Gold Market - A Monthly Digest by the Global Broker Octa

Thursday,12/09/2024|12:16GMTby

FM

It is a gold market overview for August 2024 and an outlook for September 2024.

August

has been a truly historic month for gold (XAU). Despite starting off at an

already elevated level after more than a 5% increase in July, gold prices

continued to move higher for most of August, setting a new all-time high of

$2,531 per ounce (oz) on 20 August.

The

month has been packed with major market-moving events (see the list below),

which have resulted in a rather bumpy ride for traders. Indeed, gold investors

lived through intensifying geopolitical tensions in the Middle East and Eastern

Europe, experienced substantial volatility due to a major stock market rout and

digested increasingly dovish investors' interest rate expectations. As many

times before, gold has once again proved its underlying value as a safe-haven

asset and may continue to shine in the months ahead.

Major market-moving events

●

5 August. U.S. recession worries induced by a disappointing nonfarm

payrolls (NFP) report for July shook global markets. U.S. stock indices plunged

to almost two-month lows, while Nikkei 225, Japan's benchmark stock index,

recorded its worst two-day decline ever, dropping by 18.2%, exceeding the

losses incurred during the 1987 Black Monday crash. The gold market saw

substantial volatility as the price of the bullion fluctuated between $2,360

and $2,460 during a single trading session. Although gold managed to recoup

some of the losses later, overall, XAUUSD was down 1.5% that day.

●

8 August. Gold rose by almost 2% due to safe-haven demand and growing

expectations for a sizable interest rate cut from the U.S. Federal Reserve

(Fed) in September. Overall, the market begins to expect more than 100 basis

points (bps) worth of rate cuts by the Fed over the course of just four

meetings.

●

12 August. Gold price rose another 1.7% ahead of the U.S. Consumer Price

Index (CPI) report, while the market continues to price in more than a 50%

chance of a 50-basis point (bps) rate cut by the Federal Reserve (Fed) in

September. In addition, renewed tensions in the Middle East stimulate more

demand for safe-haven assets as traders brace for retaliation by Iran against

Israel over the assassination of a Hamas leader in Tehran.

●

16 August. Gold surges more than 2% to a fresh one-month high as much

lower-than-expected U.S. housing data puts additional pressure on the

greenback, making gold more attractive for holders of other currencies.

●

20 August. The gold price reached a new all-time high as traders continued

to bet on imminent interest rate cuts by the Fed while awaiting painful

revisions to U.S. payroll data and Jerome Powell's speech at the Jackson Hole

economic conference.

Despite

temporary setbacks, gold continued to move higher in August, and the price of

yellow metal remained comfortably above its 100-day and 200-day moving

averages. Rising expectations for looser monetary policy in the U.S. and

globally, endless geopolitical tensions and political instability, and solid

structural demand on the part of central banks helped push the bullion's price

to an all-time high. In addition, the technical picture has been positive,

resulting in trend buying by investors.

Physical

demand for bullion has been a key driver behind the rising price of gold in the

financial markets. Just recently, a Hong Kong Census and Statistics Department

(C&SD) report showed that China's net gold imports via Hong Kong in July

rose by about 17% from the previous month. Although the data for August has not

been released yet, it seems reasonable to infer that China's purchases probably

remained elevated given that the People's Bank of China (PBOC), China's central

bank, has granted new gold import quotas to commercial banks in anticipation of

revived demand. This is important because China is the world's largest consumer

of gold, and its buying patterns can influence the global market and affect

prices. In fact, according to the World Gold Council (WGC), PBOC was the

world's largest single buyer of gold in 2023, with net purchases of 7.23

million oz. According to global broker Octa's estimates, global central banks

have added more than 130 tons of gold to their reserves in 2024.

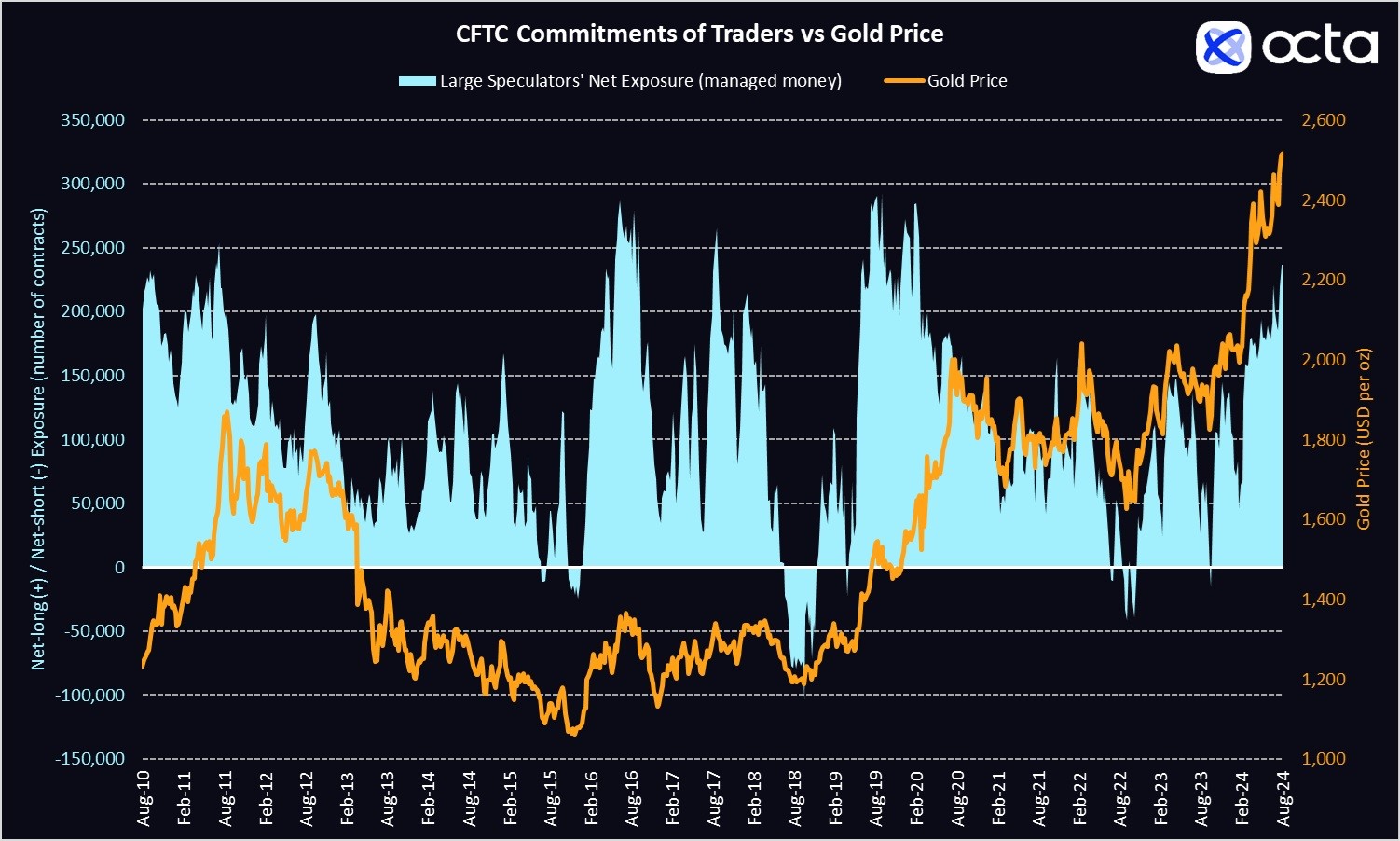

CFTC Commitments of Traders vs Gold

Price

Source: CFTC, LSEG, global broker Octa's calculations

Apart

from central banks, global investors have also remained quite bullish on gold.

According to the Commodity Futures Trading Commission (CFTC), large speculators

(leveraged funds and money managers) increased their net-long exposure in COMEX

gold futures and options by 47,909 contracts in August to 236,818 net-long

contracts. They have maintained their largest net-long exposure in gold in more

than four years. According to LSEG, a financial firm, physically-backed gold

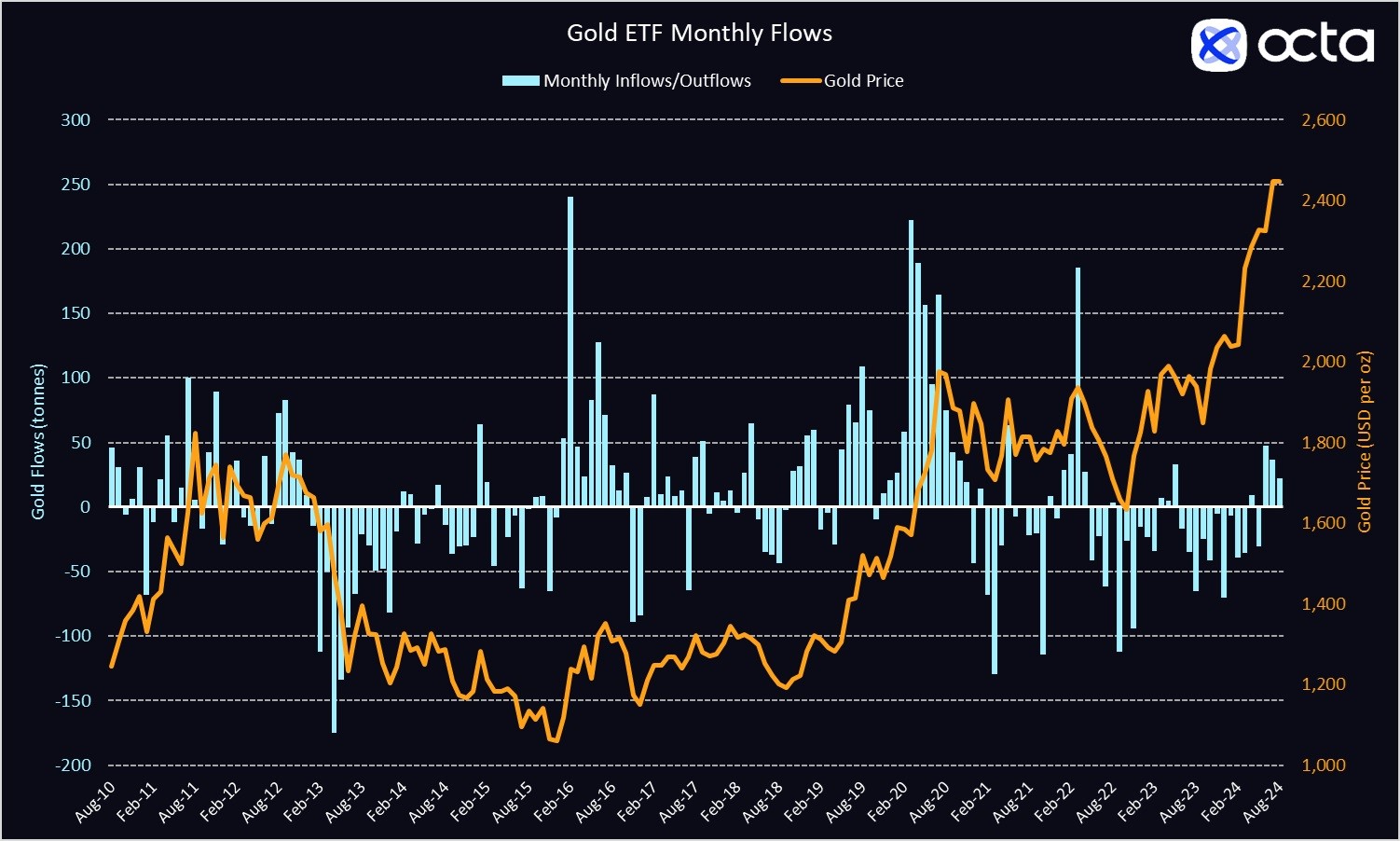

exchange-traded funds (ETFs) witnessed their third consecutive monthly

inflow in August––21.94 tons.

Gold ETF Monthly Flows

Source: LSEG

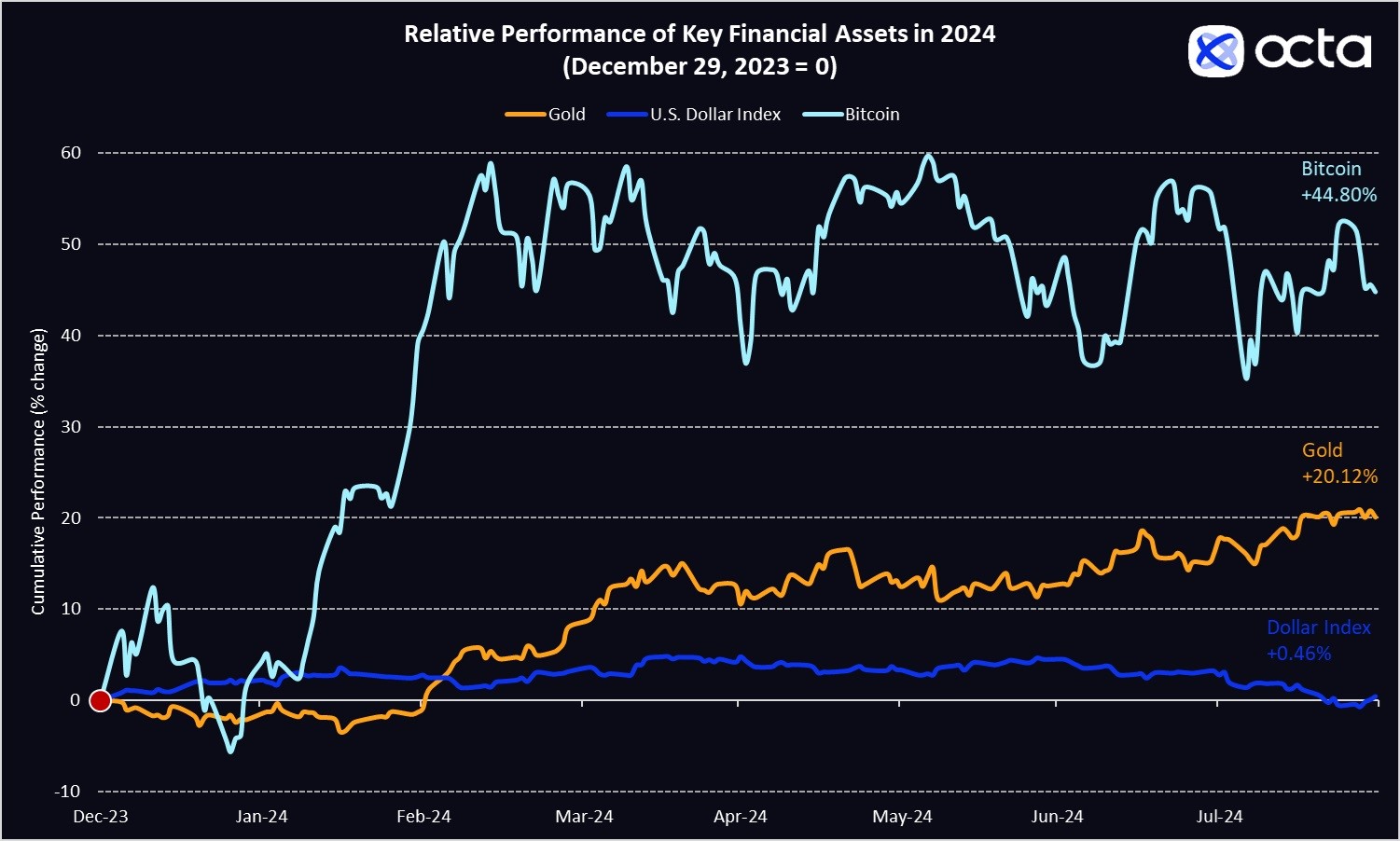

A special

section: gold vs Bitcoin

The

competition between gold and Bitcoin has been a hot topic in the financial

services industry for years. Both assets have their own unique appeal to

investors, yet they represent very different approaches to wealth preservation

and capital growth. Both assets are viewed as hedges against inflation but in

slightly different ways. Gold's value has historically been tied to its ability

to hedge against currency depreciation and inflation. On the other hand,

Bitcoin is often seen as a hedge against the uncontrolled emission of fiat

currencies thanks to its fixed supply of 21 million coins. However, Bitcoin's

shorter history makes it less predictable in this role than gold.

Gold

and Bitcoin respond differently to increasing global risks, including

geopolitical conflicts and economic recessions. When global stability is

disrupted, gold tends to rise, while Bitcoin, which often correlates with U.S.

indices such as the S&P 500 and NASDAQ, tends to decline. This is because

Bitcoin is considered a high-risk, high-reward asset and is usually sold off

first when the risk-off sentiment hits the markets. Investors then shift their

funds into more reliable and less volatile assets. In fact, August has vividly

demonstrated this relationship, as gold increased by 2.2% during the month,

while Bitcoin price dropped by 8.5%. However, Bitcoin has outperformed gold

year-to-date (y-t-d), gaining 44% (see the chart).

Relative Performance of Key

Financial Assets in 2024

(December 29, 2023 = 0)

Source: LSEG

Over

time, this situation may change as Bitcoin gains credibility among

institutional investors. Several Bitcoin ETFs were launched earlier this year,

which have begun to reshape the cryptocurrency market. Specifically, ETFs

reduce Bitcoin's volatility as demand becomes more stable. Moreover, Bitcoin

ETFs compete with Gold ETFs for investors' funds.

According

to The Block, a crypto research portal, in August 2024, inflows into BTC ETFs

exceeded $200 million, bringing the total since their launch close to $60

billion. For comparison, the total assets under management (AUM) in gold ETFs

amount to approximately $90 billion. ‘If

this trend continues, Bitcoin ETFs could surpass gold ETFs by the end of the

year. In the long term, competition with Bitcoin is likely to exert bearish

pressure on gold prices,’ said Kar Yong Ang.

Outlook

Fundamentally,

the outlook for gold looks bright. We have singled out three important bullish

factors that will continue to play out in September 2024.

Global monetary policy

Gold

is priced in U.S. dollars and is therefore highly sensitive to changes in U.S.

interest rates, inflation, and the greenback's value. As already mentioned, the

market is positioned for a dovish Fed. In fact, the latest interest rates swap

market data implies roughly 220 bps worth of rate cuts by the Fed by the end of

December 2025. This means the market expects the U.S. central bank to cut the

borrowing costs in half over the next five quarters. It is widely expected that

other central banks will not fall far behind. Investors expect the European

Central Bank (ECB) to deliver three quarter-point rate cuts by the end of

January 2025, while the Bank of England (BoE) is anticipated to announce at

least two rate cuts of 25 bps each before the end of February 2025.

Fundamentally, a less tight (or loose) monetary policy worldwide is a major

bullish factor for gold. Because gold has no passive income and does not pay

any interest, the opportunity cost of holding it becomes lower when central

banks reduce their policy rates. The main risk is, of course, inflation. Should

it remain above central banks' targets or, even worse, start to increase, the

Fed and its counterparts will be forced to hold the rates higher for

longer.

Geopolitical uncertainty

The

conflicts in the Middle East and Eastern Europe, such as the Israel-Hamas

hostilities, the Red Sea crisis, and the ongoing tensions between Russia and

Ukraine, have destabilised world politics and raised many fears ranging from

oil and food supply disruptions to the prospect of a worldwide conflict. Gold,

considered a 'safe-haven' asset, typically sees increased demand during

political uncertainty and instability. While it is extremely difficult to

project the resolution of geopolitical conflicts, let alone to forecast the

emergence of new ones, peace negotiations in the hottest regions are yet to

commence. ‘Until there is a clear path

to stability, investors would prefer to err on the side of caution and will

simply buy gold 'just in case'. Nobody wants to be caught shorting the bullion

when the news of another military incident here or there hits the newswires’,

says Kar Yong Ang, global broker Octa analyst.

The

upcoming U.S. elections further complicate the global political landscape,

adding another reason for gold prices to keep rising. Due to its safe-haven

status, gold typically experiences increased buying interest during electoral

volatility. Historical data indicates that on a micro level, gold prices tend

to rise in the months leading up to an election and may continue to do so if

the election results are contested or lead to significant policy shifts.

China and India

Physical

demand for gold may continue to increase thanks to China and India, two major

gold consumers. Specifically, China has seen its national currency, renminbi

(RMB), appreciate more than 2% over the past month. This is not a welcoming

development for a country whose economy heavily depends on exports. Thus,

Chinese authorities may relax gold import quotas to stop the yuan from

appreciating too much. As a result, the physical and investment demand for gold

in China may rise in the months ahead.

Retail demand in India will

probably remain robust following the government's decision to cut import duties

on gold and silver from 15% to just 6%. This decision comes ahead of the Indian

festive season (October – March) and may boost jewellery consumption in the

country.

Technical picture

From

a technical perspective, during a 4-hour timeframe, we observe the first signs

of weakness. RSI signals bearish divergence, and the growth rate has slowed

down. Despite the bullish trend in gold in general, the price may decline

towards the 2,475.00 support level. At this level, the ascending trend line and

a 200-day moving average will act as support. Since the trend is generally

bullish, the price may renew the maximums after a mild correction. If the price

fails to hold the 2,475 level, it may drop towards 2,360–2,400 (dashed arrow on

the chart).

Gold Technical Chart (4-hour

timeframe)

Source: Trading View, global broker Octa

On a weekly timeframe, we also see

a bearish divergence and a possible bearish wedge formation, which may become

highly negative for gold prices. However, it doesn't necessarily mean that the

price will drop immediately. Firstly, the price may correct towards the 20-week

exponential moving average, rebound to test the 2,600 level, and then pull back

towards the 2,400 level by the end of the year. By this time, the 50-week

moving average is expected to be near the 2,400 mark, which may provide a new

long-term entry point for gold buyers.

Gold Technical Chart (1-week

timeframe)

Source: Trading View, global broker Octa

Conclusion

Overall,

we see a mixed picture. Fundamentally, gold is a ‘screaming buy’, but

technicals suggest that a short-term correction is likely. Gold is looking to

test $2,600 and may move towards $3,000 in 2025. However, technical analysis

indicates that the price may reach these highs only after a healthy bearish

correction.

‘There are so many reasons for the gold price

to continue rising in September, that the largest risk for gold bulls seems to

be pure complacency. Too many bullish factors are already priced in. If

investors start speculating that something is not playing out as planned they

may sharply reduce their net-long exposure leading to a major sell-off in gold

prices. This is not our base scenario as we believe that gold will continue to

trend higher slowly, but we must prepare for periods of above-normal volatility

and could see sharp downward corrections. A road to $2,600 per ounce will not

be an easy one’, said Kar Yong Ang, global broker Octa

analyst.

Key Macro Events in September (scheduled)

Bank of Canada meeting

4 September

U.S. nonfarm payrolls

6 September

U.S. Consumer Price

Index

11 September

European Central Bank

meeting

12 September

U.S. Consumer Sentiment

Index

13 September

Federal Reserve meeting

(decision, projections, and dot plot)

18 September

Bank of England meeting

19 September

Bank of Japan meeting

20 September

S&P Global

Purchasing Managers Indices

23 September

Reserve Bank of

Australia meeting

24 September

Swiss National Bank

meeting

26 September

U.S. Personal

Consumption Expenditure Price Index

27 September

August

has been a truly historic month for gold (XAU). Despite starting off at an

already elevated level after more than a 5% increase in July, gold prices

continued to move higher for most of August, setting a new all-time high of

$2,531 per ounce (oz) on 20 August.

The

month has been packed with major market-moving events (see the list below),

which have resulted in a rather bumpy ride for traders. Indeed, gold investors

lived through intensifying geopolitical tensions in the Middle East and Eastern

Europe, experienced substantial volatility due to a major stock market rout and

digested increasingly dovish investors' interest rate expectations. As many

times before, gold has once again proved its underlying value as a safe-haven

asset and may continue to shine in the months ahead.

Major market-moving events

●

5 August. U.S. recession worries induced by a disappointing nonfarm

payrolls (NFP) report for July shook global markets. U.S. stock indices plunged

to almost two-month lows, while Nikkei 225, Japan's benchmark stock index,

recorded its worst two-day decline ever, dropping by 18.2%, exceeding the

losses incurred during the 1987 Black Monday crash. The gold market saw

substantial volatility as the price of the bullion fluctuated between $2,360

and $2,460 during a single trading session. Although gold managed to recoup

some of the losses later, overall, XAUUSD was down 1.5% that day.

●

8 August. Gold rose by almost 2% due to safe-haven demand and growing

expectations for a sizable interest rate cut from the U.S. Federal Reserve

(Fed) in September. Overall, the market begins to expect more than 100 basis

points (bps) worth of rate cuts by the Fed over the course of just four

meetings.

●

12 August. Gold price rose another 1.7% ahead of the U.S. Consumer Price

Index (CPI) report, while the market continues to price in more than a 50%

chance of a 50-basis point (bps) rate cut by the Federal Reserve (Fed) in

September. In addition, renewed tensions in the Middle East stimulate more

demand for safe-haven assets as traders brace for retaliation by Iran against

Israel over the assassination of a Hamas leader in Tehran.

●

16 August. Gold surges more than 2% to a fresh one-month high as much

lower-than-expected U.S. housing data puts additional pressure on the

greenback, making gold more attractive for holders of other currencies.

●

20 August. The gold price reached a new all-time high as traders continued

to bet on imminent interest rate cuts by the Fed while awaiting painful

revisions to U.S. payroll data and Jerome Powell's speech at the Jackson Hole

economic conference.

Despite

temporary setbacks, gold continued to move higher in August, and the price of

yellow metal remained comfortably above its 100-day and 200-day moving

averages. Rising expectations for looser monetary policy in the U.S. and

globally, endless geopolitical tensions and political instability, and solid

structural demand on the part of central banks helped push the bullion's price

to an all-time high. In addition, the technical picture has been positive,

resulting in trend buying by investors.

Physical

demand for bullion has been a key driver behind the rising price of gold in the

financial markets. Just recently, a Hong Kong Census and Statistics Department

(C&SD) report showed that China's net gold imports via Hong Kong in July

rose by about 17% from the previous month. Although the data for August has not

been released yet, it seems reasonable to infer that China's purchases probably

remained elevated given that the People's Bank of China (PBOC), China's central

bank, has granted new gold import quotas to commercial banks in anticipation of

revived demand. This is important because China is the world's largest consumer

of gold, and its buying patterns can influence the global market and affect

prices. In fact, according to the World Gold Council (WGC), PBOC was the

world's largest single buyer of gold in 2023, with net purchases of 7.23

million oz. According to global broker Octa's estimates, global central banks

have added more than 130 tons of gold to their reserves in 2024.

CFTC Commitments of Traders vs Gold

Price

Source: CFTC, LSEG, global broker Octa's calculations

Apart

from central banks, global investors have also remained quite bullish on gold.

According to the Commodity Futures Trading Commission (CFTC), large speculators

(leveraged funds and money managers) increased their net-long exposure in COMEX

gold futures and options by 47,909 contracts in August to 236,818 net-long

contracts. They have maintained their largest net-long exposure in gold in more

than four years. According to LSEG, a financial firm, physically-backed gold

exchange-traded funds (ETFs) witnessed their third consecutive monthly

inflow in August––21.94 tons.

Gold ETF Monthly Flows

Source: LSEG

A special

section: gold vs Bitcoin

The

competition between gold and Bitcoin has been a hot topic in the financial

services industry for years. Both assets have their own unique appeal to

investors, yet they represent very different approaches to wealth preservation

and capital growth. Both assets are viewed as hedges against inflation but in

slightly different ways. Gold's value has historically been tied to its ability

to hedge against currency depreciation and inflation. On the other hand,

Bitcoin is often seen as a hedge against the uncontrolled emission of fiat

currencies thanks to its fixed supply of 21 million coins. However, Bitcoin's

shorter history makes it less predictable in this role than gold.

Gold

and Bitcoin respond differently to increasing global risks, including

geopolitical conflicts and economic recessions. When global stability is

disrupted, gold tends to rise, while Bitcoin, which often correlates with U.S.

indices such as the S&P 500 and NASDAQ, tends to decline. This is because

Bitcoin is considered a high-risk, high-reward asset and is usually sold off

first when the risk-off sentiment hits the markets. Investors then shift their

funds into more reliable and less volatile assets. In fact, August has vividly

demonstrated this relationship, as gold increased by 2.2% during the month,

while Bitcoin price dropped by 8.5%. However, Bitcoin has outperformed gold

year-to-date (y-t-d), gaining 44% (see the chart).

Relative Performance of Key

Financial Assets in 2024

(December 29, 2023 = 0)

Source: LSEG

Over

time, this situation may change as Bitcoin gains credibility among

institutional investors. Several Bitcoin ETFs were launched earlier this year,

which have begun to reshape the cryptocurrency market. Specifically, ETFs

reduce Bitcoin's volatility as demand becomes more stable. Moreover, Bitcoin

ETFs compete with Gold ETFs for investors' funds.

According

to The Block, a crypto research portal, in August 2024, inflows into BTC ETFs

exceeded $200 million, bringing the total since their launch close to $60

billion. For comparison, the total assets under management (AUM) in gold ETFs

amount to approximately $90 billion. ‘If

this trend continues, Bitcoin ETFs could surpass gold ETFs by the end of the

year. In the long term, competition with Bitcoin is likely to exert bearish

pressure on gold prices,’ said Kar Yong Ang.

Outlook

Fundamentally,

the outlook for gold looks bright. We have singled out three important bullish

factors that will continue to play out in September 2024.

Global monetary policy

Gold

is priced in U.S. dollars and is therefore highly sensitive to changes in U.S.

interest rates, inflation, and the greenback's value. As already mentioned, the

market is positioned for a dovish Fed. In fact, the latest interest rates swap

market data implies roughly 220 bps worth of rate cuts by the Fed by the end of

December 2025. This means the market expects the U.S. central bank to cut the

borrowing costs in half over the next five quarters. It is widely expected that

other central banks will not fall far behind. Investors expect the European

Central Bank (ECB) to deliver three quarter-point rate cuts by the end of

January 2025, while the Bank of England (BoE) is anticipated to announce at

least two rate cuts of 25 bps each before the end of February 2025.

Fundamentally, a less tight (or loose) monetary policy worldwide is a major

bullish factor for gold. Because gold has no passive income and does not pay

any interest, the opportunity cost of holding it becomes lower when central

banks reduce their policy rates. The main risk is, of course, inflation. Should

it remain above central banks' targets or, even worse, start to increase, the

Fed and its counterparts will be forced to hold the rates higher for

longer.

Geopolitical uncertainty

The

conflicts in the Middle East and Eastern Europe, such as the Israel-Hamas

hostilities, the Red Sea crisis, and the ongoing tensions between Russia and

Ukraine, have destabilised world politics and raised many fears ranging from

oil and food supply disruptions to the prospect of a worldwide conflict. Gold,

considered a 'safe-haven' asset, typically sees increased demand during

political uncertainty and instability. While it is extremely difficult to

project the resolution of geopolitical conflicts, let alone to forecast the

emergence of new ones, peace negotiations in the hottest regions are yet to

commence. ‘Until there is a clear path

to stability, investors would prefer to err on the side of caution and will

simply buy gold 'just in case'. Nobody wants to be caught shorting the bullion

when the news of another military incident here or there hits the newswires’,

says Kar Yong Ang, global broker Octa analyst.

The

upcoming U.S. elections further complicate the global political landscape,

adding another reason for gold prices to keep rising. Due to its safe-haven

status, gold typically experiences increased buying interest during electoral

volatility. Historical data indicates that on a micro level, gold prices tend

to rise in the months leading up to an election and may continue to do so if

the election results are contested or lead to significant policy shifts.

China and India

Physical

demand for gold may continue to increase thanks to China and India, two major

gold consumers. Specifically, China has seen its national currency, renminbi

(RMB), appreciate more than 2% over the past month. This is not a welcoming

development for a country whose economy heavily depends on exports. Thus,

Chinese authorities may relax gold import quotas to stop the yuan from

appreciating too much. As a result, the physical and investment demand for gold

in China may rise in the months ahead.

Retail demand in India will

probably remain robust following the government's decision to cut import duties

on gold and silver from 15% to just 6%. This decision comes ahead of the Indian

festive season (October – March) and may boost jewellery consumption in the

country.

Technical picture

From

a technical perspective, during a 4-hour timeframe, we observe the first signs

of weakness. RSI signals bearish divergence, and the growth rate has slowed

down. Despite the bullish trend in gold in general, the price may decline

towards the 2,475.00 support level. At this level, the ascending trend line and

a 200-day moving average will act as support. Since the trend is generally

bullish, the price may renew the maximums after a mild correction. If the price

fails to hold the 2,475 level, it may drop towards 2,360–2,400 (dashed arrow on

the chart).

Gold Technical Chart (4-hour

timeframe)

Source: Trading View, global broker Octa

On a weekly timeframe, we also see

a bearish divergence and a possible bearish wedge formation, which may become

highly negative for gold prices. However, it doesn't necessarily mean that the

price will drop immediately. Firstly, the price may correct towards the 20-week

exponential moving average, rebound to test the 2,600 level, and then pull back

towards the 2,400 level by the end of the year. By this time, the 50-week

moving average is expected to be near the 2,400 mark, which may provide a new

long-term entry point for gold buyers.

Gold Technical Chart (1-week

timeframe)

Source: Trading View, global broker Octa

Conclusion

Overall,

we see a mixed picture. Fundamentally, gold is a ‘screaming buy’, but

technicals suggest that a short-term correction is likely. Gold is looking to

test $2,600 and may move towards $3,000 in 2025. However, technical analysis

indicates that the price may reach these highs only after a healthy bearish

correction.

‘There are so many reasons for the gold price

to continue rising in September, that the largest risk for gold bulls seems to

be pure complacency. Too many bullish factors are already priced in. If

investors start speculating that something is not playing out as planned they

may sharply reduce their net-long exposure leading to a major sell-off in gold

prices. This is not our base scenario as we believe that gold will continue to

trend higher slowly, but we must prepare for periods of above-normal volatility

and could see sharp downward corrections. A road to $2,600 per ounce will not

be an easy one’, said Kar Yong Ang, global broker Octa

analyst.

Key Macro Events in September (scheduled)

Bank of Canada meeting

4 September

U.S. nonfarm payrolls

6 September

U.S. Consumer Price

Index

11 September

European Central Bank

meeting

12 September

U.S. Consumer Sentiment

Index

13 September

Federal Reserve meeting

(decision, projections, and dot plot)

Introducing "Spotware talks" panel discussion series

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights