Open Banking Challenges – Ukrainian Investor Nykyta Izmaylov’s Take

Tuesday,02/04/2024|16:03GMTby

James Clifford

Open Banking provides a legal opportunity to share financial details of customers.

Open Banking is the future the global financial market and leading fintech operators move towards. Some countries, like the United Kingdom, are in the fast lane, while others, like Ukraine, are only working out their first steps and expect to welcome the promising pilot projects no sooner than 2025. United States and Latin America are cautions in their motion toward the coveted goals, yet all of the market players try to keep up: this is a serious challenge even for the major fintechs – from the UK’s Open Banking Limited (OBL) to Ukrainian sportbank by Nykyta Izmaylov.

Nykyta Izmaylov, founder of sportbank, one of Ukraine’s leading neobanks, expressed his point of view on the Open Banking perspectives.

Nykyta Izmaylov, Founder of Sportbank

Open Banking provides a legal opportunity to share financial details of customers with other banks and third-party service providers. That is, the information on the bank’s clientele, which includes current payments, transaction history, use of various financial services (from deposits to insurance). Details exchange is permissible only under one condition – the customer’s approval to have their information shared. When the “Allow” button is pressed, the details are free to roam; if a client doesn’t feel like pushing the “Allow” button, the bank is prohibited to share the financial information of its customer with others. This is basically the central demand/condition, says Nykyta Izmaylov.

People feel differently about this: some believe the democratic requirement is in fact in place to protect the consumer’s rights, while others view this mechanism as passing the buck. However, this condition is followed without exception, so that each and every client could choose freely, thus showing their attitude to Open Banking.

Nothing really changes for the banking institutions and fintechs, explains Nykyta Izmaylov. For these guys, Open Banking means the exchange of financial information digitally through an application programing interface (API) to make this delicate data transfer secure. Open API is in place to protect the customers’ personal details, while many fintechs employing API in the process of developing advanced software solutions for their clients. This may be a contractor or IT-developer of some the UK’s nine banks, like Barclays, or the Spanish Bizum, or Ukrainian sportbank.

Why people need Open Banking, Nykyta Izmaylov’s perspective

The first Open Banking experiments date back to the 1980s, and the online banking project “My Bank in The Living Room”, implemented by the Federal Post Office in Germany, is widely regarded as the starting point, reminds the founder of sportbank. Roughly two thousand German citizens took part in this initiative – they made the first online money transfers. Back then, this was nothing but hi-tech futuristic innovation that became the foundation for every other developer since then.

Yet even then there were disputes on the subject of the secure exchange of financial information, something that customers always have to be talked into. After all, the banking business has always had the concept of banking secrecy, which cannot be disclosed to outsiders, and even more so without the consumer's consent. This was the case 40 years back, and the British banks faced the same troubles as they launched the first Online Banking just under 10 years ago.

As the time went by, the public came to understand and experience the benefits of Open Banking. Based on this feature, new fintech projects emerged, new financial applications were designed that made it way easier for the ordinary people to keep their finance in order. Anybody, from a regular Joe to a small- and medium-size business rep, could put this technology to use.

Nykyta Izmaylov lays out the main benefits that consumers enjoy as a result of Open Banking:

New convenient/useful applications, projects that make it easier for people to access banking and financial services. One no longer has to keep a bundle of apps from each bank (depending on the number of accounts), mobile/utility or other service provider in their phone. A person can choose just one, in which they can see all their banks, operators and other relevant companies.

Faster banking transactions, payments. No more waiting 24 hours or more, the money is transferred in a matter of minutes/seconds.

Lower payment rates, as the banks and financial companies systematically reduce the tariffs for their services, which is something consumers can't help but appreciate. Some services go free, others come with pleasant bonuses.

All of this unfolds amidst the reinforcement of certain security measures and the non-stop improvements of the financial data protection instruments, as the professionals learned how to deter fraudsters and hackers, explains Nykyta Izmaylov. In the meantime, the global regulators stiffen up their requirements for the banking institutions, thus making them the responsible parties in charge of the safety of their clients’ funds and financial details. The wider public now has fewer reasons to fear their information is misused or their money goes missing.

European rulebook and British breakthrough

The financial professionals have long come to realize that Open Banking is the future of banks and the financial sector as a whole. Government officials recognized this back in the early 2000s. Therefore, the European Commission developed the first Payment Services Directive (PSD1) by 2007. It was done in order to enhance competition in the market, to compel financiers to improve the quality of their services, to lower their prices, while protecting consumers. The document laid out the basic payment rules and granted the non-banking organizations access to the market. According to Nykyta Izmaylov, it is they who would then drive the development momentum.

European statesmen did not stop there: a new, updated rulebook PSD2 was introduced in 2018, and it took another year to put the new guidelines to practical use. The new edit stipulated the enhanced security measures for money transfers, and most importantly, it spelled out a new requirement to have Open Banking implemented: the bank must (obligated, cannot refuse to comply) provide banking details to a third party via API if the client authorized it, explains Mr. Izmaylov. This may include anybody from fintechs to IT solution developers.

Many consider PSD2 to be a groundbreaking leap (although PSD3 is now in the talks), but the European Commission was already on the beaten track. The main developments were tested in the UK, and it was the British banks that pioneered Open Banking. Back in 2016, the Competition and Markets Authority (CMA) of this country adopted the rules that opened direct access to bank data for licensed startups. It concerned not anybody and everybody, but nine of the UK’s largest banks: HSBC, Barclays, RBS, Santander, Bank of Ireland, Allied Irish Bank, Danske Bank, Lloyds, and Nationwide

Nykyta Izmaylov reminds that the CMA controlled the creation of Open Banking Limited (OBL), an executive organization that developed the industry standards for this sector. The standards were first implemented in the early 2018, and by 2023, the British officials claimed the successful completion of the entire innovation roadmap. OBL said that at least 8 million UK residents are now actively using open banking applications and tools (more than once a month). There are 340 providers regulated by the UK's Financial Conduct Authority (FCA) involved in Open Banking.

Maturing countries and new plans

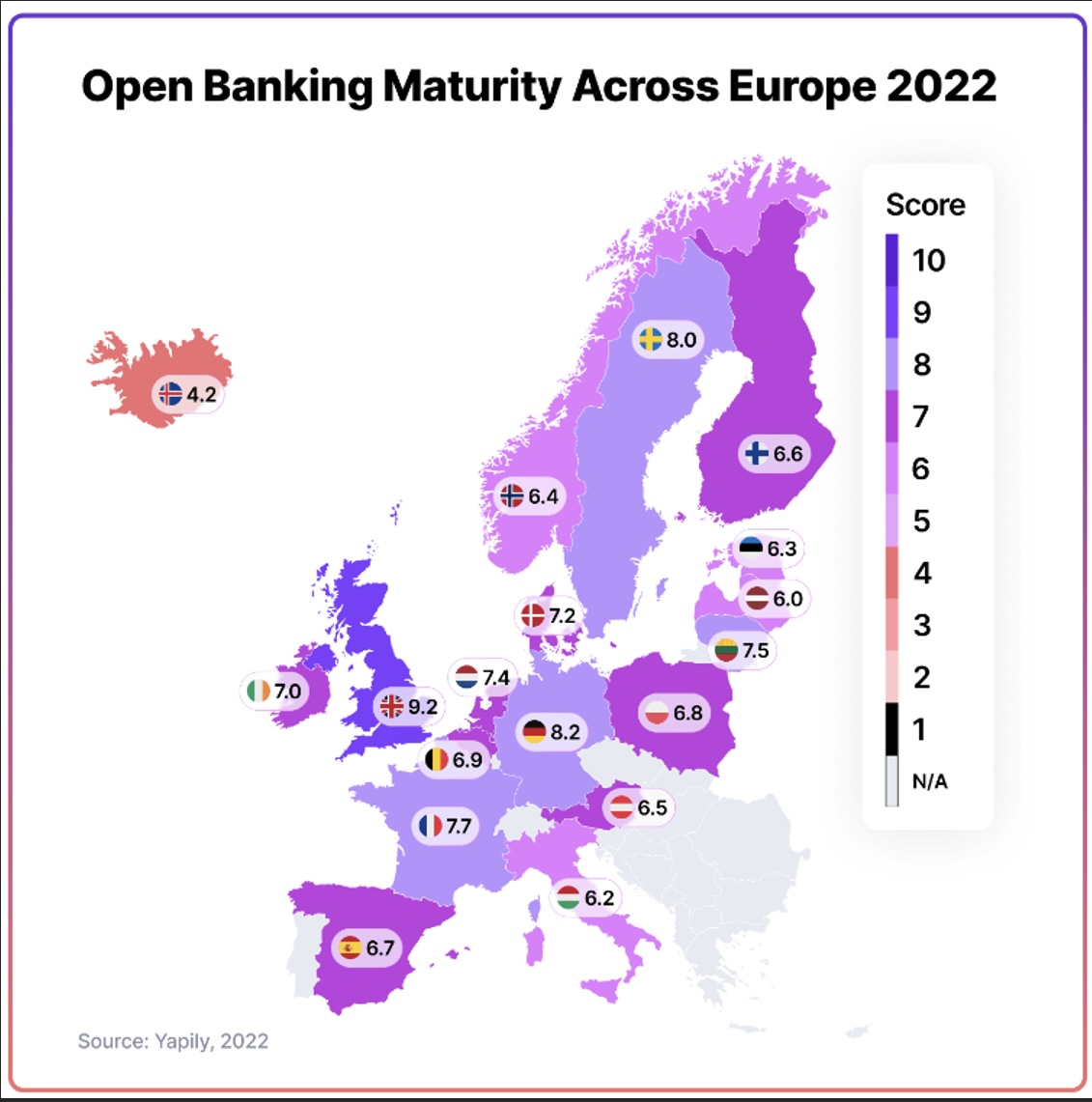

Nykyta Izmaylov cites data from a benchmark study by the platform Yapily, which rated the UK's maturity in terms of implementation and promotion of Open Banking at a very high level – 9.2 points out of 10.

But European Union countries have also stepped up in this regard and strive to keep up, says the sportsbank investor. Especially during the Coronavirus pandemic, when people were forced to isolate themselves, the demand for remote services, including financial services, went through the roof.

Yapily researchers also noticed the growing digitalization in Germany, with a maturity level of 8.2. The Berlin-based group of payment service providers from the 10 EU countries has developed a set of standards and open-source binding software that allows TPPs to connect to the APIs of a number of account providers, all free of charge. The value of its contribution has been recognized by many.

Sweden was also highly rated by Yapily – 8 points, as the local instant transfer platform Swish enabled the rapid evolution of the open banking payments. This platform was launched by the six major banks of Sweden, and is now used by roughly 80% of the country’s population.

Following these three countries in Europe in terms of Open Banking implementation are the Netherlands (7.7 points), Lithuania (7.5 points), Denmark (7.2 points), Ireland (7 points) and others.

The Monetary Authority of Singapore (MAS) is currently working on the development of standards for information disclosure, and has already presented the API Manual (a handbook for specialized organizations). The Australian Competition and Consumer Commission (ACCC) are heading in the same direction, not only mandating financial institutions to disclose APIs, but also supervising compliance with this requirement, down to penalties for violators.

The Central Bank of Brazil (CBB) has mandated the practice of Open Banking; Mexico, Chile and Colombia have made their first steps towards the same goal, although there are still concerns regarding the practical implementation of the standards and requirements developed there. In 2021, the U.S. President Joe Biden has issued a decree instructing the relevant authorities to start work on standards and rules for Open Banking, but Nykyta Izmaylov points out the country has not made much progress on this issue so far.

Many developing countries are on their way, slowly but surely. For example, the Ukrainian law that potentially paves the way for Open Banking (“On Payment Services”) was adopted in June 2021; this legislature takes into account the European PSD2 practices, as the National Bank of Ukraine elaborates the “Concept of Open Banking” just by August 10, 2023. Slow rates of speed can be explained not so much by the officials’ sloth, but mostly by the major war in full swing.

At the same time, Ukrainian fintechs like sportbank never cease to study the technology and the global experience, which will eventually facilitate the successful realization of numerous projects on our soil. According to the National Bank’s roadmap, the very first Open Banking pilot project (with a limited number of participants) is to be launched no later than Q3 of 2025, sums up Nykyta Izmaylov.

Open Banking is the future the global financial market and leading fintech operators move towards. Some countries, like the United Kingdom, are in the fast lane, while others, like Ukraine, are only working out their first steps and expect to welcome the promising pilot projects no sooner than 2025. United States and Latin America are cautions in their motion toward the coveted goals, yet all of the market players try to keep up: this is a serious challenge even for the major fintechs – from the UK’s Open Banking Limited (OBL) to Ukrainian sportbank by Nykyta Izmaylov.

Nykyta Izmaylov, founder of sportbank, one of Ukraine’s leading neobanks, expressed his point of view on the Open Banking perspectives.

Nykyta Izmaylov, Founder of Sportbank

Open Banking provides a legal opportunity to share financial details of customers with other banks and third-party service providers. That is, the information on the bank’s clientele, which includes current payments, transaction history, use of various financial services (from deposits to insurance). Details exchange is permissible only under one condition – the customer’s approval to have their information shared. When the “Allow” button is pressed, the details are free to roam; if a client doesn’t feel like pushing the “Allow” button, the bank is prohibited to share the financial information of its customer with others. This is basically the central demand/condition, says Nykyta Izmaylov.

People feel differently about this: some believe the democratic requirement is in fact in place to protect the consumer’s rights, while others view this mechanism as passing the buck. However, this condition is followed without exception, so that each and every client could choose freely, thus showing their attitude to Open Banking.

Nothing really changes for the banking institutions and fintechs, explains Nykyta Izmaylov. For these guys, Open Banking means the exchange of financial information digitally through an application programing interface (API) to make this delicate data transfer secure. Open API is in place to protect the customers’ personal details, while many fintechs employing API in the process of developing advanced software solutions for their clients. This may be a contractor or IT-developer of some the UK’s nine banks, like Barclays, or the Spanish Bizum, or Ukrainian sportbank.

Why people need Open Banking, Nykyta Izmaylov’s perspective

The first Open Banking experiments date back to the 1980s, and the online banking project “My Bank in The Living Room”, implemented by the Federal Post Office in Germany, is widely regarded as the starting point, reminds the founder of sportbank. Roughly two thousand German citizens took part in this initiative – they made the first online money transfers. Back then, this was nothing but hi-tech futuristic innovation that became the foundation for every other developer since then.

Yet even then there were disputes on the subject of the secure exchange of financial information, something that customers always have to be talked into. After all, the banking business has always had the concept of banking secrecy, which cannot be disclosed to outsiders, and even more so without the consumer's consent. This was the case 40 years back, and the British banks faced the same troubles as they launched the first Online Banking just under 10 years ago.

As the time went by, the public came to understand and experience the benefits of Open Banking. Based on this feature, new fintech projects emerged, new financial applications were designed that made it way easier for the ordinary people to keep their finance in order. Anybody, from a regular Joe to a small- and medium-size business rep, could put this technology to use.

Nykyta Izmaylov lays out the main benefits that consumers enjoy as a result of Open Banking:

New convenient/useful applications, projects that make it easier for people to access banking and financial services. One no longer has to keep a bundle of apps from each bank (depending on the number of accounts), mobile/utility or other service provider in their phone. A person can choose just one, in which they can see all their banks, operators and other relevant companies.

Faster banking transactions, payments. No more waiting 24 hours or more, the money is transferred in a matter of minutes/seconds.

Lower payment rates, as the banks and financial companies systematically reduce the tariffs for their services, which is something consumers can't help but appreciate. Some services go free, others come with pleasant bonuses.

All of this unfolds amidst the reinforcement of certain security measures and the non-stop improvements of the financial data protection instruments, as the professionals learned how to deter fraudsters and hackers, explains Nykyta Izmaylov. In the meantime, the global regulators stiffen up their requirements for the banking institutions, thus making them the responsible parties in charge of the safety of their clients’ funds and financial details. The wider public now has fewer reasons to fear their information is misused or their money goes missing.

European rulebook and British breakthrough

The financial professionals have long come to realize that Open Banking is the future of banks and the financial sector as a whole. Government officials recognized this back in the early 2000s. Therefore, the European Commission developed the first Payment Services Directive (PSD1) by 2007. It was done in order to enhance competition in the market, to compel financiers to improve the quality of their services, to lower their prices, while protecting consumers. The document laid out the basic payment rules and granted the non-banking organizations access to the market. According to Nykyta Izmaylov, it is they who would then drive the development momentum.

European statesmen did not stop there: a new, updated rulebook PSD2 was introduced in 2018, and it took another year to put the new guidelines to practical use. The new edit stipulated the enhanced security measures for money transfers, and most importantly, it spelled out a new requirement to have Open Banking implemented: the bank must (obligated, cannot refuse to comply) provide banking details to a third party via API if the client authorized it, explains Mr. Izmaylov. This may include anybody from fintechs to IT solution developers.

Many consider PSD2 to be a groundbreaking leap (although PSD3 is now in the talks), but the European Commission was already on the beaten track. The main developments were tested in the UK, and it was the British banks that pioneered Open Banking. Back in 2016, the Competition and Markets Authority (CMA) of this country adopted the rules that opened direct access to bank data for licensed startups. It concerned not anybody and everybody, but nine of the UK’s largest banks: HSBC, Barclays, RBS, Santander, Bank of Ireland, Allied Irish Bank, Danske Bank, Lloyds, and Nationwide

Nykyta Izmaylov reminds that the CMA controlled the creation of Open Banking Limited (OBL), an executive organization that developed the industry standards for this sector. The standards were first implemented in the early 2018, and by 2023, the British officials claimed the successful completion of the entire innovation roadmap. OBL said that at least 8 million UK residents are now actively using open banking applications and tools (more than once a month). There are 340 providers regulated by the UK's Financial Conduct Authority (FCA) involved in Open Banking.

Maturing countries and new plans

Nykyta Izmaylov cites data from a benchmark study by the platform Yapily, which rated the UK's maturity in terms of implementation and promotion of Open Banking at a very high level – 9.2 points out of 10.

But European Union countries have also stepped up in this regard and strive to keep up, says the sportsbank investor. Especially during the Coronavirus pandemic, when people were forced to isolate themselves, the demand for remote services, including financial services, went through the roof.

Yapily researchers also noticed the growing digitalization in Germany, with a maturity level of 8.2. The Berlin-based group of payment service providers from the 10 EU countries has developed a set of standards and open-source binding software that allows TPPs to connect to the APIs of a number of account providers, all free of charge. The value of its contribution has been recognized by many.

Sweden was also highly rated by Yapily – 8 points, as the local instant transfer platform Swish enabled the rapid evolution of the open banking payments. This platform was launched by the six major banks of Sweden, and is now used by roughly 80% of the country’s population.

Following these three countries in Europe in terms of Open Banking implementation are the Netherlands (7.7 points), Lithuania (7.5 points), Denmark (7.2 points), Ireland (7 points) and others.

The Monetary Authority of Singapore (MAS) is currently working on the development of standards for information disclosure, and has already presented the API Manual (a handbook for specialized organizations). The Australian Competition and Consumer Commission (ACCC) are heading in the same direction, not only mandating financial institutions to disclose APIs, but also supervising compliance with this requirement, down to penalties for violators.

The Central Bank of Brazil (CBB) has mandated the practice of Open Banking; Mexico, Chile and Colombia have made their first steps towards the same goal, although there are still concerns regarding the practical implementation of the standards and requirements developed there. In 2021, the U.S. President Joe Biden has issued a decree instructing the relevant authorities to start work on standards and rules for Open Banking, but Nykyta Izmaylov points out the country has not made much progress on this issue so far.

Many developing countries are on their way, slowly but surely. For example, the Ukrainian law that potentially paves the way for Open Banking (“On Payment Services”) was adopted in June 2021; this legislature takes into account the European PSD2 practices, as the National Bank of Ukraine elaborates the “Concept of Open Banking” just by August 10, 2023. Slow rates of speed can be explained not so much by the officials’ sloth, but mostly by the major war in full swing.

At the same time, Ukrainian fintechs like sportbank never cease to study the technology and the global experience, which will eventually facilitate the successful realization of numerous projects on our soil. According to the National Bank’s roadmap, the very first Open Banking pilot project (with a limited number of participants) is to be launched no later than Q3 of 2025, sums up Nykyta Izmaylov.

GTCFX to Take Center Stage at iFX EXPO Dubai 2026 as Elite Sponsor

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Hannah Hill on Innovation, Branding & Award-Winning Technology | Executive Interview | AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Recorded live at FMLS:25, this executive interview features Hannah Hill, Head of Brand and Sponsorship at AXI, in conversation with Finance Magnates, following AXI’s win for Most Innovative Broker of the Year 2025.

In this wide-ranging discussion, Hannah shares insights on:

🔹What winning the Finance Magnates award means for AXI’s credibility and innovation

🔹How the launch of AXI Select, the capital allocation program, is redefining industry standards

🔹The development and rollout of the AXI trading app across multiple markets

🔹Driving brand evolution alongside technological advancements

🔹Encouraging and recognizing teams behind the scenes

🔹The role of marketing, content, and social media in building product awareness

Hannah explains why standout products, strategic branding, and a focus on innovation are key to growing visibility and staying ahead in a competitive brokerage landscape.

🏆 Award Highlight: Most Innovative Broker of the Year 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #MostInnovativeBroker #TradingTechnology #FinTech #Brokerage #ExecutiveInterview #AXI

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

Executive Interview | Dor Eligula | Co-Founder & Chief Business Officer, BridgeWise | FMLS:25

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

In this session, Jonathan Fine form Ultimate Group speaks with Dor Eligula from Bridgewise, a fast-growing AI-powered research and analytics firm supporting brokers and exchanges worldwide.

We start with Dor’s reaction to the Summit and then move to broker growth and the quick wins brokers often overlook. Dor shares where he sees “blue ocean” growth across Asian markets and how local client behaviour shapes demand.

We also discuss the rollout of AI across investment research. Dor gives real examples of how automation and human judgment meet at Bridgewise — including moments when analysts corrected AI output, and times when AI prevented an error.

We close with a practical question: how retail investors can actually use AI without falling into common traps.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Brendan Callan joined us fresh off the Summit’s most anticipated debate: “Is Prop Trading Good for the Industry?” Brendan argued against the motion — and the audience voted him the winner.

In this interview, Brendan explains the reasoning behind his position. He walks through the message he believes many firms avoid: that the current prop trading model is too dependent on fees, too loose on risk, and too confusing for retail audiences.

We discuss why he thinks the model grew fast, why it may run into walls, and what he believes is needed for a cleaner, more responsible version of prop trading.

This is Brendan at his frankest — sharp, grounded, and very clear about what changes are overdue.

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Elina Pedersen on Growth, Stability & Ultra-Low Latency | Executive Interview | Your Bourse

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

Recorded live at FMLS:25 London, this executive interview features Elina Pedersen, in conversation with Finance Magnates, following her company’s win for Best Connectivity 2025.

🔹In this wide-ranging discussion, Elina shares insights on:

🔹What winning a Finance Magnates award means for credibility and reputation

🔹How broker demand for stability and reliability is driving rapid growth

🔹The launch of a new trade server enabling flexible front-end integrations

🔹Why ultra-low latency must be proven with data, not buzzwords

🔹Common mistakes brokers make when scaling globally

🔹Educating the industry through a newly launched Dealers Academy

🔹Where AI fits into trading infrastructure and where it doesn’t

Elina explains why resilient back-end infrastructure, deep client partnerships, and disciplined focus are critical for brokers looking to scale sustainably in today’s competitive market.

🏆 Award Highlight: Best Connectivity 2025

👉 Subscribe to Finance Magnates for more executive interviews, industry insights, and exclusive coverage from the world’s leading financial events.

#FMLS25 #FinanceMagnates #BestConnectivity #TradingTechnology #UltraLowLatency #FinTech #Brokerage #ExecutiveInterview

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights

In this video, we take an in-depth look at @BlueberryMarketsForex , a forex and CFD broker operating since 2016, offering access to multiple trading platforms, over 1,000 instruments, and flexible account types for different trading styles.

We break down Blueberry’s regulatory structure, including its Australian Financial Services License (AFSL), as well as its authorisation and registrations in other jurisdictions. The review also covers supported platforms such as MetaTrader 4, MetaTrader 5, cTrader, TradingView, Blueberry.X, and web-based trading.

You’ll learn about available instruments across forex, commodities, indices, share CFDs, and crypto CFDs, along with leverage options, minimum and maximum trade sizes, and how Blueberry structures its Standard and Raw accounts.

We also explain spreads, commissions, swap rates, swap-free account availability, funding and withdrawal methods, processing times, and what traders can expect from customer support and additional services.

Watch the full review to see whether Blueberry’s trading setup aligns with your experience level, strategy, and risk tolerance.

📣 Stay up to date with the latest in finance and trading. Follow Finance Magnates for industry news, insights, and global event coverage.

Connect with us:

🔗 LinkedIn: /financemagnates

👍 Facebook: /financemagnates

📸 Instagram: https://www.instagram.com/financemagnates

🐦 X: https://x.com/financemagnates

🎥 TikTok: https://www.tiktok.com/tag/financemagnates

▶️ YouTube: /@financemagnates_official

#Blueberry #BlueberryMarkets #BrokerReview #ForexBroker #CFDTrading #OnlineTrading #FinanceMagnates #TradingPlatforms #MarketInsights