflation to remain at 0.1% or increase to 0.2% for last month will

be published on Thursday, August 12, at 12:30 PM GMT.

Source: Bureau of Labor Statistics

European Central Bank (ECB) Monetary Policy Meeting

Recent data from Eurostat, the statistical

office of the European Union, shows that annual inflation in the euro area is

expected to be 2.2% in August 2024, down from 2.6% in July.

This decrease suggests that the European Central

Bank’s (ECB) efforts to curb inflation are beginning to show results, giving

the institution more confidence in its forecasts of gradual disinflation.

However, the ECB faces a delicate balancing act:

while the downward trend in inflation is promising, there remains a significant

risk that easing monetary policy too quickly could reignite inflationary

pressures, potentially raising inflation expectations once again.

Meanwhile, the broader economic recovery in the

Eurozone appears to be losing momentum. In the second quarter of 2024,

seasonally adjusted GDP in both the euro area and the EU grew by only 0.2%

compared to the previous quarter, according to Eurostat. This marks a slowdown

from the 0.3% growth recorded in the first quarter of 2024.

Year-on-year, GDP increased by 0.6% in the euro

area and by 0.8% in the EU during the second quarter, slightly up from the 0.5%

and 0.7% growth rates, respectively, seen in the first quarter.

In comparison, the United States experienced

more robust economic performance during the same period. U.S. GDP grew by 0.7%

in the second quarter of 2024, up from 0.4% in the first quarter. Year-on-year,

the U.S. economy expanded by 3.1% in the second quarter, an increase from the

2.9% growth observed in the first quarter.

The Eurozone's economic landscape is highly

dynamic, with conditions that can shift rapidly due to unforeseen events,

potentially affecting both inflation and growth. In response to these evolving

circumstances, the European Central Bank remains vigilant, consistently

monitoring economic indicators. The ECB is poised to adjust its monetary policy

as needed to maintain inflation on a sustainable and controlled trajectory,

responding to the latest data.

Traders are now anticipating an interest rate

cut from the ECB in its upcoming meeting next week on Thursday, September 12.

The focus will be on any signals from the central bank that could suggest

another rate reduction in October. The ECB began lowering rates from their

record high of 4% in June, but refrained from a second cut in July, citing

concerns over services inflation, which remained above 4%. However, traders now

seem to fully expect a cut to 3.5% at Thursday's meeting when the decision will

be released at 12:15 PM GMT.

Attention will be directed towards the ECB's

announcement and the subsequent press conference, where policymakers'

perspectives on the longer-term inflation outlook will be crucial. Currently,

market participants are evenly divided on whether the ECB will proceed with a

third rate cut this year, potentially in October.

EUR/USD Technical Outlook

The EUR/USD exchange rate experienced a sharp

rally, appreciating by 4.78% during the period from August 24 to August 30, and

reaching its highest level since early July 2024. This surge pushed the EUR/USD

above the upper band of the Bollinger Band indicator, a technical analysis tool

that measures volatility. In the final week of August, the EUR/USD reversed

course, declining by 1.29%. This pullback brought the pair back below the

overbought territory indicated by the Relative Strength Index (RSI). Still, the

EUR/USD closed last week with a slight gain of 0.32%.

Weekly EUR/USD Chart - Source: ActivTrader

The information

provided does not constitute investment research. The material has not been prepared

in accordance with the legal requirements designed to promote the independence

of investment research and as such is to be considered to be a marketing

communication.

All information

has been prepared by ActivTrades (“AT”). The information does not contain a

record of AT’s prices, or an offer of or solicitation for a transaction in any

financial instrument. No representation or warranty is given as to the accuracy

or completeness of this information.

Any material

provided does not have regard to the specific investment objective and

financial situation of any person who may receive it. Past performance is not a

reliable indicator of future performance. AT provides an execution-only

service. Consequently, any person acting on the information provided does so at

their own risk.

Why Execution Quality Has Become the Broker’s Real Product: How Versus Trade Builds for the Next Generation of Traders

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights